Westlife Development Ltd (WLDL), through its 100% subsidiary, Hardcastle Restaurants Pvt Ltd (HRPL) owns and operates McDonald’s restaurants in West and South India.

Stock analysis: Axis Securities says 'buy' Westlife Development Ltd

TL;DR.

Axis Securities initiates coverage on the stock with a ‘BUY’ recommendation and a Target Price (TP) of ₹625/share, implying an upside of 30% from the current CMP.

McDonald’s operates in various formats that include standalone restaurants, delivery, drive-thru’s and On the Go. It also has four brand extensions – McCafe, McBreakfast, McDelivery, and Dessert Kiosks. As per the 2010 agreement, HRPL is the master franchisee of McDonald’s Corporation, USA.

Moreover, HRPL is responsible for all financing and development of McDonald’s stores in West and South India, while operations and technical support will be provided by McDonald’s Corporation.

Industry overview

Within the organised foodservice market, QSR (Quick Service Restaurant) segment is expected to grow at a 23% CAGR over FY20-25, outpacing all other chain food segments. It has recovered swiftly from the pandemic and has become much stronger.

Due to the pandemic, QSR players are making swift changes in product offerings, focusing on delivery, regionalising the menu, entering smaller cities/towns, and, as per Axis Securities research report, there is a pent-up demand for movies and eating out, which will benefit the overall QSR segment as 30–40% of stores are located in malls. Domino’s, McDonald's, Burger King, Pizza Hut, and KFC are key players in the Indian QSR segment.

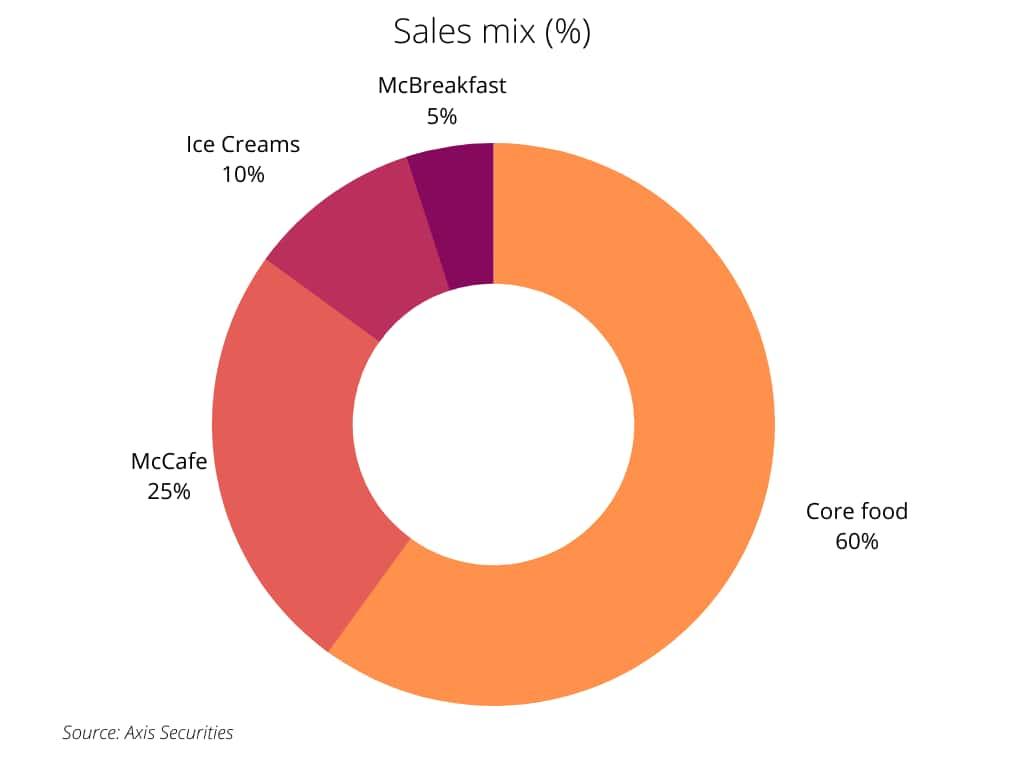

Product Portfolio

WLDL has entered into different categories and has introduced various formats to increase consumption through ‘All Day Menu’ – McCafé (in between day), McBreakfast (breakfast), McDelivery, Dessert Kiosk, and recently entered into gourmet burgers and fried chicken category to cater different sets of the customers.

Sales mix of WLDL

Such a diversified menu provides sustained revenue and growth through all its stores without incurring any heavy Capex, thereby improving the returns profile at the aggregate level, the report added.

