The new set of regulatory actions by the RBI pertaining to the capital account comes after recent policy curbs on exports and imports and the RBI’s consistent intervention in all currency trading spaces to signal its support to the Indian rupee (INR), which went as low as 79.35 this week.

We had earlier argued that dislocation in forwarding rates (which seem to have corrected somewhat), falling forex (FX) cover, high commodity prices and CAD funding risks mean that the RBI’s intervention strategy cannot be the sole support for INR and will soon face limitations.

To that extent, further complementary monetary and fiscal corrective measures in the form of trade curbs or regulatory changes are needed to address the looming pain on the BoP, and the external imbalances thereof.

Not material change in flows but certainly helpful in directional FX signalling to speculators

While these measures to boost capital accounts are helpful, they may not have a material impact on flows. Nonetheless, they will still ease the pressure on the RBI to intervene to some extent.

Firstly, the 2013 FCNR swap scheme saw both the FX risk borne by the RBI and a highly subsidised swap rate as well, making mobilisation of “leveraged” FCNR deposits by (foreign) banks highly lucrative, leading to banks raising more than 3 times of the initially expected amount of $10bn through the scheme.

We are unlikely to see the same zeal this time around. However, with low forward premia, this mobilisation may still make some sense for banking entities.

We reckon the timing of RBI’s move today coincides with the typically strong remittance/deposit season that comes with the beginning of the festive season. This can take the pressure off banks to raise domestic deposits amidst accelerating credit growth, and also somewhat cool-off domestic borrowing rates.

Secondly, easing all the available channels of FPI investments in debt may not lead to a material change in FPI flows given the free limits that are already available. However, the new tenors added in Fully Accessible Route (FAR) securities are fairly active.

Thirdly, the all-in cost ceiling under the ECB framework is also being raised by 100 bps, subject to the borrower being of investment grade rating, however, we seek more clarity on this front as to whether it leads to any change in caps (from existing 450bps), and if it makes sense for domestic good investment-grade borrowers to borrow in foreign currency, except when they are facing a credit crunch back home.

In all, these measures, while having a slight sense of deja vu from 2013, are still proactive, rather than the reactive measures taken back then. While it is debatable if these steps can lead to significant flows, they could be effective in preventing speculative attacks on the currency and giving directional policy signals to the markets.

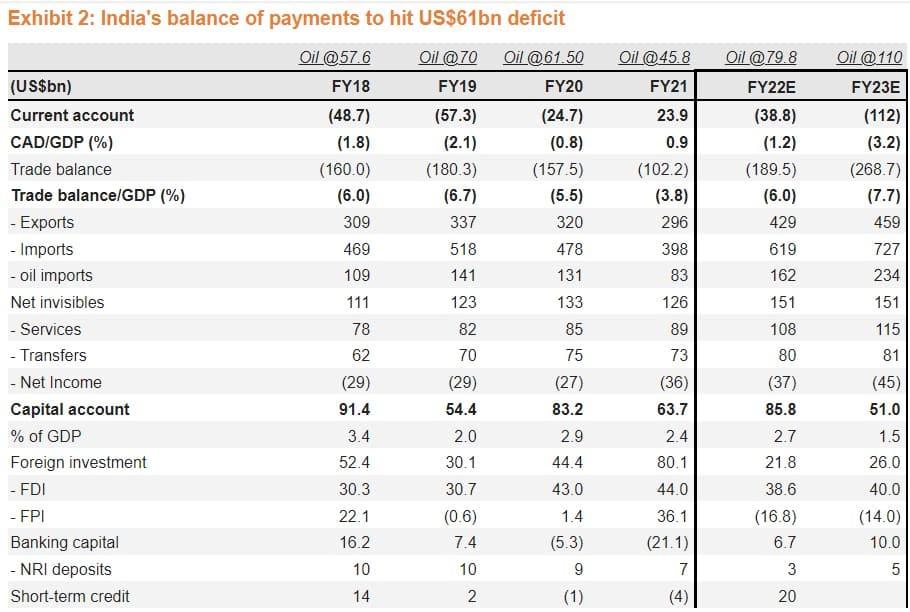

As of now, we see a sharp BoP deficit of US$61bn, CAD/GDP at 3.2 percent (US$112bn) in FY23E and basic BoP deficit (CAD+FDI) worsening to levels seen last in 2013. However, we will revisit these as things evolve. That said, we think the peak of CAD/GDP is behind us in Q1FY23 (around 3.8-3.9 percent).

