As the impact of the pandemic continues to fade away, credit offtake in the financial system has been gathering momentum. The latest RBI data suggests a 2% sequential growth in March-June 2022, which is generally against the usual trend. However, with underlying demand being strong this time around, Q1FY23E is expected to be exceptional in terms of growth compared to the earlier corresponding years, said ICICI Securities.

Results Preview: Rising Treasury yields will hurt bank margins in Q1FY23

TL;DR.

The yield on the Indian 10-year government bond is currently trading at around 7.42%. Between April and June, the bond yield surged by 60bps to 7.42% on the back of recession fears and concerns over the fiscal deficit.

It anticipates that the banking industry's core earnings will remain strong, with strong in-advances, a healthy margin profile, and a decline in credit costs across lenders. However, ICICI Securities expressed concern over rising bond yields as it may affect the bank's margins in Q1FY23E. Last week, the yield on the Indian 10-year government bond fell to around 7.3%, the lowest in six weeks, data from Trading Economics shows. Still, the yield remained close to a 3-year high of 7.6% hit in June as high domestic inflation, increasing interest rate differentials, and weak external finances have been causing sustained foreign investor portfolio outflows. Meanwhile, the Reserve Bank of India liberalised rules for foreigners to invest in local currency bonds. So far this year, the RBI has raised interest rates by 90 basis points, to 4.9%, and experts believe this is set to increase in the coming months.

As a part of SLR (Statutory Liquidy Ratio), banks will maintain large holdings of government securities, including state development loans and treasury bonds. Any volatility in the bond market is expected to affect their treasury income.

The yield on the Indian 10-year government bond is currently trading at around 7.42%. Between April and June, the bond yield surged by 60bps to 7.42% on the back of recession fears and concerns over the fiscal deficit. However, the Indian government's recent windfall tax on fuel exports may provide some relief after May's excise duty cut on domestic fuel prices and a rise in fertiliser subsidies.

Indian 10- Year bond yiled - Between April and June, the bond yield surged by 60bps to 7.42%

Meanwhile, ICICI Securities said that the credit growth of its coverage universe is expected to be above industry at 16% YoY to ₹66.5 lakh crore, driven by retail (home, auto, and credit cards) and MSME segments. It expects NII to increase by 16% year on year, aided by healthy business growth and stable NIM. A better understanding of growth segments and a view on the sustainability of credit momentum should remain key, it added.

Deposit traction is expected to remain at 9% YoY with a slight improvement in CASA YoY, though QoQ CASA may decline. It said that NIMs are expected to be largely steady with some positive bias of 2-4 bps sequentially as banks have increased lending rates while deposit rates are expected to catch up with a lag.

“Asset quality is expected to be less concerning with confidence shown by the management as collection activity is showing improving trends. Stress behaviour in the MSME segment needs to be monitored as increasing interest rates and the end of the moratorium could have built up pressure. For our coverage universe, We believe GNPA should decline 10 bps QoQ to 3.4%.” ICICI Securities said.

The hardening of interest rates is expected to negatively impact treasury income, especially for PSU banks. However, banks have built up an investment fluctuation reserve, which could be used to offset losses, though the bank’s stance is to be seen, it added.

It said that the credit costs on a sequential basis should decline as asset quality improves. Also, in the last quarter, a few banks had taken excess provisions to strengthen their balance sheet and some for write-offs, which may not be the case in Q1FY23. Hence, The brokerage firm expects the PAT to report healthy growth of 37% to ₹27,975 crore due to a healthy topline show and low credit costs.

Q1 Preview of Public sector banks

ICICI Securities expects the Bank of Baroda to post credit growth of 18% to ₹7.9 lakh crore in Q1FY23E as credit on a YoY basis continues to gather pace. It estimated bank deposit growth to be at 15% YoY at ₹10.7 lakh crore, driven by CASA and NII to grow at 13.4% YoY to ₹8,945 crore. Further, it expects the bank's non-interest income to decline by 38% YoY, mainly on account of treasury losses as the interest rate hardens.

| Public sector banks ( ₹in Cr) | NII Q1FY23E | Change (%) | PPP Q1FY23E | Change (%) | NP Q1FY23E | Change (%) | |||

| YoY | QoQ | YoY | QoQ | YoY | QoQ | ||||

| Bank of Baroda | 8,945.8 | 13.4% | 3.9% | 5,267.6 | -6.0% | -6.5% | 1,384.9 | 14.6% | -22.1% |

| SBI | 32,258.4 | 16.7% | 3.4% | 19,891.5 | 4.8% | 0.9% | 7,741.7 | 19.0% | -15.3% |

| Total | 41,204.2 | 16.0% | 3.5% | 25,159.1 | 2.4% | -0.8% | 9,126.6 | 18.3% | -16.4% |

| Source: ICICI Direct Research | |||||||||

For State Bank of India, ICICI Securities expects loan growth of 12% YoY to ₹2,8190 billion and deposit growth of 10% YoY. Overall NII growth is seen at 16.7% YoY led by a pick-up in loan growth clubbed by higher interest rates. However, the rise in bond yields in Q1FY23 will increase the provision cost, it added.

