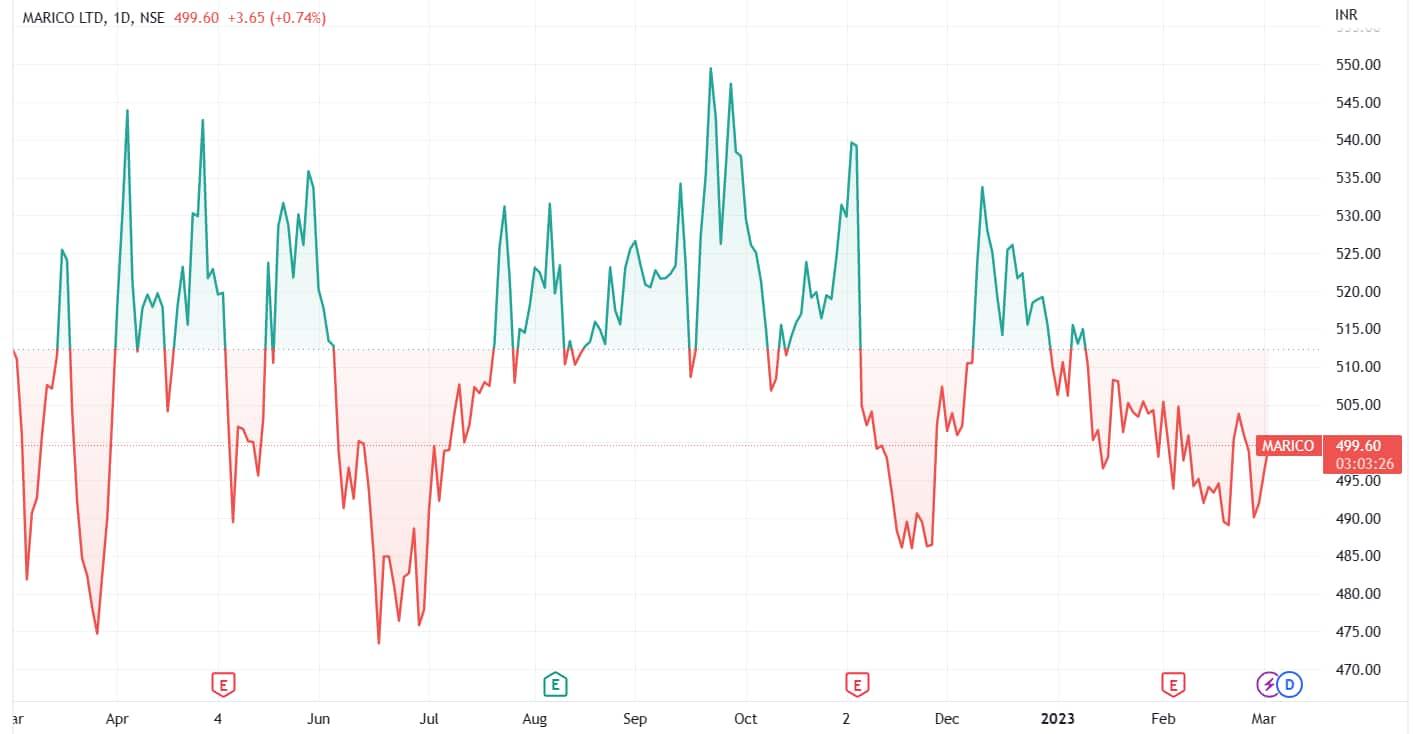

Domestic brokerage firm Sharekhan in its latest research note maintained its bullish outlook on FMCG firm Marico. Although the stock has been underperforming the broader indices for the past year, the brokerage noted that it has better earnings visibility when compared to its peers in a soft-demand environment.

The brokerage firm considers the stock to be an attractive pick in the consumer goods space, given its valuation of 38x/34x its FY2024E/FY2025E EPS, which is at a discount to its five-year average multiple of 42x.

The company is comfortably placed compared to its peers to achieve good double-digit earnings growth in the coming years with key drivers in place. This along with discounted valuations, makes it a good fit from a medium- to long-term perspective, said the brokerage.

Marico is one of India’s leading consumer products companies in the domestic hair and wellness market. The company is present in the categories of hair care, skin care, edible oils, health foods, and male grooming, with a vast portfolio of brands such as Parachute, Saffola, Hair & Care, Nihar, Livon, Kaya Youth, and Coco Soul.

The brokerage pointed out that the market share gains in the core domestic portfolio, scaling up of the foods business, and improving growth prospects in international markets such as Bangladesh and Vietnam are some of the key catalysts for double-digit earnings growth over the next two to three years.

Key input prices such as copra and kardi are down on a YoY basis and are expected to remain range-bound in the coming months. This will lead to a good recovery in its Q4 performance with improved volume growth and sequential margin improvement.

With a price correction of 8% stabilizing in key markets, Parachute rigid pack volume growth is expected to improve to the mid-single digit in Q4 FY2023. The shift to branded coconut oil has regained its pace and will support a recovery in Parachute coconut oil volume growth in the coming quarters, it added.

Saffola Brand, on the other hand, crossed Rs. 2,000 crore in revenue and is expected to maintain its strong growth momentum in the coming years. In addition, Livon Serums continued its double-digit growth momentum, while Set Wet's portfolio is nearing pre-Covid levels, said the brokerage.

Marico is well poised to achieve a 15% earnings CAGR over FY2022-FY2025E, aided by steady growth in the core portfolio coupled with scale-up in emerging businesses such as foods and digital brands.

The brokerage maintained its "buy" rating on the stock with an unchanged target price of ₹645 apiece, implying an upside potential of 30.30% from the stock's previous closing price.

In the October-December quarter, Marico delivered a decent performance with low-mid single-digit revenue and PAT growth despite multiple headwinds. The company reported a 5.04% rise in consolidated net profit at ₹333 crore, compared to ₹317 crore in the October-December quarter a year ago.

The total revenue from operations during the quarter came in at ₹2,470 crore, up 2.61% as against ₹2,407 crore in Q3FY22. Its revenue from the domestic market was up 1.87% to ₹1,851 crore in Q3 FY23. The revenue from international business stood at ₹619 crore, up 4.91% in the third quarter of FY23.

39 analysts polled by MintGenie on average have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.