The Indian pharmaceuticals sector has been under pressure from the ongoing Russia-Ukraine war as a majority of pharma companies have a strong presence in both countries.

Q4 Results Preview: Margins of Pharma companies likely to remain under pressure in the March quarter

TL;DR.

According to industry experts, high raw material and logistics costs will reduce EBITDA and PAT margins in the fourth quarter of FY22.

In addition, Indian pharmaceutical majors like Dr. Reddy’s Laboratories and Sun Pharma have a strong presence in Ukraine and Russia.

Experts believe the industry will deliver a modest earnings performance in the March quarter.

Axis Securities anticipates that pharma companies in its coverage universe will post a single-digit growth of 6.2 percent year on year, led mostly by the injectable and generic segments. With elevated prices of organic chemicals and solvents due to the Russia-Ukraine conflict, persistently high API/KSM costs from China that have risen 7-8 percent QoQ in Q4FY22, and near-normal A&P spending for the India market, we expect EBITDA margins of Pharma companies to remain under pressure, says the report.

The report estimates EBITDA in 4QFY22E to be sequentially lower for the majority of Indian generic pharma companies on account of lower gross margins due to an increase in raw material costs and sustained price erosion in the US at 5%-6% YoY during the quarter.

Indian Market

"The India Pharma Market (IPM) grew by 3.9% YoY in Q4FY22 as a volume decline of 3.3% YoY was offset by a price growth of 5.3% and new introduction growth of 1.8% YoY. Among acute segments, while the anti-infective segment declined by 4% YoY, Chronic segments remained muted as cardiac grew 4% YoY, anti-diabetic was up 2% YoY and CNS grew 3.4% YoY. Other key segments such as the Respiratory segment witnessed a growth of 27% YoY while Vitamins and Derma declined by 1.5% and 4% YoY respectively. However, India-focused players like Abbott India may do well as they are gaining market share in the domestic market," says Axis Securities in a report.

US Market

It expects a muted quarter for the US business like most companies, owing to continued price erosion and limited new launches (except Lanreotide for Cipla and Vasostrict for Dr. Reddy’s).

Logistic costs are also likely to impact the margins in the US business as Indian companies export products from India to the US, says the report.

Hospitals

Axis Securities prefers HCG and KIMS from the hospital sector, as it believes that they have robust balance sheets and leadership in their respective therapies. The hospital sector has performed relatively better than the overall industry owing to its lower base due to COVID-19 and a significant consumer preference shift from unorganised to organised healthcare services given integrated platforms, it added.

ICICI Securities, on the other hand, estimates pharma companies to post YoY growth of 7%–44,593 crore.

It expects the Select pack of domestic formulations to grow 11% year on year to 10,609 crore, owing to price increases, continued traction for acute therapies, a pick-up in chronic demand, and a small increase in Covid induced sales.

The report estimates Divi’s Lab, Biocon, Ipca, and Sun Pharma are likely to report 10%+ YoY growth.

ICICI estimates revenues for Ajanta Pharma to grow 8% YoY to 817 crore on the back of 13% growth in domestic business and 6% growth in exports. EBITDA is likely to decline by 13% YoY to 225 crore. Adjusted PAT is expected to increase by 6% YoY to 168 crore, it says.

It expects revenues for Alembic Pharma to decline 5% YoY to 1216.3 crore, as 21% growth in domestic formulations to 433.2 crore is likely to be offset by a 19% decline in US revenues to 382.7 crore.

The report estimates revenues for Biocon are likely to grow by 25% YoY to 2292.9 crore, mainly due to 45% expected growth in the biosimilar segment to 959.6 crore and 7% growth in Syngene to 703.6 crore. EBITDA margins are expected to improve by 81 bps YoY to 24.5%, it added.

"We expect Divi's Lab to grow 29% YoY to 2302.2 crore, mainly due to a likely 75% growth in the custom synthesis segment to 1251.7 crore. "According to ICICI Securities, EBITDA margins are expected to remain healthy at 42.4%."

The report estimates revenues for Dr Reddy's are likely to grow 6% YoY to 5062.5 crore, mainly due to 11% growth in domestic formulations to 937.4 crore and 12% YoY growth in US business to 1951.2 crore.

For Lupin, it anticipates revenues to grow 7% YoY to 4040 crore, mainly driven by 10% growth in domestic business to 1408.8 crore and 4% growth in the US to 1552.9 crore. EBITDA margins are expected to fall 535 basis points year on year to 13.4%.