Q1 preview of Private banks

The domestic brokerage firm expects the net interest margin to grow by 3.1 QoQ and 17.2% YoY to ₹9,094 crore for Axis Bank. It anticipates 18% YoY deposit growth for the axis, with a sequential 40 bps increase in the CASA ratio.

| Private Banks ( ₹in Cr) | NII Q1FY23E | Change (%) | PPP Q1FY23E | Change (%) | NP Q1FY23E | Change (%) | |||

| YoY | QoQ | YoY | QoQ | YoY | QoQ | ||||

| Axis Bank | 9,093.5 | 17.2% | 3.1% | 5991.3 | -3.2% | -7.3% | 3715.7 | 72.0% | -9.8% |

| Federal Bank | 1,641.0 | 15.7% | 7.6% | 815.2 | -21.4% | 2.1% | 536.1 | 46.0% | -0.8% |

| HDFC Bank | 19,203.1 | 12.9% | 1.8% | 16,169.7 | 6.8% | -1.1% | 9,720.9 | 25.8% | -3.3% |

| IDFC Bank | 2,756.3 | 23.2% | 3.3% | 727.3 | -23.9% | -12.0% | 277.0 | NA | -19.2% |

| IndusInd Bank | 4,063.5 | 14.0% | 2.0% | 3,311.7 | 5.8% | -0.5% | 1,450.6 | 48.8% | 6.6% |

| Kotak Bank | 4724.5 | 19.9% | 4.5% | 3,322.9 | 15.0% | -0.5% | 2,327.8 | 41.8% | -15.9% |

| Bandhan Bank | 2,569.4 | 21.5% | 1.2% | 2,418.4 | 24.8% | -4.1% | 728.9 | 95.4% | -61.7% |

| CSB Bank | 305 | 13.9% | 0.4% | 146.9 | -16.0% | 3.4% | 91.5 | 50.0% | -30.0% |

| Total Banks | 44,356.6 | 15.9% | 2.6% | 32,903.4 | 4.5% | -2.6% | 18,848.4 | 48.7% | -11.2% |

| Source: ICICI Direct Research | |||||||||

"HDFC bank, credit growth is expected to remain strong at 21.6% YoY to ₹13.95 lakh crore. Deposit growth is expected at 19% YoY and the CASA ratio is to be at around 46%. NII growth is expected to be 12.9% year on year to ₹19,203 crore, with margins remaining flat QoQ at 4%. Other income is expected to increase YoY, and asset quality is expected to improve QoQ, with GNPA hovering around 1.1%. Expect the provision to decline to Rs. 3208 crores. Thus, PAT growth is seen at 26% YoY to ₹9720 crore.”

Q1 preview of NBFC's

ICICI Securities expects Bajaj Finserv's revenue to grow at 25.8% YoY to ₹17,542 crore, led by a pick-up in the lending business coupled with continued healthy traction in premium accretion in the insurance business.

For SBI life insurance, the brokerage house estimates a healthy growth in premium accretion at 19% YoY to ₹9,852 crore, led by traction in non-par products for both individuals and groups.

| NBFC ( ₹in Cr) | NII Q1FY23E | Change (%) | PPP Q1FY23E | Change (%) | NP Q1FY23E | Change (%) | |||

| YoY | QoQ | YoY | QoQ | YoY | QoQ | ||||

| HDFC | 4,350.2 | 4.9% | -0.4% | 5,295.6 | 15.4% | 5.4% | 3,469.2 | 15.6% | -6.2% |

| Bajaj Finance | 6,315.8 | 40.7% | 4.2% | 4,156.2 | 33.4% | 4.8% | 2,469.2 | 146.3% | 2.1% |

| Bajaj Finserv | 17,542.3 | 25.8% | -7.0% | 3527.1 | 99.6% | 1.9% | 1,345.9 | 61.6% | 0.0% |

| SBI Life Insurance | 9,852.4 | 18.5% | -43.5% | 262.4 | 135.6% | -79.9% | 281.1 | 25.9% | -58.2% |

| HDFC Life Insurance | 9,189.2 | 21.9% | -35.7% | 270.7 | 357.3% | -51.0% | 371.5 | 22.9% | 3.9% |

| Muthoot Finance | 1,824.1 | 7.2% | 6.0% | 1361.5 | 2.1% | 11.4% | 996.6 | 2.6% | 3.8% |

| Star Health | 2,628.6 | 17.2% | NA | 196.3 | NA | NA | 142.2 | NA | NA |

| ICICI Lombard | 4,074.7 | 45.1% | 2.5% | -194.0 | NA | NA | 394.9 | 103.3% | 26.4% |

| Total | 56,347.0 | 23.0% | -16.3% | 15,303.3 | 45.1% | 18.7% | 9,793.3 | 47.0% | 32.9% |

| Source: ICICI Direct Research | |||||||||

The decline in COVID cases and base effect are expected to lead to a reduction in claims, leading to a surplus of ₹262 crore. Healthy premium accretion, steady efficiency and a decline in claims led to earnings growth of 26% YoY to ₹281 crore, it said. ICICI Securities stated that the guidance on VNB margins and increased competitive intensity in the non-par segment should be closely monitored.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

