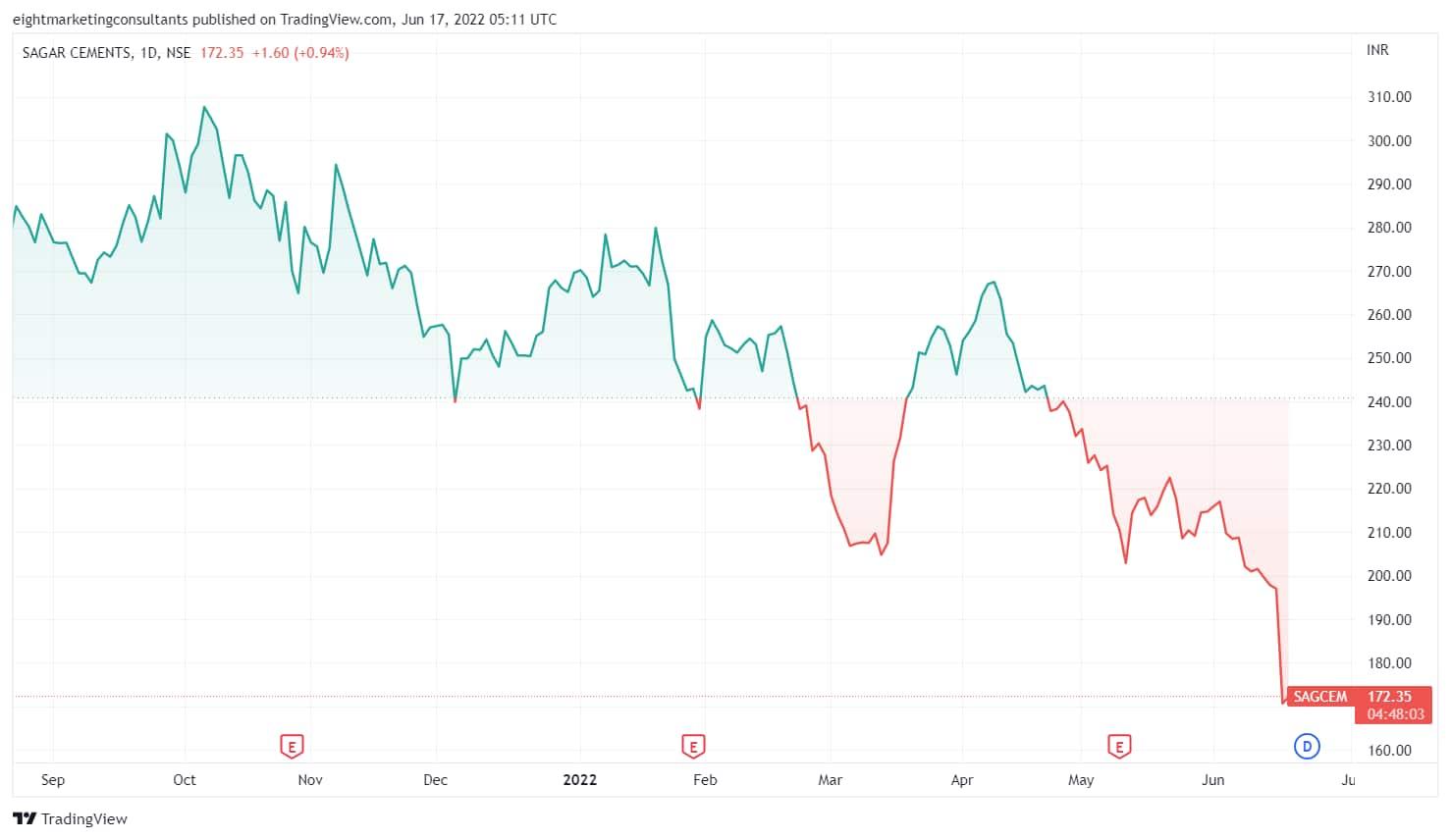

Shares of Sagar Cements ended at Rs. 170.75 on the BSE in Thursday's trade, down 13.37 per cent. The stock has fallen 45.90% from its 52-week high. In the last six months, the stock gave a negative return of 32.22%. It is down 36.66 per cent year to date.

Furthermore, in the last five trading sessions, the stock fell 14.73%.

The stock hit a fresh 52-week low at Rs. 170.75 in Thursday's trade. It has a market value of Rs. 2,231.8 crore.

Stock generated a 31.43% return as compared to Nifty Infrastructure which gave investors a 40.97% return over 3 year time period.

The stock traded at a price-to-earnings (P/E) multiple of 30.25, while the price-to-book value ratio stood at 1.81. The return on equity (ROE) was at 8.01 per cent.

The rising input costs of fuel, petcoke, and coal prices have dampened the gross margins of cement companies in the March quarter. Petcoke prices skyrocketed due to geopolitical tensions between Russia and Ukraine.

Petcoke is widely used by the cement industry. The surge in petcoke prices has led to huge uncertainty in terms of costs and margin recovery for cement companies.

According to media reports, the prices of global pet coke rose by over 50% in March, compared with the average prices recorded during December–February, and those of the domestic variety rose by about 22% in March (from December–February).

Furthermore, higher oil prices have resulted in higher fuel prices, resulting in increased freight expenses.

Sagar Cements reported a consolidated net loss of ₹19.15 crore in the March quarter after 3 consecutive quarters of profits.

The company posted a consolidated net profit of ₹48.15 crore in the January-March quarter a year ago.

For the previous financial year as a whole, the company reported a 68.21 per cent decline in profit after tax to ₹59.15 crore. Sagar Cements posted a net profit of ₹186.12 crore in 2020–21 (Apr-Mar).

However, domestic brokerage firms ICICI Securities and HDFC Securities are bullish on the stock.

ICICI Securities has given a 'BUY' rating for Sagar cements with a target price of ₹265. This equates to a potential 55% upside from the current level. It valued the stock at ₹265 (8.0x FY24E EV/EBITDA multiple).

ICICI believes company Capex's expansions into high-growth regions like east and central will lead to strong momentum going forward.

HDFC securities on the other hand upgrade the stock to buy (from ADD earlier), with a revised target price of ₹240/share, implying an upside of 40% from the current CMP.

"We like the company for its prudent capacity growth, rising regional diversification, and increased focus on green fuel/power consumption and blended cement production," said HDFC securities.

Sagar Cements is a south-based cement player with a cement capacity of 8.25 MT. Region-wise, AP/Telangana accounted for 60% of sales followed by Tamil Nadu (16%), and Karnataka (9%).

An average of 9 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.