On May 5, Tata Group's consumer durable major Voltas Ltd. announced its March quarter results. In the fourth quarter ended March 2022, the company reported a 23.46 per cent decrease in consolidated net profit, at ₹182.71 crore. The company posted a consolidated net profit of ₹238.72 crore in the January-March quarter of last fiscal.

Results Review: Voltas loses market share but brokerages remain bullish on its future

TL;DR.

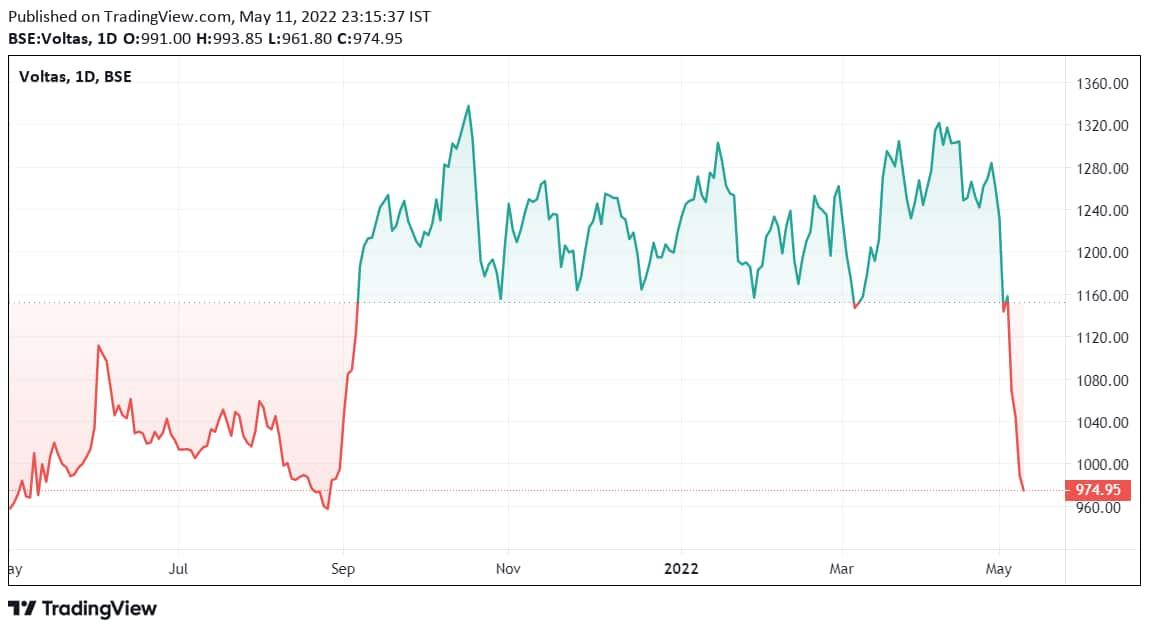

Voltas reported a market share of 23.4% YTD, down from 25.8% YTD Nov 2021, largely due to the low price gap and aggressive pricing. Voltas's shares crashed 15 per cent in a week after the announcement of its Q4 numbers.

Total income was ₹2,703.78 crore during the period under review, up 0.76 per cent from ₹2,683.24 crore in the previous fiscal period.

The company's total expenses were at ₹2,427.53 crore, up 3.73 per cent in the fourth quarter of FY22, as against ₹2,340.22 crore in the year-ago period.

Voltas' revenue from "unitary cooling products for comfort and commercial use" rose 9.89 per cent to ₹1,818.41 crore as against ₹1,654.69 crore in the same quarter of FY21.

Revenue from "engineering products and services" went up 26.43 per cent to ₹123.50 crore as against ₹97.68 crore.

For the fiscal ended March 2022, Voltas' consolidated net profit was down 4.30 per cent to ₹506 crore. It reported a net profit of ₹528.79 crore for FY21.

Voltas reported a market share of 23.4% YTD, down from 25.8% YTD Nov 2021, largely due to the low price gap and aggressive pricing, particularly in southern markets.

However, management believes that market share will recover in the remainder of the summer season with pricing action and customer-centric schemes.