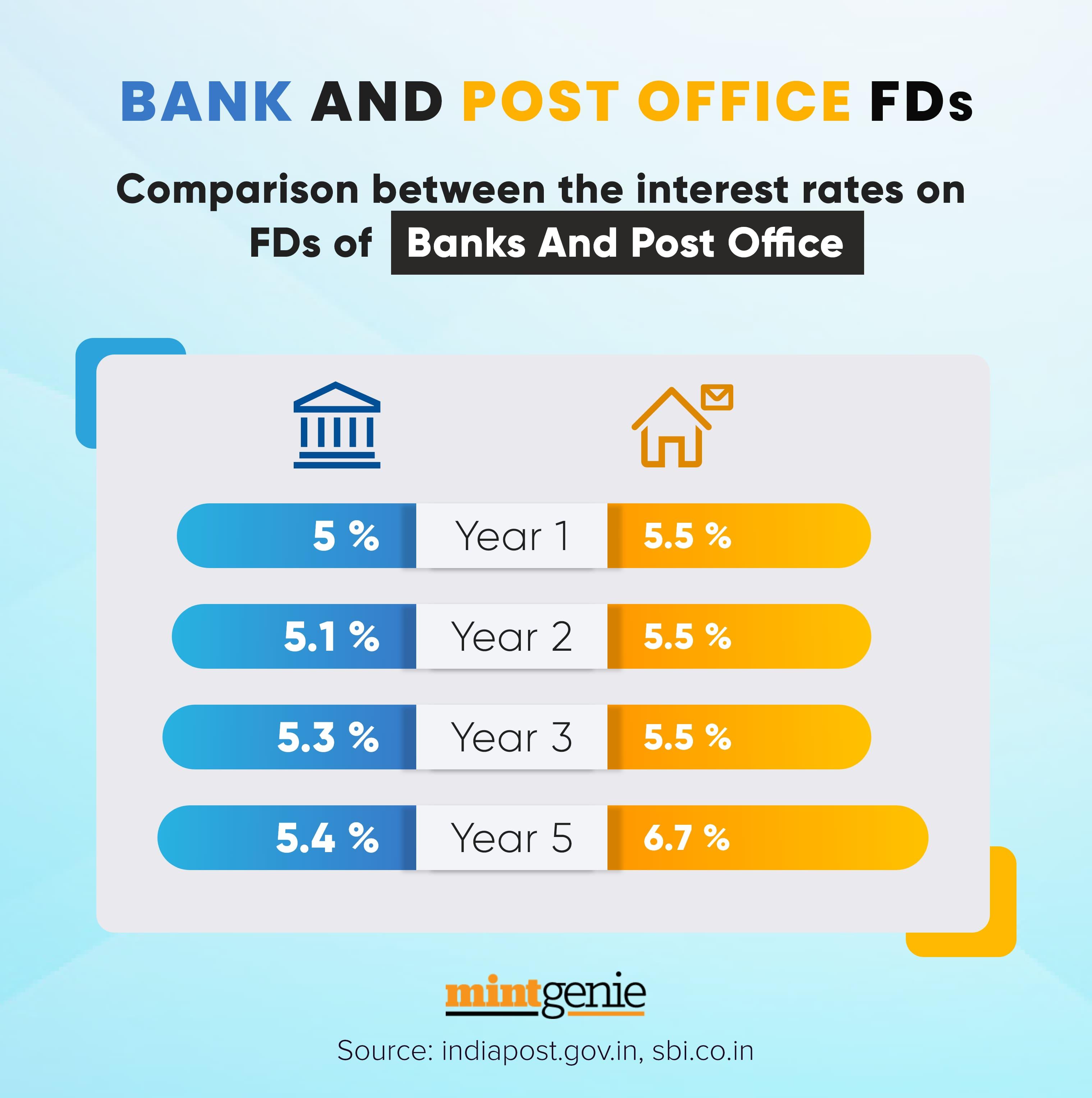

We explain here interest rates on FDs of banks and post offices.

First Published: 12 Jul 2022, 11:05 AM IST

Topics to follow

Related Stories

personal finance

MCLR: What is it and why is preferred over the base interest rate for loan EMIs?

Kirti Jhapersonal finance

RBI imposes restrictions, withdrawal caps on 4 co-op banks; Find details here

Team MintGenie

Explain Like I am 5

personal finance

Fixed Deposit rates: How do they stack up against interest offered by banks & NBFCs

Vimal Chander Joshi