Earlier this month, Uttar Pradesh revised its liquor excise policy. Alcohol is set to become expensive in the state from 1st April, 2023. Under the new excise policy, the licensing fee for shops and model shops has been raised by 10 percent. The new rules also mandate a 10 percent increase in the minimum guarantee quota.

Radico Khaitan vs Globus Spirits: Which liquor stock is a better long-term investment?

TL;DR.

From a long-term perspective, let's find out which liquor stock between Radico Khaitan and Globus Spirits is a better investment.

On the back of this development, liquor stocks have been in focus lately. But from a long-term perspective, let's find out which liquor stock between Radico Khaitan and Globus Spirits is a better investment.

Stock price trend

While Radico Khaitan has risen nearly 25 percent in the last 1 year, Globus Spirits has lost nearly 40 percent of its investor wealth in this period.

In 2023 YTD, Radico has risen nearly 14 percent as against a 4 percent decline in Globus.

Radico rose 3 percent in Feb so far followed by an 11 percent rise in Jan. In 2022, it shed 18 percent.

Globus, on the other hand, has been flat but in the green in Feb so far after a 4.5 percent decline in Jan. In 2022, the stock lost 35 percent.

Radico Khaitan stock price trend

About the firms

Globus Spirits is primarily engaged in the business of manufacture and sale of Indian Made Indian Liquor (IMIL), Indian Made Foreign Liquor (IMFL), bulk alcohol hand sanitizer and franchise bottling. Its business segments are divided into manufacturing and consumer business. The company’s current brands include Governors Reserve Premium Grain Whisky, Governors Reserve 100 percent Finest Grain Whisky, Oakton Barrel Aged Rare Finest Grain Whisky, Laffaire Napolean Premium French Blended Grape Brandy and Terai Craft Gin. It was incorporated in the year 1993 and is a small cap company.

Radico Khaitan is engaged in the manufacturing and trading of alcoholic products, such as Indian-made foreign liquor (IMFL) and country liquor. It offers various brands, such as Jaisalmer Indian Craft Gin, Rampur Indian Single Malt Whisky, Magic Moments Vodka, After Dark Premium Whisky, Morpheus Blue XO Brandy, 8PM Whisky, Pluton Bay Rum, Whytehall Premium Brandy, Regal Talons Premium Grain Whisky, Old Admiral Brandy and Contessa Rum. It has two distillery campuses located in India. It operates a total of over 33 bottling units across India, including five owned and operated by the company. It also operates approximately 75,000 retail outlets and 8,000 on-premises shops.

Q3 Earnings

In the December quarter, Globus Spirits' net profit fell over 11 percent to ₹27 crore as against ₹30.5 crore in the year-ago period. However, its total income jumped 48 percent to ₹810 crore versus ₹547 crore in the same period last year. The firm's total expenses came in at ₹755 crore, up over 50 percent in the third quarter of FY23, from ₹489 crore a year ago.

Globus Spirits stock price trend

Meanwhile, Radico Khaitan on Tuesday reported a decline of 22.63 percent in its consolidated net profit at ₹61.22 crore for the third quarter ended December 2022, on account of commodity inflation impacting margins. It had posted a consolidated net profit of ₹79.13 crore in the October-December quarter a year ago. Its revenue from operations was down 3.97 percent to ₹3,166.19 crore during the quarter under review as against ₹3,297.24 crore in the corresponding quarter of the previous fiscal. Radico Khaitan's total expenses were at ₹3,092.49 crore, down 3.30 percent in the third quarter of FY23, as against ₹3,198.30 crore a year ago.

Which is a better investment?

Kaustubh Pawaskar, DVP Fundamental Research at Sharekhan by BNP Paribas, likes Radico better.

"Radico Khaitan is consistently growing ahead of the industry due to strong traction to its premium products in the domestic market, which is scaling up well in key markets. Volatile raw material prices will keep up the pressure on the margins in the near term. However, price hikes in key states, benefits of backward integration and better mix would help margins to gradually recover from H1FY2024. Thus with a large focus on premiumisation coupled with expected benefits coming from backward integration augurs well for Radico Khaitan from a long-term perspective," it rationaled.

