Emami has expanded its summer portfolio by acquiring Reckitt's Dermicool, well-known prickly heat and cool talc brand, for ₹432 crore.

Stock Analysis: Emami's Dermicool acquisition will strengthen its summer portfolio

TL;DR.

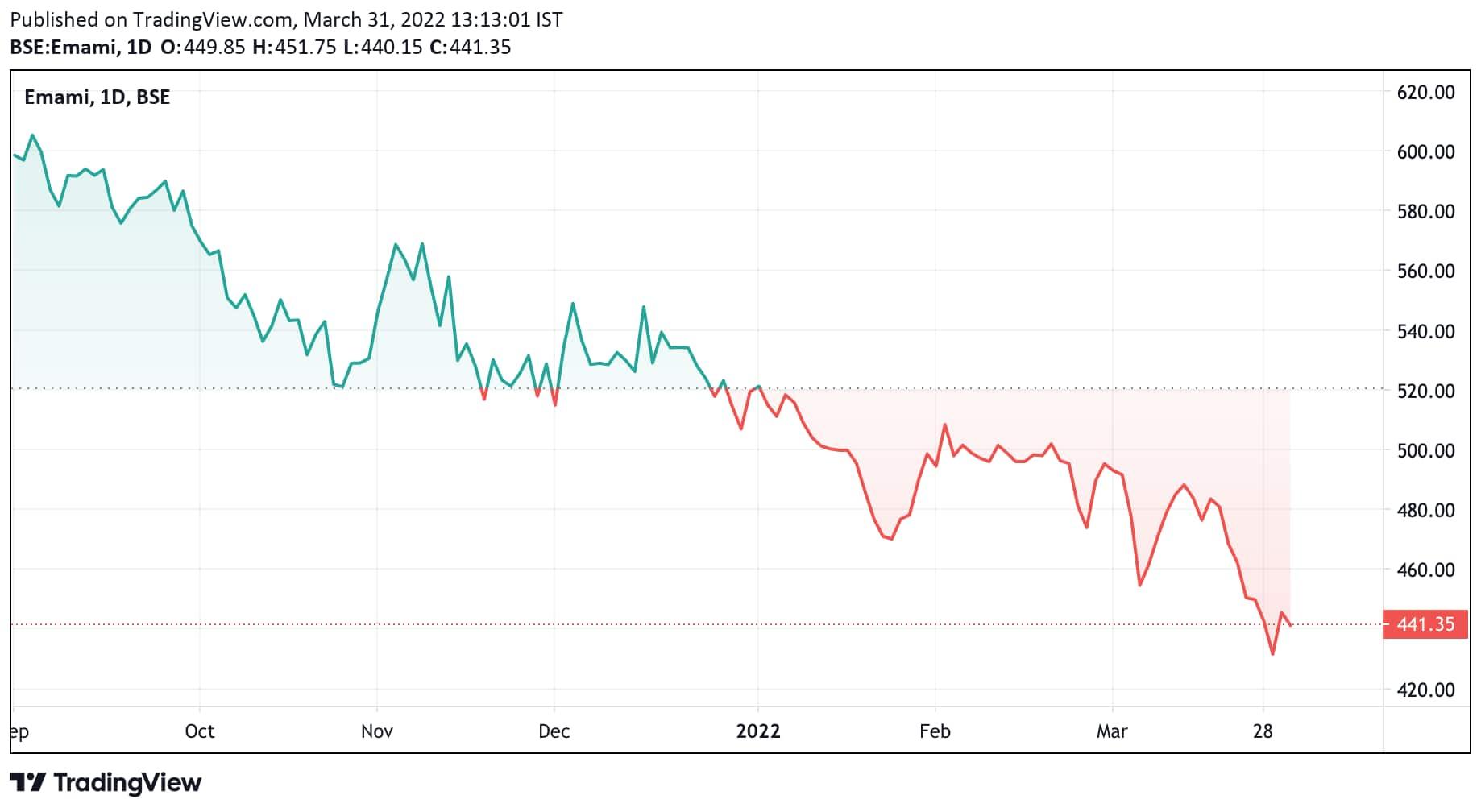

Sharekhan has given a 'buy' recommendation on the stock with a revised price target of Rs.550, Around 24% higher than the current market price of 441 (valuing it at 26x its FY2024E EPS).

