Banks have been in focus lately after most lenders reported strong results for the quarter ended March 2023 (Q4FY23). Overall, banks have been performing well on the back of the expansion of loan portfolios, rise in margins, and improving asset quality.

Private vs PSU Banks: Which ones should you choose in the current market scenario?

TL;DR.

In the last 1 year, PSU banks have outperformed private banks with the Nifty PSU Bank index surging over 67 percent and the Nifty Private Bank index advancing 33 percent. However, this trend has reversed in recent times.

In the last 1 year, PSU banks have outperformed private banks with the Nifty PSU Bank index surging over 67 percent and the Nifty Private Bank index advancing 33 percent. However, this trend has reversed in recent times. In 2023 YTD, the Nifty PSU Bank index has shed over 5 percent whereas the Nifty Private Bank index is up 2 percent.

So among private and PSU banks, which ones should investors focus on more and why? Let's find out.

EXPERT TAKE:

Dnyanada Vaidya, Research Analyst, Axis Securities, prefers private sector banks over PSU ones.

"We remain optimistic about private banks' ability to sustain the growth momentum, maintain healthy asset quality, and deliver strong earnings growth. However, that said, amongst the public sector banks, we prefer names like SBI and BoB, with many of their metrics being comparable to the top private banks. Our top picks from the banking space are ICICI Bank and SBI from the larger banks, while we like Federal Bank among the mid-tier banks," the expert explained.

Meanwhile, Deepak Jasani, Head of Retail Research, HDFC Securities, believes that private banks could give moderate returns with lower risks, while PSU banks could give higher returns with higher risks.

Jasani noted that PSU banks have underperformed over the last few months after gaining sharply between July 2022 and January 2023 and their initial Q4 results are encouraging and the valuation of most PSU banks seems attractive. However, he pointed out that they could be exposed to corporate defaults in case of a slowdown (like the Go Air issue). Private banks, on the other hand, continue to perform well in terms of credit growth, NIM and asset quality, but the scope of improvements from these lofty levels seems low, he added.

Sonam Srivastava- Founder at Wright Research, prefers private banks in the current scenario over PSU banks.

"In the current scenario, I would lean towards private banks due to their stronger growth prospects, better margins, higher credit quality, and effective use of technology. Private banks have consistently outperformed PSBs in deposit mobilization and capturing higher-yielding consumer loan segments. While PSBs have improved their asset quality and provisioning, their core profitability still lags behind their private counterparts," she said.

Her top picks in this space are -

Kotak Mahindra Bank: Strong profit growth, robust retail lending, healthy margins, and stable management make it an attractive long-term investment.

HDFC Bank: A consistent performer with a well-diversified loan book, strong asset quality, and a history of delivering robust returns to investors.

ICICI Bank: With its focus on retail banking and digital innovation, ICICI Bank has turned around its performance, delivering strong growth and improving asset quality.

Rahul Malani, Banking and NBFC Analyst, Sharekhan, by BNP Paribas, likes PSU banks over private banks.

Malani noted that in the past 2-3 years, loan growth has been driven by majorly retail loans and now RBI has also taken a rate hike pause. On the backdrop of that, he believes that the credit to large industries/corporates is expected to pick up gradually driven by capex-led demand.

According to Malani, PSU banks still have a higher share of corporate loans than private banks and thus should benefit them disproportionately. Also, in terms of margins outlook, PSU banks have a higher share of MCLR linked book where incremental rates hikes have been passed lower compared to EBLR linked book, so PSU banks have still greater room for improvement in margins, he added. Further, the liability franchise continues to remain strong for top PSU and top private peers; and the asset quality outlook remains stable to positive for the sector in the near to medium term, he stated. However, Malani believes PSU banks still have scope for improvement in core RoA trajectory.

Top preferred picks in PSU banks: SBI & PNB; private banks: ICICI Bank, Axis Bank, HDFC Bank, Kotak Bank, Federal Bank & AU small finance Bank.

Nirav Karkera, Head of Research at Fisdom, stated that over the years, both public and private sector banks have worked towards strengthening their financial positions, resulting in significant improvements in their gross and net non-performing asset ratios. Several banks, both private and public, have demonstrated remarkable growth as a result of their efforts.

Therefore, he advised that instead of filtering banks based on ownership, one should evaluate them based on their balance sheet strength and improvement in their profit and loss accounts. This approach can provide a more accurate picture of a bank's financial stability and growth potential, stated Karkera.

While the largest four private sector banks and the largest public sector banks are expected to retain market leadership for quite some time, there are growth opportunities available even beyond it, he mentioned.

Here are Karkera's top picks within the banking sector:

1. Bank of Baroda: Bank of Baroda has established itself as one of India's leading public sector banks, with a substantial global loan book of around ₹9.2 lakh crore. Compared to other public sector banks, Bank of Baroda has demonstrated superior operating metrics, including net interest income (NII), asset quality, and loan growth.

The bank has positioned itself well to capitalise on growth opportunities, particularly in the retail loan segment. It has seen a gradual improvement in loan growth thanks to a healthy recovery in its corporate book. Bank of Baroda has also delivered impressive financial results, reporting a 15 percent increase in profit after tax (PAT) in Q3FY23.

The bank has significantly improved its asset quality, with its net non-performing asset (NPA) standing at less than 1 percent. Bank of Baroda has adequate provision cover for its existing stressed assets, further strengthening its financial position. Additionally, the bank has sustained improvement in the cost-to-income ratio (CIR) over the past three quarters.