Further, it projects revenues for Sun Pharma will grow by 11% YoY to 9459 crore, mainly on the back of 12% growth in domestic formulations to 2991 crore.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

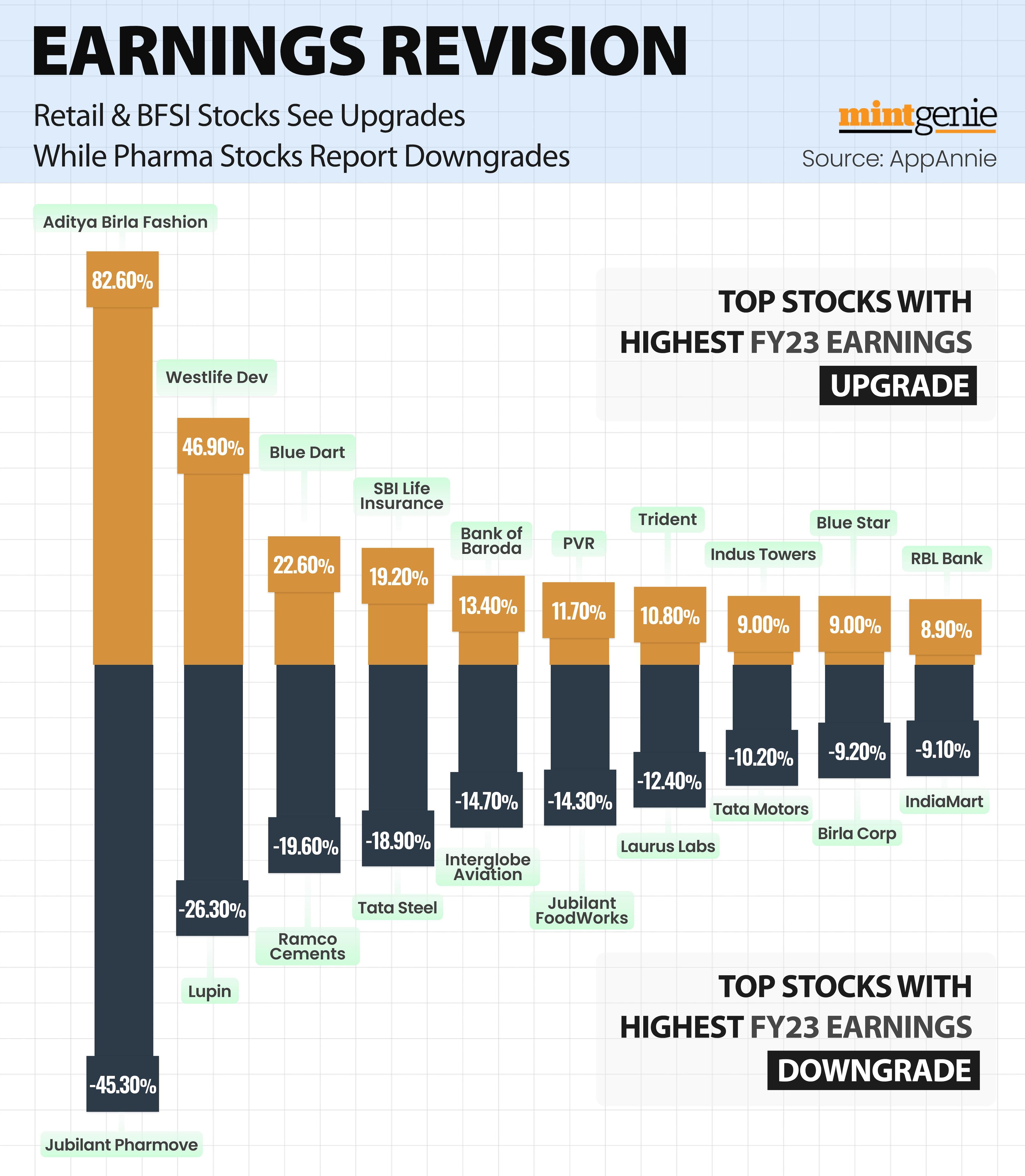

Earnings revision: Retail, BFSI sees upgrades, while pharma stocks sustains downgrades

First Published: 20 Apr 2022, 09:18 AM IST