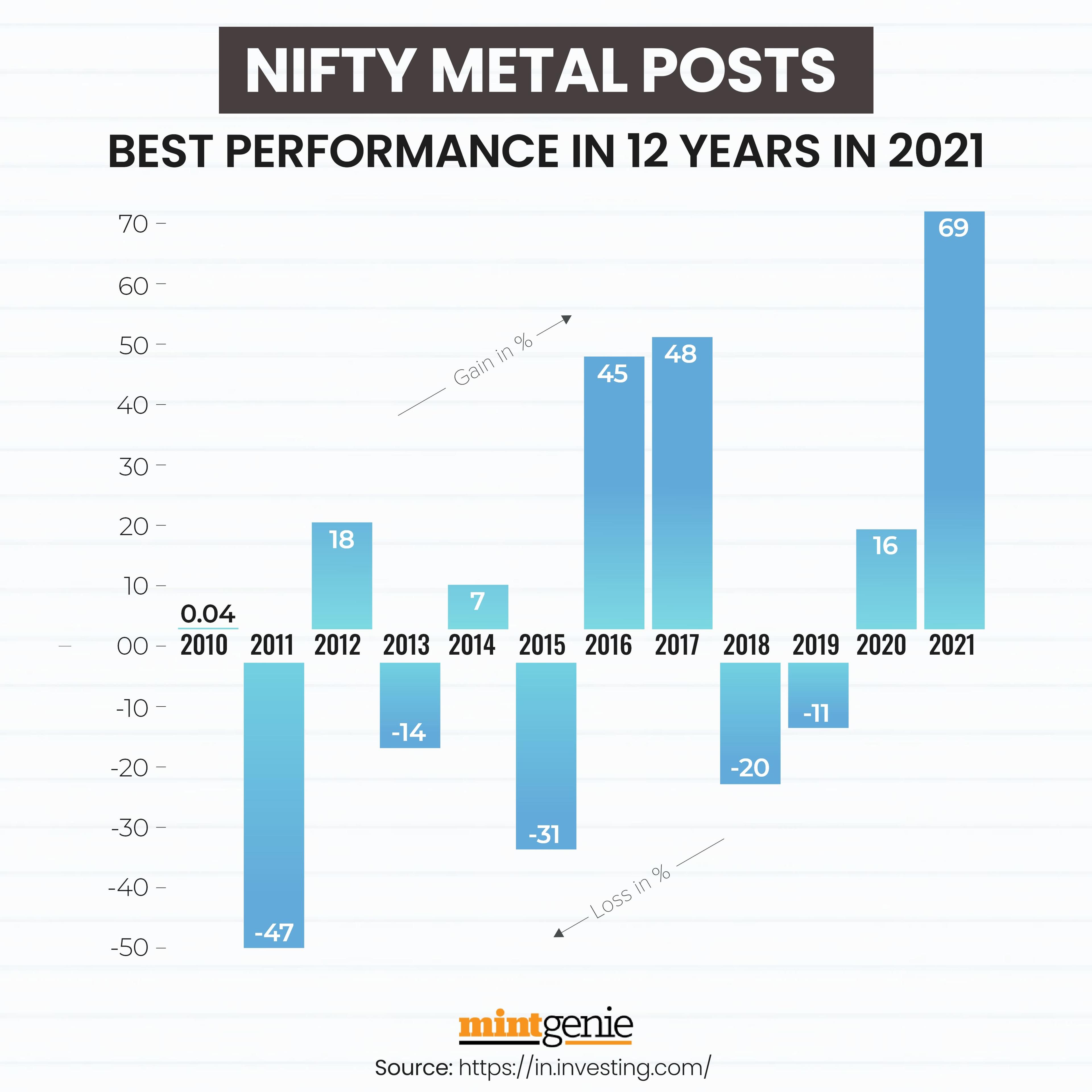

Steel companies will deliver robust Revenue/EBITDA growth on a year-over-year basis, primarily due to strong underlying commodity prices and robust sales volume as the companies optimise production and sales volumes to capture the share of higher prices, according to Axis Securities' report.

It expects that company's EBITDA margins will remain flattish or marginally decline YOY and QOQ, mainly due to higher coal and energy prices. Aluminium and steel prices rallied. Due to the supply disruption that emerged from the Russia-Ukraine conflict.

Coking coal prices for steel companies have jumped sharply which will impact the margins in Q4FY22. Power costs for aluminium smelters, too, are expected to go up due to the jump in coal prices. The rise in input raw material inflation will partially offset the gains from strong prices and sales volumes and will keep the margins flattish, said the report.

Furthermore, the report expects both steel and base metals prices to remain strong in upcoming quarters and companies will continue to deliver robust cash flows, while at the same time deleveraging their balance sheets.

“We expect steel prices to remain resilient in the short term. Regional steel prices have increased recently due to the escalated geopolitical conflict. Indian domestic HRC prices have increased by 10% MoM in the domestic market, 40% in Europe, 37% in the US, and 2% in China (export FOB price).

The steel price hike is sharp in Europe which incentivises the Indian steel mills for exports to the EU. China’s decarbonisation leading to lower steel exports is creating opportunities for Indian steel mills to fill the volumes. Coking coal prices have stood strong eating into the steel mills' margins, due to supply shortage from Australia. However, Apr’22 and May’22 coking coal contracts are pointing towards price correction,” the report added.

Earnings Estimates

For Hindalco's fourth quarter, Axis Securities estimates EBITDA to increase owing to higher sales realisation(which is partially offset by higher coal and energy prices). According to the report, EBITDA margins will improve year on year while falling slightly quarter on quarter due to higher coal and raw material prices (partially offset by higher LME prices). PAT and EPS will follow the EBITDA rise.

Tata Steel's revenues are expected to grow due to higher steel prices and steel deliveries. Tata Steel has released provisional production and deliveries. Group Steel deliveries are higher at 13% QoQ and 4% YoY. EBITDA is expected to marginally increase as the impact of higher raw material costs (coking coal) is offset by higher steel prices. Margin pressure due to higher coking coal prices EBITDA growth is broadly followed by PAT and EPS.

Revenue to rise on higher sales volumes and price realisation for APL Apollo tubes. The company registered a sales volume of 551,723 tonnes in Q4FY22, up 37% QoQ and 27% YoY. EBITDA to increase led by higher revenue and cost control, and a higher contribution from value-added products. Margins will improve year on year, driven by higher sales realization.

NALCO's EBITDA is expected to increase due to higher revenues and lower raw material costs. It expects lower caustic soda costs. The YoY increase is in line with higher realization.

The report added that there was a marginal improvement in EBITDA margins in Q4FY22 vs. Q3FY22 due to the assumption of lower caustic soda costs.

For SAIL, the report pegs revenue to increase on the back of higher saleable steel sales along with higher steel price realization. (Up 16% year on year, but down 3% quarter on quarter).

EBITDA is expected to fall YoY and increase QoQ, it said. The YoY fall would be mainly due to higher coking coal prices in Q4FY22. which have increased sharply (though partially offset by higher realization). The QoQ rise is mainly due to higher sales volume expectations in Q4FY22. In Q4FY22, coking coal costs are expected to increase by ₹1,000-2,000/tonne over and above the Q3FY22 costs.

EBITDA margins are expected to fall to 16% from 26% in Q4 FY21, in line with higher costs. According to the report, PAT and EPS should reflect EBITDA falling year on year and rising quarter on quarter.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.