Assuming commodity prices stay at current levels, the CAD is expected to gradually narrow from here but still remain elevated at above 3 percent of GDP for the next two quarters. We believe the RBI should eventually let the exchange rate adjust to new realities, albeit orderly, letting it act as an automatic macro stabilizer to the policy reaction function.

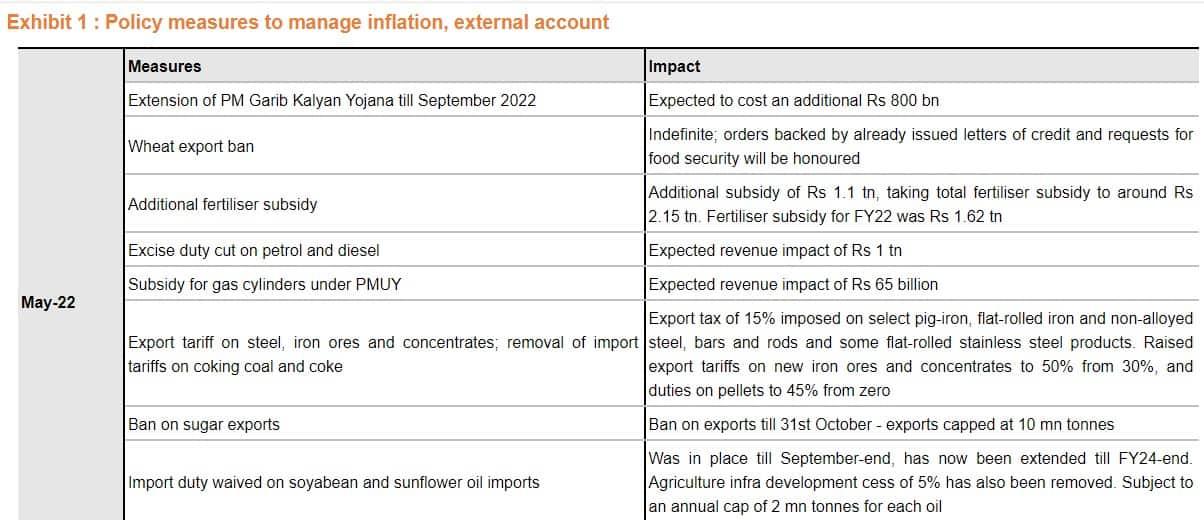

Key regulator measures announced on capital account:

CRR+ SLR exemptions: Incremental FCNR(B) and NRE deposit liabilities are now exempt from NDTL computation for maintenance of CRR and SLR. Transfers from NRO accounts will not qualify for this relaxation. This relaxation is available till 4th Nov’22.

Interest rates on FCNR and NRE deposits: Banks are temporarily allowed to raise fresh FCNR(B) and NRE deposits without having to adhere to the regulations on interest rates on these deposits.

FPI debt investment: Easing all the available channels of FPI investments:

(i) All new issuances of 7-year and 14-year G-secs (including fairly active current issuances of 7.10 percent GS 2029 and 7.54 percent GS 2036 ) to be now covered under Fully Accessible Route (FAR). At present, 5-year, 10-year and 30-year tenors are covered.

(ii) FPI investments in G-secs and corporate debt will not be subject to the short-term limit i.e. not more than 30 percent of investments in G-secs and corporate debt can have a residual maturity of less than one year.

(iii) FPIs can invest in CPs and NCDs with an original maturity of up to one year versus an earlier mandate of at least one-year. These investments will not be included as part of the short-term investment limit in corporate securities.

Foreign currency lending by banks: Banks can utilise overseas foreign currency borrowings (OFCBs) for lending for a wider set of purposes, not just export finance. The measure is expected to facilitate foreign currency borrowing by a larger set of borrowers who may find it difficult to directly access overseas markets.

ECB limits: The limit for ECBs under the automatic route has been raised from US$750 mn to US$1.5 bn per financial year. The all-in cost ceiling has also been raised by 100bps.

(Madhavi Arora is Lead – Economist at Emkay Global Financial Services)

Disclaimer: The views and recommendations made above are those of the author and not of MintGenie.