Meanwhile, Sharekhan has a neutral view on Globus. It lowered earnings estimates for FY2023/24/25 to factor in lower than earlier expected operating margins due to the effect of higher raw material cost and incremental losses in IMFL business.

Vinit Bolinjkar- Head of Research - Ventura Securities, believes headwinds for both companies remain strong in the near term but in the longer frame, both companies are expected to do well.

Bolinjkar noted that Radico’s Q3FY23 Revenue growth was robust mainly due to growth in the Prestige and Above( P&A) segment. As per the latest conference call, the company has already commissioned the dual feed plant at Rampur as well as the bottling operations at their Sitapur plant, it informed. This backward integration would further enhance the company’s EBITDA margins and as most of the CAPEX is already incurred, the company is expected to turn net cash positive soon, expects Bolinjkar.

On the other hand, he also pointed out that Globus Spirits is currently focusing on improving its margins. Q3FY23 margins stood at 10.1 percent vs 9.7 percent in Q2FY23, on account of higher Bulk Alcohol realization from ₹58.5 in Q2FY23 to ₹60 per litre in Q3FY23.

"With the coal prices cooling off, margins are further expected to increase in the grain-based ethanol segment, however in Q4FY23, the grain prices are further expected to increase. Capacity utilization at the Samalkha facility was below the optimal level, although improving QoQ. (Capacity utilization Q3 FY 22- 54 percent; Q2 FY 23- 67 percent, and Q3 FY23-79 percent). Improving capacities along with increased utilization, by FY25 the company will have access to 100 million cases per annum Consumer market (combined market size of all the GSL states). Management has also guided that Margins would remain in the range of 13-15 percent," he explained.

Harsh Sheth, Research Analyst, HDFC Securities, said he remains positive about Radico’s constant product innovation and success in the luxury portfolio. However, with the overall slowdown in consumption, the demand for the mid-price segment will remain muted, Sheth cautioned. Capex execution and margin recovery remain key monitorable for the stock, he added.

"Radico’s journey since FY17 has been remarkable, with continuous expansion in the P&A business, share gains, improving operating margins, deleveraging of the balance sheet, and improving FCFs. It certainly improved our confidence in the business and we consistently re-rated our valuation multiples. As the company returns to being asset-heavy (2x of the gross block, a debt of ₹541 Cr), we see the rerating journey to consolidate. This journey from being asset-light to being asset-heavy is taking place in an industry that has historically seen several headwinds. Thereby, it is adding to the risks in many ways," stated Sheth.

"In Q3FY23, Radico delivered a miss on both revenue and EBITDA despite a beat in P&A revenue. Net sales were up by 5 percent YoY with flat IMFL volume (three-year CAGR at 3 percent). Gross margin was flat QoQ but contracted by >400bps YoY to 41.3 percent. EBITDA margin was down by 350bps YoY to 12.2 percent. EBITDA contracted by 19 percent YoY — a fifth quarter of weak performance," informed Sheth.

With investments in backend capabilities, he modeled recovery in EBITDA margin to 15.5/16.5 percent in FY24/25 (cautious for downside risk).

On account of consistent miss in margin and weak show for the regular portfolio, HDFC cut EPS for the stock by 7 percent for FY23/FY24.

Sector outlook

The Indian Ethanol (also called Ethyl Alcohol) market is projected to expand aggressively in the forecast period on the back of increased Ethanol consumption in fuel additives and beverages, predicted Bolinjkar of Ventura. Moreover, heavy investments made by the Government of India towards converting excess sugar to Ethanol, further strengthened by the government's vision to create an Ethanol Economy, will accelerate the Ethanol demand in the forecast period, he added.

"With the start of National Biofuel Policy 2018, which has put forth an Ethanol blending target of 10 percent by 2022 and 20 percent by 2030 from the current rate of 2-3 percent, Ethanol demand is set to grow by leaps and bounds in the period of forecast. Over the past five years, the Indian government has been encouraging Ethanol capacity expansion to cut its dependency on imported crude oil and channelize the excess sugar inventories into Ethanol production. These factors will further propel the growth of the Ethanol market in India," he explained.

Pawaskar also predicted that growth in the Indian Manufactured Indian liquor (IMFL) is expected to be driven by a growing consumer base, conducive regulatory policies at the state level, and a sharp shift to premium brands in the liquor space in the coming years.

