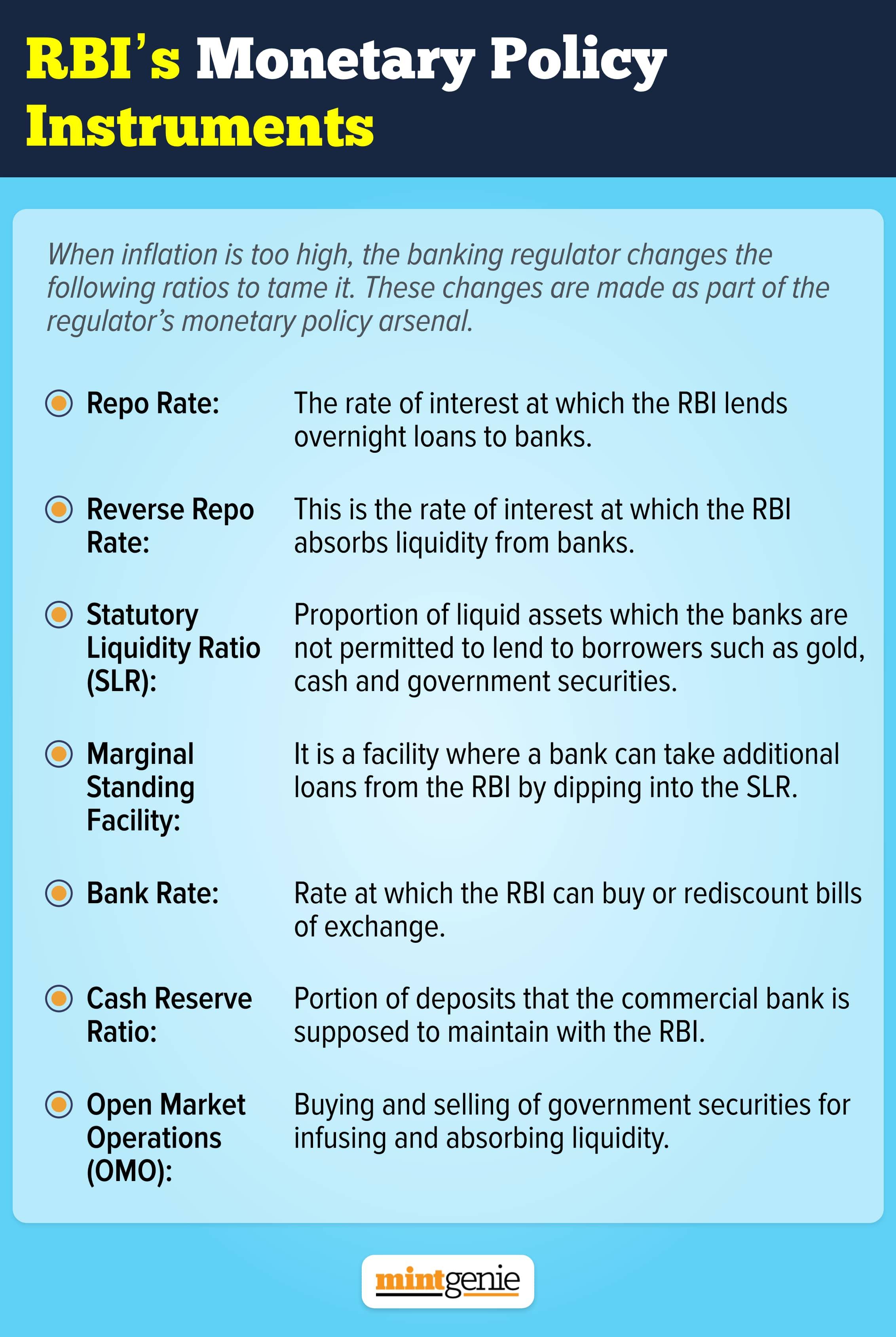

The Reserve Bank of India (RBI) on May 4 surprised many by hiking the repo rate by 40 basis points (bps) to 4.40 percent with immediate effect. It also raised Cash Reserve Ratio (CRR) by 50 bps to 4.50 percent effective May 21.

"We have demonstrated in the MPC that we are not bound by a set book of rules but be accommodative of changing scenarios," said Das.

As inflation is soaring and expected to remain elevated, an interest rate hike of 25-50 basis points was long overdue and while it may keep the mood of the market subdued for some time as it impacts investors' saving and investment cycle, from a long-term perspective, it may help banks & NBFCs in terms of better margins and growth in the next few quarters.

Many experts think the rate hike will have a short-term negative impact on the market. We have collated the views of many experts. Take a look:

Unmesh Kulkarni, Managing Director Senior Advisor, Julius Baer India

RBI's decision shows RBI's commitment to tackle inflation, which has been ruling high and at the higher end of RBI's comfort zone. Also, given the expectations of a 50 bps rate hike by the US Fed, RBI possibly wants to pre-empt the Fed action, in order to ensure stability in the currency and capital flows.

The CRR hike is a further step in RBI's liquidity normalisation drive, as it attempts to tame the persistently high inflation.

While RBI is committed to ensuring sufficient liquidity, the policy stance looks to have already changed to neutral-to-hawkish, which it may officially announce at the June MPC meet.

Given the enhanced government borrowing calendar this year, RBI has a tough job at hand, to manage the market's expectations of yields while seeing the weekly auctions through in a non-disruptive manner.

Lakshmi Iyer, Chief Investment Officer (Debt) & Head Products, Kotak Mahindra Asset Management Company

Bond markets witnessed surgical strike moments with a surprise 40 bps repo rate hike and 50 bps CRR hike. Inflation racing ahead of expectation seems to be the key trigger for this unanimous inter-meeting decision.

