In a stock market filing to the BSE, HDFC Ltd announced on Monday that its board has approved a transformation merger with HDFC Bank. The scheme, however, is subject to approvals from numerous regulators such as RBI, SEBI, among others.

As per the merger deal, for every 25 shares held in HDFC Ltd, a shareholder will get 42 shares of HDFC Bank. Shares of HDFC Ltd and HDFC Bank rallied up to 11 percent after both the firms announced a corporate merger.

The combined entity will bring together complementary strengths of the two organisations, enabling a rewarding customer relationship. Post the combination, HDFC Bank’s customers will be offered mortgages as a core product in a seamless manner, it said in a statement.

Six key reasons for the merger:

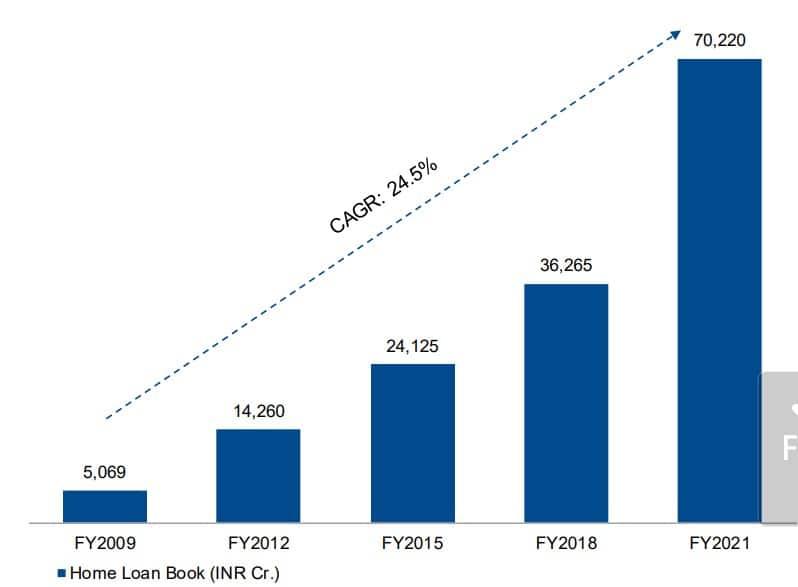

1. Demand for housing sector: First and foremost, there are structural drivers in place for housing sector. The demand for housing is poised to drive Indian economy. There is a growing importance of mortgages for the bank. In fiscal 2009, the home loan book was valued at ₹5,069 crore, which rose to ₹14,260 crore in fiscal 2012.

This further rose to ₹24,125 crore in fiscal 2015, to ₹36,265 crore in fiscal 2018 and finally to ₹70,220 crore in fiscal 2021.These figures show a CAGR of 24.5 percent.

The below chart indicates growing importance of mortgages for the bank

2 Robust asset portfolio mix: After the merger, secured and long tenor product will ensue robust asset portfolio mix. HDFC Bank has total advances of ₹12,68,863 crore, whereas HDFC has ₹525,806 crore. The banking company has 35 percent allocation to commercial and rural banking; 28 percent to retail customers, 11 percent to mortgages and 26 percent to corporate.

HDFC, on the other hand, will have 77 percent allocation to individuals, 9 percent to lease rental discounting and 5 percent to corporate.

The merged entity is likely to have total advances of ₹17,86,669 crore out of which the largest share will be seized by mortgage i.e., 33 percent, 24 percent by commercial and rural banking, 21 percent by retail customers and 19 percent by corporate.

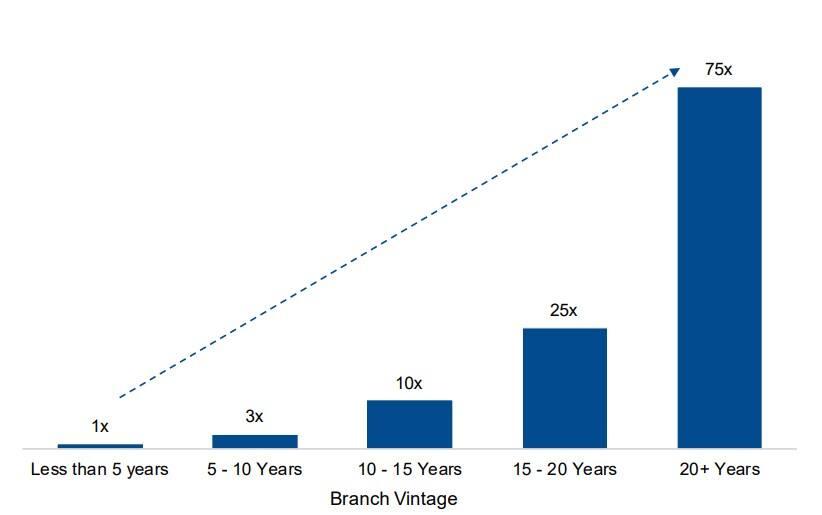

Branch deposits continue to compound

3. Leveraging the power or branch banking: The merged entity will be able to leverage the power of branch banking. The branch deposits compound with time.

In 5 to10 years, the branch deposits will increase 3 times, whereas increase by 10X in 10-15 years. In another 15-20 years, the branch deposits increase 25 times whereas in 20 plus years, they increase 75 times.

4. Ability to cross sell with full suite of financial products: Savings accounts of HDFC Bank and mortgages of HDFC will offer a bouquet of services to customers across the categories of life insurance, general insurance, health insurance, investment products, credit cards and personal loans.

HDFC argues that it will increase the organisation's ability to enhance customer lifetime value.

ALSO READ: HDFC Ltd and HDFC Bank to merge: Here's all you need to know

5. Blend of deep multi decade mortgage underwriting expertise: There will be a blend of deep multi decade mortgage underwriting expertise across cycles. On one hand, HDFC Bank has superior scale and distribution, core financial products, superior risk management framework, strong data analytics and digital competencies, on the other hand, HDFC is number on mortgage player, has 45 years of deep domain expertise, best in-class cost of operations and around 3,500 product specialists.

The merged organisation is expected to enable faster origination, improved operational efficiency, and reduced default rates.

6. Better integration of resources: Finally, there will be seamless integration of people, processes, infrastructure with limited disruption.

The well-entrenched and aligned processes would reduce lead time typically needed to unlock synergies, and there will be minimal need towards optimization of any physical infrastructure assets.