Despite potential challenges such as a higher deposit cost, Bank of Baroda's strong financial position and favorable growth prospects make it a bank with long-term potential for growth and profitability.

2. Federal Bank: Federal Bank is a top pick in the banking portfolio due to its impressive growth performance since the COVID-19 pandemic. "The bank's focus on high-margin portfolios, including credit cards, personal loans, and digital partnerships, has resulted in solid financial results. We are also impressed with the bank's "lite branch heavy distribution model," which emphasizes a leaner branch network and increased use of digital channels to improve customer reach and service quality while reducing costs," it said.

The bank continues adding more fintech players to its ecosystem, and its existing partnerships have contributed significantly to its business. “We expect these partnerships to continue to drive growth, especially after the bank's recent launch of its first personal loan partnership with PaisaBazaar, aimed at enhancing lending business, mainly in the unsecured segment,” it added.

Federal Bank has shown remarkable improvement across most of its financial indicators, with solid momentum in credit growth across all verticals. The bank has also demonstrated excellent asset quality and net interest margins, delivering multiyear high ROA & ROE for the investors. The net interest income and fee income of the bank also grew substantially.

With plans to add more branches in CY23 and the maturation of its fintech partnerships, Federal Bank's journey will likely result in higher shareholder value over time. It is worth noting that Federal Bank has raised money only once in the last 2-3 years, demonstrating its strong financial position.

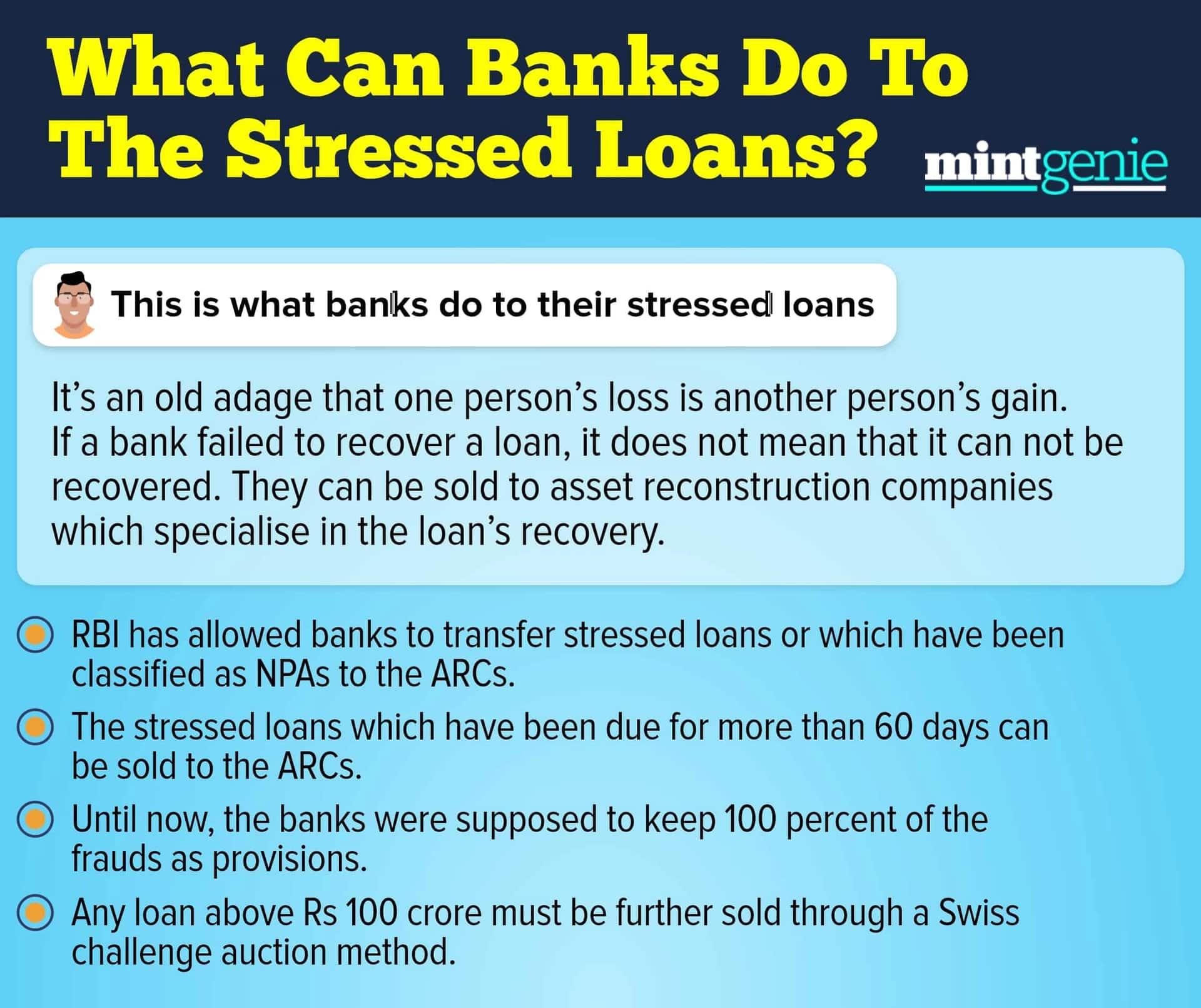

We explain what can banks do to the stressed loans.

First Published: 16 May 2023, 04:28 PM IST