A combination of weaning off liquidity and expectations of continued rate hikes could mean sustenance of elevated bond yields. Global factors also act as headwinds for yields, as US impending rate hike also weighs in.

Sujan Hajra, Chief Economist and Executive Director, Anand Rathi Shares & Stock Brokers

The surprise mid-cycle rate hike by the RBI is driven by factors such as inflation concern (Mar’22 inflation nearly 100 bps higher than expected and another surprise high inflation rate now expected in Apr’22), the perception that the RBI is falling behind the curve, external sector pressures (capital outflow, higher trade deficit, weaker rupee) and the likelihood of 50 bps rate hike by the Fed.

By setting the interest rate on the newly introduced SDF rate at 40bps higher than the reverse repo rate, the RBI effectively increased the policy rate by 40 bps in the April’22 policy. Today’s rate hike makes the effective rate higher by 80 bps.

The simultaneous 50 bps CRR hike would tighten liquidity (By ₹90,000 crore immediately), which would improve the transmission of the rate hike in the credit and debt market.

We expect an immediate increase in the money market rate, some transmission in the long-term bond market and also the credit market (both lending and deposit rates). The impact on the equity market is likely to be negative in the short term.

Suvodeep Rakshit, Senior Economist, Kotak Institutional Equities

The combination of a 40 bps hike in repo rate and a 50 bps hike in CRR is an attempt by the RBI to preempt the rising inflationary pressures and be ahead of the curve. The bigger surprise was the CRR hike which indicates the RBI’s intent on withdrawing liquidity at a sharper pace.

While inflation is unlikely to decline in the near term, today’s move should help in pushing real rates towards neutral over the next few quarters. Rates across the curve will reprice factoring in a markedly more hawkish RBI. We continue to expect cumulative 100-125 bps of repo rate hikes in FY2023.

Aditi Nayar, Chief Economist, ICRA

Today's surprise repo rate and CRR hikes are very well-timed, as our own CPI inflation projection for April 2022 is an eye-watering 7.4 percent. By advancing the rate decision by approximately one month, the MPC has focused on preventing inflationary expectations from unanchoring in an increasingly uncertain environment. The Committee has displayed its nimble-footedness and clearly completed the pivot back to inflation management.

If the US Fed's decision tonight is more hawkish than expected, then the 10-year G-sec yield could test 7.5 percent as early as tomorrow; this is the cap that we had foreseen for H1 FY2023.

As of now, we see a higher base softening the May 2022 CPI inflation print considerably, although it will likely remain above 6 percent. While a back-to-back hike in the June 2022 policy is not yet certain, we do foresee an additional 35-60 bps of rate hikes in the remainder of H1 FY2023. If a de-escalation in geopolitical tensions cools commodity prices, then we expect a pause to reassess the impact on growth, followed by another 25-50 bps of rate hikes in CY2023.

VK Vijayakumar, Chief Investment Strategist at Geojit Financial Services

The MPC's decision, in an unscheduled meeting, to raise the repo rate by 40bp and CRR by 50 bp is a surprise since it came on the LIC IPO opening date. MPC's proactive move is justified from the perspective of inflation management, but the timing leaves a lot to be desired. The above 1000-point crash in Sensex has soured the sentiments on the opening day of India's largest IPO. The 10-year bond yield has spiked to above 7.39 percent indicating an imminent rise in the cost of funds.

Ajit Kabi, Banking Analyst at LKP Securities

RBI has raised the repo rate by 40bps with immediate effect and CRR by 50bps by May 21. The rate hike was much-anticipated factoring rise in food and general inflation. The rate hike is likely to shrink liquidity in the economy overall. As per as the banks are concerned the cost of funds is likely to increase so does the cost of deposits. It may translate into NIMs pressure. However, a quick increase in MCLR may control the NIMs squeeze.

Parth Nyati, Founder, Tradingo

This sudden hawkish move has been taken against the backdrop of retail inflation persistently staying above the central bank's comfort zone. This will be negative for rate negative sectors like banking, NBFCs, automobiles, real estate, etc in the short term.

The current inflation is due to supply-side pressures not from the demand side, and many businesses haven’t reached the pre-Covid levels, hence the market was expecting a rate hike in the next meeting.

Nevertheless, the interest rates are still near all-time lows, this conservative move will give RBI an upper hand in fighting inflation, this decision also removes the overhang from the financial markets, so we are still positive on the market from a medium to long term perspective.

Sorbh Gupta, Fund Manager- Equity, Quantum AMC

RBI’s surprise move on increasing the repo rates today is an acknowledgment of inflation becoming a more important variable in policy decisions than growth.

It will not have an immediate bearing on growth in inflation but it is an indication of things to come. These types of events will come and go multiple times in an investor’s journey to achieving financial goals & one should not be swayed too much.

An equity portfolio stress-tested for balance sheet strength (lower leverage) and attractive valuations of investee companies is well suited for this environment. Investors should stick to their asset allocation plans and use a staggered approach to increase allocation to equities.

Honeyy Katiyal, Founder, Investors Clinic

The Indian real estate market performed much better than other sectors post-pandemic. The sector was supported with steady rates and plenty of housing inventory which was cleared after Covid.

The rate hike was expected to be in line with the global central banks' move, to control inflation which is required for the masses. This is primarily because inflation is very high and affects the household budgets. Most importantly, we do not see banks immediately passing on the increased rates to consumers.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies and not of MintGenie.