Opportunity

The company is well placed to capitalise on the growing QSR opportunity on account of - Its ability to drive consistent growth in SSSG (Same-store sales Growth) and keep the innovation funnel on - Launching new products that suit the Indian taste palate, Entering and then quickly scaling up the growing QSR categories – (Fried chicken and coffee), Pushing affordability through combo meals, and driving premiumisation through launching premium products to increase overall ticket size (from current ₹200-250).

Moreover, the company continues its sharp focus on driving convenience format –delivery, drive thru’s and On the Go, format to mitigate the future risk of dine-in while simultaneously providing customers with more touchpoints that will improve the overall consumer experience says Axis Securities in a research report.

Financials

The company reported a multi-fold jump in its consolidated net profit to ₹20.82 crore for the third quarter ended December 2021. The company had posted a net profit of ₹0.11 crore in the corresponding quarter last year.

Its sales during October-December 2021 jumped 46.68 per cent to ₹476.83 crore, compared with ₹325.06 crore in the year-ago period.

It also reported a high EBITDA (earnings before interest, tax, depreciation and amortisation) of ₹83.62 crore.

| Key Financials (Consolidated) ( ₹Cr) | FY21 | FY22E | FY23E | FY24E |

| Net sales | 986 | 1,573 | 1,920 | 2,361 |

| EBITDA | 47 | 189 | 253 | 333 |

| Net Profit | -104 | -10 | 21 | 57 |

| EPS (Rs) | -6.7 | -0.6 | 1.4 | 3.7 |

| PER (x) | NA | NA | 355.8 | 130.9 |

| EV/EBITDA | 160.1 | 39.2 | 29.0 | 21.7 |

| P/BV (x) | 15.6 | 15.9 | 15.3 | 13.7 |

| ROE (%) | -21.5 | -2.1 | 4.3 | 10.4 |

| Source: Axis Research |

Operating costs and expenses stood at ₹369.24 crore, a jump of 43.13 per cent as against ₹257.96 crore a year ago. The company added eight new stores, taking the total store count to 316 restaurants across 44 cities.

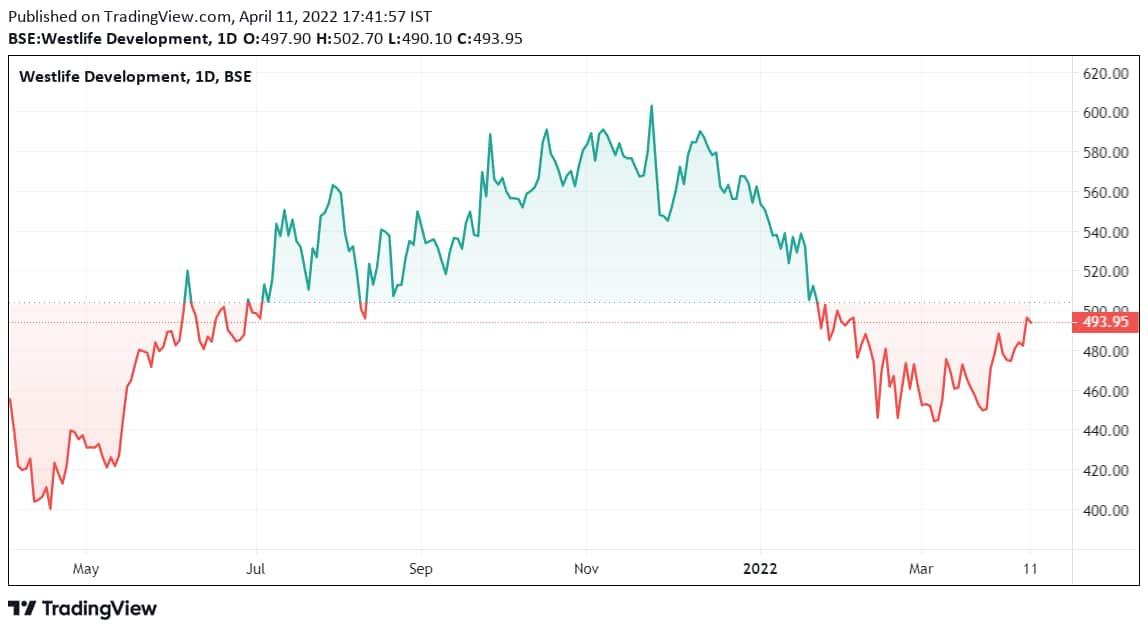

Stock Performance

In the past one year, the stock of Westlife development has surged 15 per cent as compared to a 22 per cent rise in the S&P BSE Sensex, Moreover, in the past 3 years, it has rallied 18 percent.

Stock Movement of Westlife Development Ltd.

Further, over the past five years, the market price of the stock has zoomed 100 per cent, as compared to a 105 per cent surge in the Sensex.

