After a 32 percent jump in October and November (combined), brokerage house HDFC Securities has initiated coverage on hospital stock Indraprastha Medical Corporation (IMCL) with a buy call for a time horizon of 2-3 quarters.

"We believe the base case fair value of the stock is ₹75.75 (7.7x FY24E EPS) and the bull case fair value of the stock is ₹83.25 (8.5x FY24E EPS) over the next 2-3 quarters. Investors can buy the stock at between ₹66.5-68.5 and add on dips to ₹59 band (6x FY24E EPS). At the LTP, the stock is trading at 6.9x FY24E EPS," recommended the brokerage.

HDFC Securities noted that due to pandemic-induced lockdowns, healthcare companies in India were severely impacted. There was a significant drop in patient footfall—be it a single specialty, multi-specialty, tertiary-care hospitals, or even diagnostics businesses, during this time, it added.

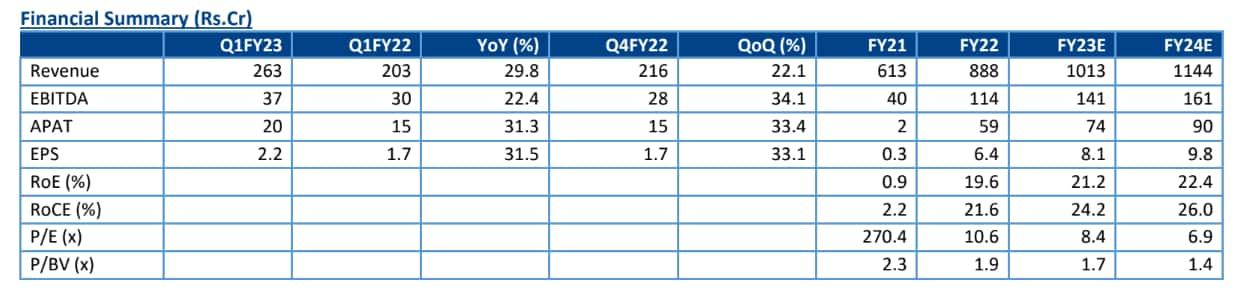

"The financial performance of IMCL was also impacted due to the same, however, as the situation has stabilized, the company’s business has also got back on track. There was a 45 percent jump in revenue and margins again also improved to 13 percent in FY22 vs 6.6 percent in FY21. The company has negligible debt on the balance sheet and has been paying healthy dividends to its shareholders," rationale the brokerage. It expects a 13 percent CAGR in revenue and a 24 percent CAGR in Net Profit over FY22-24E.

Indraprastha Medical Corporation, a JV between Apollo Hospitals Enterprise (holds 22 percent stake) and the State Government of Delhi (Government holds 26 percent stake) is a 764-bedded, super specialty tertiary care hospital with 52 specialty departments.

The stock rose 19 percent in November so far after an 11.5 percent jump in October even as broader markets were extremely volatile. In the 10 completed months of 2022, the stock gave positive returns in 6 of them. It surged the most in August and November (so far), up 19 percent in each, meanwhile, it lost the most in February, down 15 percent.

The brokerage also pointed out that the company has an impeccable track record, a long presence as well as a quality of medical care supported by long-term relationships with its doctors and other medical professionals. It also drives significant tangible and intangible benefits from the "Apollo" brand value.

HDFC is constructive on the Indian healthcare market and believes that there is immense potential for growth as driven by the rising income levels, aging population, increasing healthcare awareness, increasing health insurance penetration and renewed focus of the government on building universal healthcare, especially after the pandemic.

"IMCL is a good bet on the structural long-term growth story of the Indian healthcare industry, considering its established presence, its strong brand image, healthy financials, asset-light business model and lower capex need. The company is available at decent valuations compared to other peers," it said.

Geographic concentration, government regulations and ongoing litigations regarding free treatment to poor patients are the key concerns for the long-term investment in the company, further added HDFC.

In the June quarter, the company reported strong performance with 30 percent YoY and 22 percent QoQ sales growth to ₹263 crore. EBITDA margin stood at 12 percent in Q1FY23 vs 10.1 percent in Q1FY22; it, however, slipped on a QoQ basis by 190bps. Meanwhile, the net profit of the firm rose by 31 percent YoY and 33 percent QoQ to ₹20.3 crore for the quarter.

"IMCL’s financial profile has been robust led by negligible debt, healthy cash generating ability and consistent dividend payment to shareholders over the past. Financial flexibility is strong, supported by robust liquidity. There was a minor blip in the performance due to Covid due to price caps for Covid treatment and lower footfall of non-Covid patients amid lockdowns. However, with the ease in a pandemic situation, the improvement in the financials was clearly visible," noted the brokerage.

In FY22, the company reported revenue of ₹888 crore, up 45 percent YoY, with 13 percent operating margins. The momentum was sustained in Q1FY23 also.

With no major need for capex as well as a lower requirement of working capital, the debt level remains at a negligible level, which along with better-operating margins resulted in healthy profitability, HDFC pointed out.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.