PI Industries is one of India's leading agrochemical companies. Offering integrated and innovative products and solutions to its customers, PI enjoys tremendous brand recognition and a strong global presence built over the years on a strong foundation of trust, integrity, and respect.

PI Industries: All poised to cater the increasing demand

TL;DR.

PI Industries Ltd is a leading player in the agro-chemicals space having strong presence in both domestic and export markets. Read further to know more

PI has exclusive rights from several global corporations for distribution of their products in India. It constantly evaluates prospects to further expand its product portfolio.

PI Industries Ltd is a leading player in the agrochemicals space having strong presence in both domestic and export markets. It has state-of-art facilities in Gujarat having integrated process development teams with in-house engineering capabilities.

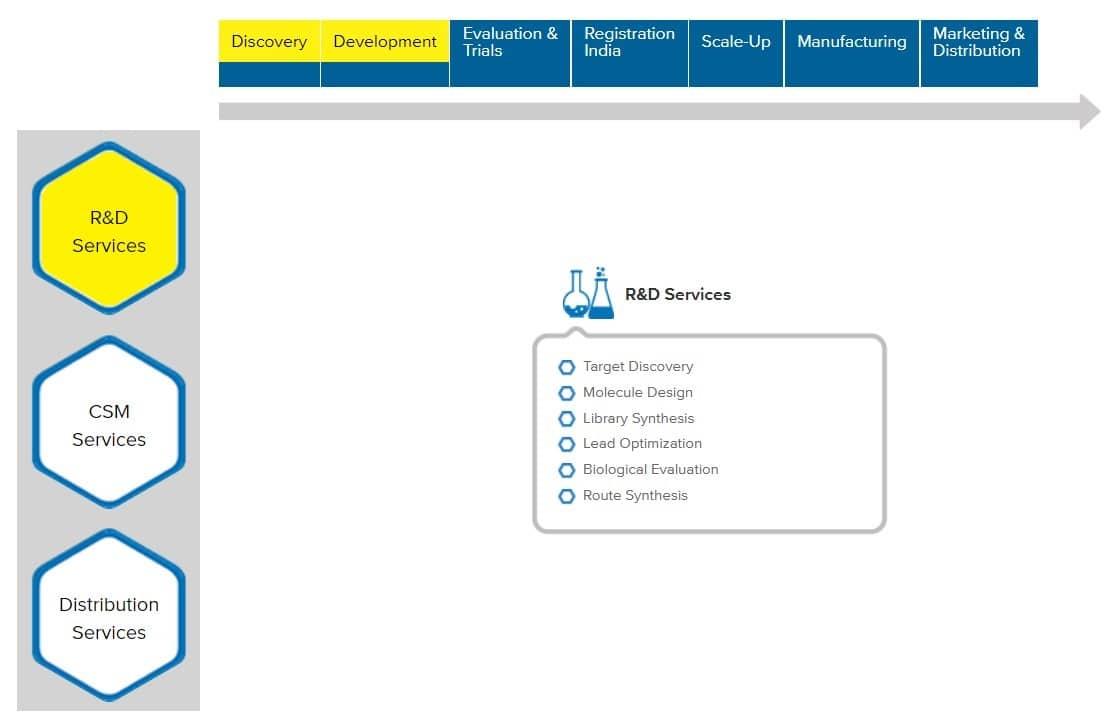

Business model

Business model

Over the past several decades, PI has worked relentlessly to provide value-added solutions to millions of farmers in the country and across the globe, carving a niche for itself in the market, and leaving a lasting impact on the minds of the customers. The strategic, differentiated and partnership approach has enabled the Company to grow at a faster pace, delivering superior returns to all its stakeholders.

PI Industries posted a strong quarter beating street estimates. The company's exports grew 34% (over a high base) mainly on account of an increase in revenue of existing products and 19% growth in the domestic segment, which was driven by the good Kharif season. The company reported revenue of 1,770 Cr. up 31% YoY & 15% QoQ. It reported an EBITDA Margin of 24.4%.

The growth was led by a favourable product mix coupled with improved operating leverage. The company has revised its growth guidance from 18-20% earlier to over 20%+ in FY23 given the strong demand witnessed from non-agro chem products across the CSM segment. The company will continue its healthy growth trajectory in the future, supported by a normal Kharif season going ahead.

Current position for the company

Confident in delivering 20% growth in FY23. The tax rate for the year would be 16.5% as the company will receive the SEZ benefit for 5 more years. Total Capex stood at 120 Cr for H1 FY23 & total expected Capex for FY23 stands at 700 Cr (650 Cr earlier). Liquidity position as of Q1 FY23 stands at 2321 Cr.

The net $ 0.4 bn increase in orderbook came largely from existing CSM agri-business. Commercialised electro chemicals products last year. Focus this year will be scaling them up.

In terms of building capacity, PI is building capacities in electronic chemicals at a commercial as well as private scale. A good number of molecules are there in the pipeline. Freshness index i.e products launched in the last three years constitute 16-18% of revenue.

The company continues to focus on improving its balance sheet in FY23. Capex of ₹120.4 cr in 1H23 is in line with company guidance. Management expects capex to reach ₹700 cr in FY23 to meet its order book. PI’s net worth rose to ₹6,617.6 cr. It maintained higher inventory levels of Rs. 1,609.5 cr. to meet customer supply schedules and avert supply chain disruptions. Trade working capital increased by 8 days i.e., 103 to 111 in 1HFY23.

Outlook

CSM Outlook & Demand –The CSM segment witnessed strong growth in exports, up 29% YoY while growth in the domestic market was 36%. The growth in both segments was largely volume led through ~5-6% growth came from the price increase. Traction in new enquiries for non-agro chemical space of electronics, Pharma, and other areas continued.

New Product Launch – The company launched 5 new products in H1 and has products at different stages of development and registration. It is targeting expansion into wheat crops and horticulture, and better efficiency in products launched in the last quarter.

The company has a rich pipeline of 40+ products at different development stages, of which over 20% are non-agro chemical products. PIIND will commercialise 6 more molecules this year, out of which, 4-5 are from Agro-Chem and 1 will be from the non-Agro-Chem segment.

8.3% growth is expected for the Asia Pacific market during the year. PI has invested in state-of-the-art technologies to ensure the highest level of safety, product quality, productivity, and consistency in the resulting products. The four integrated manufacturing facilities are cumulatively spread across 100+ acre land and include 15 multi-purpose plants.

The manufacturing units are equipped with dedicated high-pressure reaction facilities with a high level of futuristic automation. In addition, PI’s 2 Formulation units at Panoli cater to domestic requirements of local as well as global clientele.

PIIND is well-placed for future growth given clear revenue visibility in the CSM segment and strong domestic formulation business. The company is also strategically developing its capabilities which are translating into improved asset turns and higher growth in the top line.

Shuchi Nahar is a Certified Research Analyst. She can be found on Twitter at @shuchi_nahar

Note: This article is for informational purposes only. Please speak to a SEBI-registered investment advisor before making any investment related investment-related decision.

First Published: 14 Dec 2022, 10:37 AM IST