Financials

| Financials (Consolidated) ( ₹Cr) | Mar-2022 | Dec-2021 | Sep-2021 | Jun-2021 | Mar-2021 |

| Total Revenue | 2,703.8 | 1,822.3 | 1,737.3 | 1,860.2 | 2,683.2 |

| Operating Expenses | 2,405.6 | 1,638 | 1,560 | 1,649.4 | 2,320.9 |

| Operating Profit Margin % | 9.79% | 8.68% | 7.64% | 7.61% | 12.47% |

| Interest | 12.5 | 3.6 | 6.2 | 3.5 | 10.4 |

| Profit Before Tax | 276.2 | 171.11 | 161.7 | 198.6 | 343 |

| Tax | 64.7 | 42.5 | 38.5 | 45.6 | 82.1 |

| Net Profit | 182.7 | 96 | 103.6 | 121.8 | 237.7 |

| Basic EPS (Rs) | 5.5 | 2.9 | 3.1 | 3.7 | 7.2 |

Stock performance

Voltas crashed 15 per cent in a week after it announced its March quarter numbers.

Voltas' share gained 8.5% in one year but lost 12.41 per cent since the beginning of this year.

Stock Movement of Voltas

The stock is currently trading near to its 52- week low of ₹953.

Brokerage Views

ICICI Securities believes that the lower than expected performance of Voltas in Q4FY22 is attributable to lower revenues from the EMPS segment and higher raw material costs. On the UCP front, it believes that the revenue growth was primarily driven by price increases (a 15% YTD price increase), while volume offtake was impacted by a higher base and an extended winter.

Voltas continues to be the market leader in the room AC segment with a YTD (till January 22) market share of 25.4 per cent.

ICICI Securities noted that Voltbek’s market share in the highly competitive segments of washing machines and refrigerators grew to 4% and 3.5% YoY, and thus it believes an affordable range of products, strong brand and distribution synergies will help the company to gain further market share.

It assigned a 'HOLD' rating to the stock with a DCF-based target price of Rs1,033/share, valuing Voltas at (implied P/E of 44x of FY24E).

"We remain positive on Voltas volume off-take in FY23. We believe the profitability will continue to remain under stress with higher input prices, freight costs as well as INR depreciation," said ICICI securities.

Meanwhile, Prabhudas Lilladher has cut FY23-FY24 earnings for Voltas by 9-10% on account of a reduction in margin estimates, due to continued commodity inflation and increased competitive intensity.

It noted that Voltas' share price declined 17% over concerns of losing market share in the room AC segment after a long time.

However, Prabhudas Lilladhar is bullish on the stock for the long term due to the comfortable balance sheet of Voltas ( ₹6.45bn net cash and restructuring in the B2B business with a focus on B2C).

It estimated 35% EPS CAGR over FY22-24 and assigned a 'HOLD' rating with a SOTP based Target Price of ₹1,071/share. It valued the UCP business at 46x FY24EPS.

On the other hand, HDFC Securities believes that it will not be easy for Voltas to regain its full market share. However, HDFC Securities is confident on the company's execution capabilities (demonstrated in the past several years).

HDFC Securities cut its EPS estimate by 4% for FY23/FY24 and remained bullish on Voltas as being a market leader in the RAC category, and it also cut its UCP multiple to 45x vs. 50x earlier on FY24 EPS.

Further, it valued the stock on SoTP (UCP/EMPS/EPS P/E at 45/9/15x and Volt-Beko P/S of 4x) in FY24.

HDFC Securities keep its 'ADD' rating for the stock and recommended a target price of ₹1,150/share, implying an upside of 18%.

Edelweiss said that Voltas' revenue of ₹2,703 cr came in their line of estimates of ₹2,681 and above the consensus estimate of ₹2,573 cr.

"We are cautiously optimistic as disruptive pricing by competition could also affect VOLT in the north Indian market." In addition, EMPS "de-grew with a lower order book," said Edelweiss in a report.

Edelweiss revised FY23E/FY24E earnings downwards by 1.4%/5.8% and it maintained 'BUY' with a SOTP-based revised target price of ₹1,246/share.

