After falling 10 percent just in September, the global brokerage house Jefferies sees bluechip stock Reliance Industries (RIL) hitting ₹3,000 in 12 months. The brokerage has a 'buy' call on the stock with a June 2023 target price of ₹3,080, indicating a potential upside of 29.5 percent on the back of its foray into green hydrogen.

Jefferies earlier has a target price of ₹2,980 for the stock.

Reliance Industries has fallen nearly 5 percent in the last 1 year and has been in 2022 YTD. However, in the last 5 years, the scrip has given multibagger returns, up over 150 percent.

"RIL's green hydrogen foray is part of its Net Carbon Zero target by 2035. Falling renewable costs and scale economics will lower green hydrogen costs. Given the capex intensity, RIL's strong balance sheet and backward integration put it in the driver's seat in the $74 billion opportunity," said the brokerage. It further added that RIL's hydrogen business is worth $8 billion at a 20 percent discount to the European benchmark.

Other key positives:

1) Sustainable competitive advantage on scale economics, cost leadership, financial strength, recurring positive free cash flow FY22E onwards

2) ₹2 lakh crore free cash flow invested in consumer businesses created ₹9 lakh crore in equity value

3) New growth engines with large addressable markets: Digital in Jio, and e-commerce in Reliance Retail.

4) Interesting optionalities with likely financial services foray and partnerships with Facebook, Google.

Green energy

Despite its higher cost, govts in major economies are accelerating green H2 adoption to cut carbon emissions. The EU recently identified investments of EUR 63-78bn in the H2 ecosystem and 20 mmtpa consumption target in 2030 backed up by a funding plan.

India also aims to produce 5 mmt green H2 annually by 2030 requiring $130 billion in capex. Policy support including capital subsidies, eliminating charges on renewable power, mandated use in refining and fertilizer, higher fertilizer subsidy funding and development of a carbon trading market should aid adoption.

As per the brokerage, backward integration into end-to-end solar PV manufacturing, wind turbine and grid-scale battery manufacturing helps lower renewable costs. Only a handful of players with adequate balance sheet strength will be able to undertake the high upfront capital commitment and get access to the latest technologies, it noted.

It further highlighted that its calculations suggest an annual capacity of 1 mmt of green hydrogen in India requires $25 bn of capex. These include solar and battery equipment manufacturing facilities, utility-scale solar and wind generation and electrolyzer capex and do not include any capex related to transport and storage of hydrogen. Given the sizeable capex involved, Jefferies sees RIL’s adequately funded balance sheet as a key competitive advantage.

"We value the captive green hydrogen revenue stream assuming it is in an InvIT. We apply 8% cap rate on the operating profit. We then add it to the value of the electrolyzer manufacturing business. We discount the FY30E fair value so obtained at 12 percent WACC to give us a Jun-23E fair value of $8 billion. As RIL establishes its hydrogen business, we see it contributing ₹100/share to our Jun-23 price target," explained Jefferies.

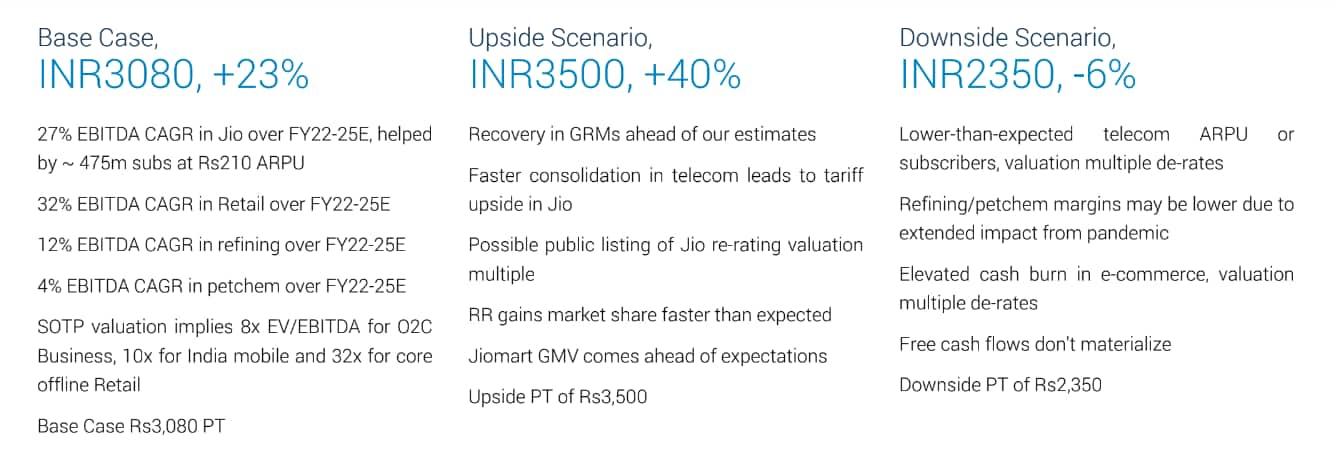

Base, Bull, Bear cases

In the base case scenario, with TP of ₹3080, the brokerage assumes a 27 percent EBITDA CAGR in Jio over FY22-25E, helped by 475 million subscribers at ₹210 ARPU. It also expects a 32 percent, 12 percent, and 4 percent EBITDA CAGR over FY22-25E in retail, refining and petchem, respectively.

In the Bull case scenario, the brokerage has a target price of ₹3,500, indicating an upside of 40 percent. In this particular case, it assumes 1) a recovery in gross refining margins more than estimated, 2) faster consolidation in telecom leads to tariff upside in Jio, 3) possible public listing of Jio re-rating valuation multiple, 4) Reliance Retail gains market share faster than expected, 5) Jiomart GMV comes ahead of expectations.

Meanwhile, in the bear case scenario, the brokerage has a target price of ₹2,350, indicating a downside of 6 percent. For this scenario, the brokerage assumes 1) Lower-than-expected telecom ARPU or subscribers, 2) valuation multiple de-rates, 3) Refining/petchem margins may be lower due to extended impact from the pandemic, 4) Elevated cash burn in e-commerce, 5) Valuation multiple de-rates Free cash flows don't materialize.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.