Future Plans

WLDL has 316 (3QFY22) stores currently and plans to open over 200 stores in the next 3–4 years, implying an addition of 40–50 stores annually. Its 70–80% store presence is concentrated in metros and tier 1 cities, implying significant room for further expansion into smaller cities/towns. While currently, it is present only in 43 cities, the brokerage believes the market opportunity is spread across 160 cities across west and south India.

Moreover, the company's management's ambition to convert all normal stores into digital-savvy EOTF stores (33% of total stores) and the introduction of McCafe (80% of total stores) will further drive the company’s medium-term growth prospects, it added.

Outlook

Axis Securities initiates coverage on the stock with a ‘BUY’ recommendation and a Target Price (TP) of ₹625/share, implying an upside of 30% from the current CMP.

Going forward it expects the company to deliver healthy Revenue/EBITDA growth of 11%/11%CAGR over FY20-24E. The stock is currently trading at 22x EV/EBITDA on FY24E earnings (3year average EV/EBITDA is 45x), which we believe is attractive given the company’s strong revenue growth over FY20-24E and large headroom for expansion moving forward, Says Axis securities in a report.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

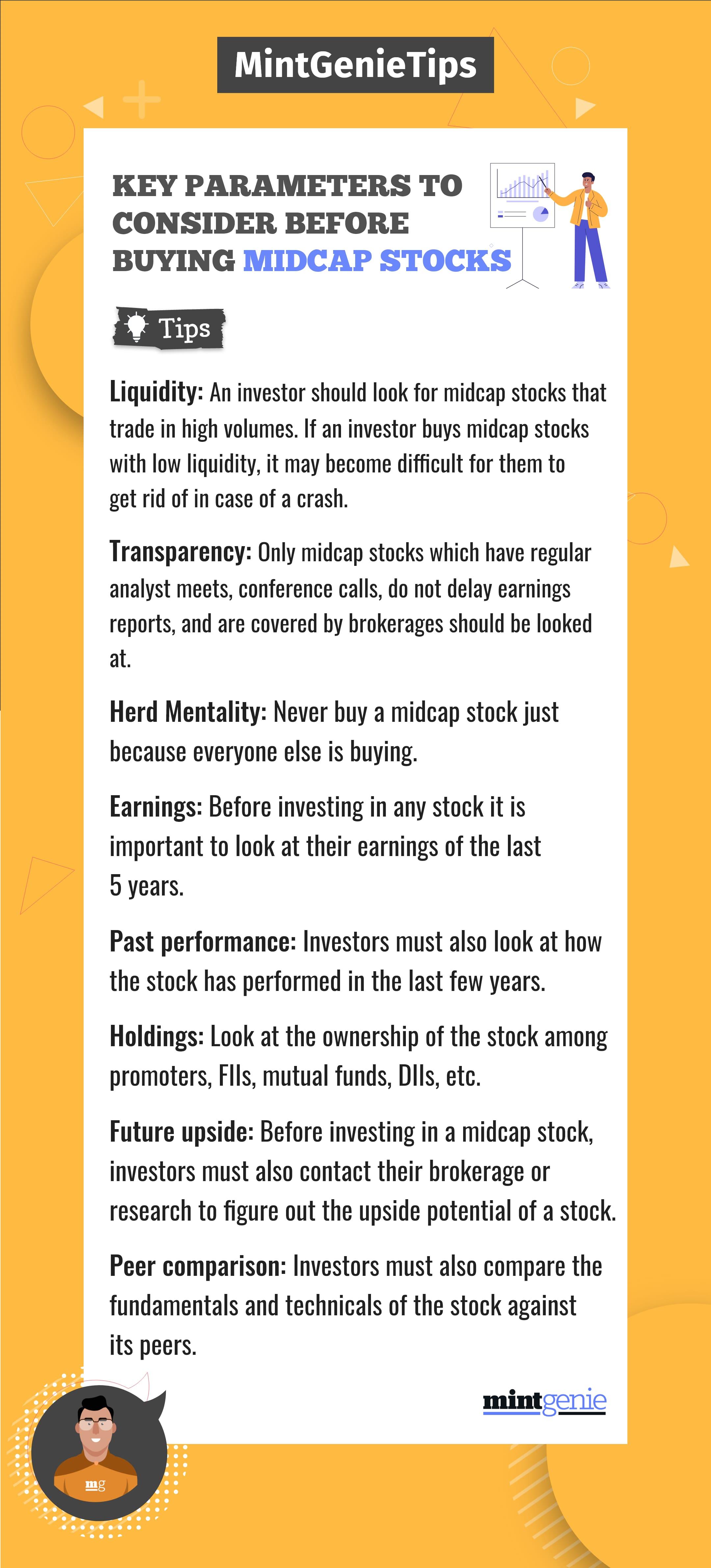

Key parameters to consider before buying midcap stocks

First Published: 12 Apr 2022, 08:07 AM IST