An average of 37 analysts polled by MintGenie have a 'BUY' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

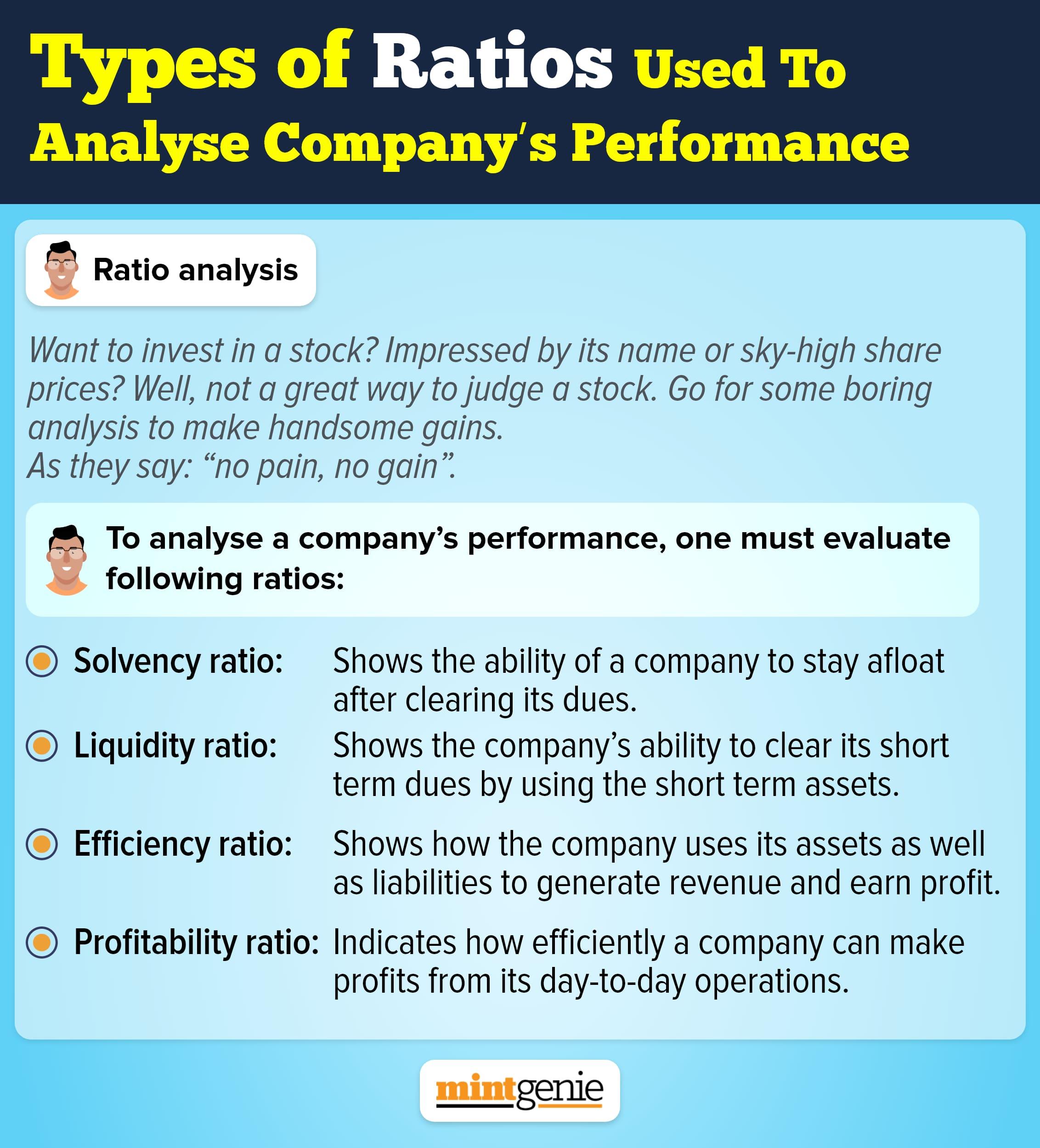

Types of ratios used to analyse company's performance

First Published: 12 May 2022, 10:23 AM IST