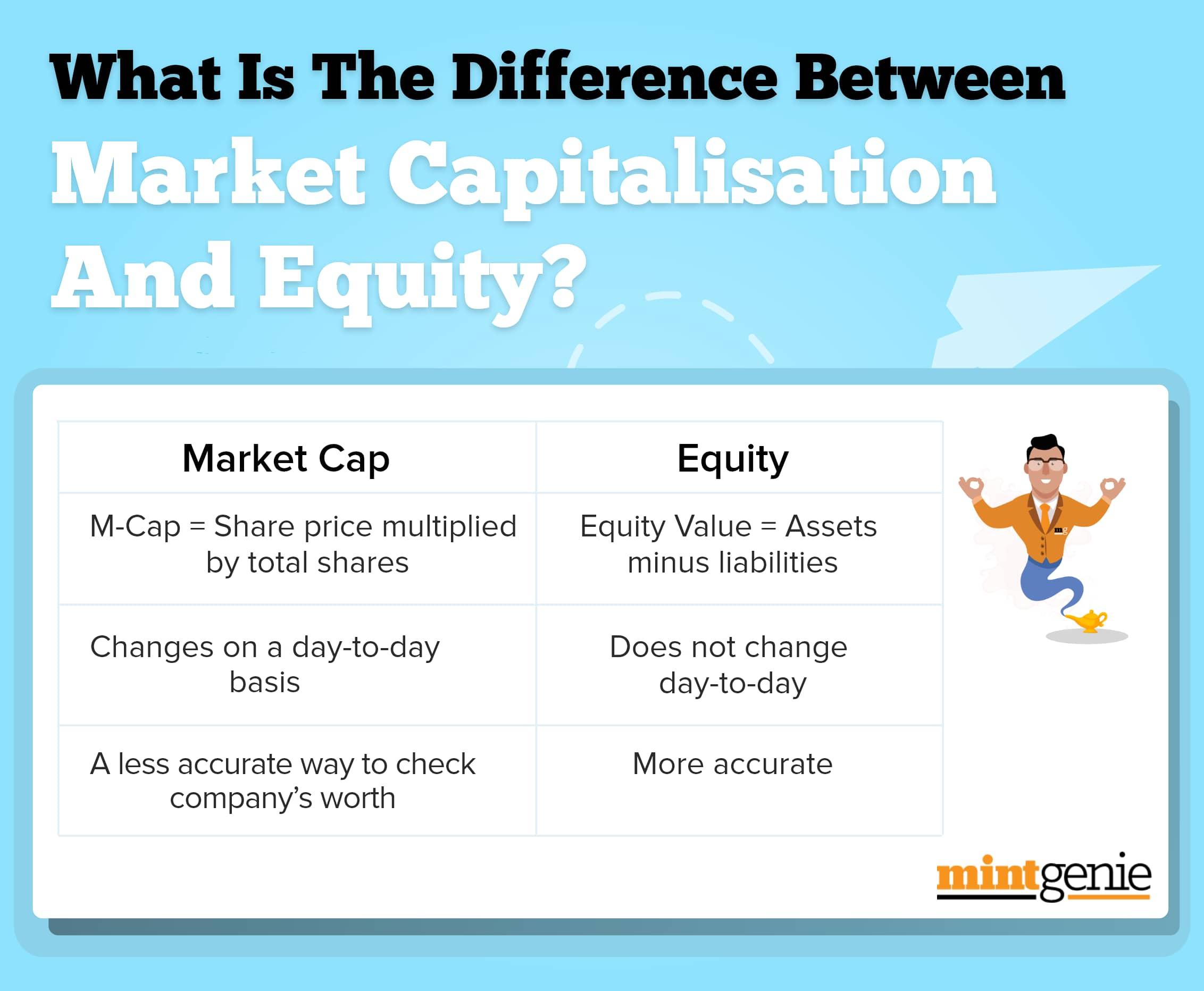

Market cap vs equity

First Published: 24 Feb 2023, 01:50 PM IST

Related Stories

Explain Like I am 5

personal finance

Equity vs real estate: Which will yield better returns in the long term?

Team MintGenie