Dermicool has a 20% market share and, together with Navratna cool talc, will control 45 percent of the low penetrated prickly heat and cool talc category, which is worth ₹760 crore.

“Emami's acquisition of Dermicool was in line with its objective of strengthening its portfolio with strong brands that have the potential to grow steadily in the medium to long term. In the long run, the brand delivers a lot of synergistic benefits and margin improvement potential,” according to a report by Sharekhan.

| Valuation (Consolidated) | ₹Cr | |||

| Particulars | FY21 | FY22E | FY23E | FY24E |

| OPM (%) | 30.7 | 31.0 | 30.1 | 31.0 |

| Adjusted PAT | 673 | 735 | 776 | 946 |

| % YOY Growth | 28.0 | 9.2 | 5.6 | 21.8 |

| Adjusted EPS (Rs.) | 15.1 | 16.5 | 17.5 | 21.3 |

| P/E (x) | 28.7 | 26.1 | 24.7 | 20.3 |

| P/B (x) | 10.9 | 9.7 | 8.6 | 7.2 |

| EV/EBITDA (x) | 21.2 | 18.9 | 17.8 | 14.5 |

| RoNW (%) | 37.5 | 39.3 | 36.9 | 38.8 |

| RoCE (%) | 42.5 | 47.9 | 46.6 | 48.7 |

| Source: Sharekhan Estimates |

Analysts at Sharekhan believe that the acquisition of the Dermicool brand will strengthen Emami's summer product portfolio because the acquisition was funded through internal accruals and Emami has a cash surplus of over ₹500 crore.

Why Dermicool?

Dermicool has a turnover of more than ₹100 crore, with gross margins of 55 percent and EBITDA margins of 38 percent (compared to Emami's consolidated EBITDA margins of 30 percent).

"Slowdown in rural India and sustained high input cost inflation will affect the company's earnings in the near term," according to sharekhan. We anticipate that revenues will be nearly flat in Q4FY2022, while gross margins will fall by 100 basis points year on year.

The impact of a significant increase in input prices will be felt in H1FY2023. As a result of the slowdown in demand and ongoing margin pressures, we have reduced our earnings estimates for FY2023 and FY2024 by 10% and 7%, respectively.

Stock has corrected by 13% in the last one month (26% in last six months) factoring the near-term uncertainties. The stock is currently trading at discounted valuations of 24.7x/20.3x its FY2023E/24E EPS.

Emami share price chart over the past 6 months.

Sharekhan has given the company a ‘buy’ recommendation with a revised price target of Rs.550, which is around 24% higher than the current market price of 441 rupees (valuing it at 26x its FY2024E EPS).

Can Dermicool help Emami survive the Summer?

It further said that Emami will become the No. 1 player in the prickly heat, and cool talc category after acquiring the Dermicool brand, with a market share of almost 45 percent, surpassing Nycil, which has a market share of 34 percent.

In the ₹760 crore prickly heat and cool talc category, Emami's Navratna Cool Talc (25 percent market share) is currently the No. 2 player, followed by Dermicool at No. 3 (20 percent market share). Aaya Mausam Thande Thande Dermicool Ka, Dermicool's widely known jingle, has a strong consumer connection. As per the report, the acquisition makes a solid argument for Dermicool coexisting alongside Emami's existing brands.

| Comparison in terms of various parameters | ||

| Particulars | Emami (Navranta, Boroplus) | Dermicool |

| Category | Cooling talc | Prickly heat talc |

| Caters to | Mass (45% contribution from below Rs. 10 SKU) | Mid - Premium (150 gm contributes 80% of revenues) |

| Distribution reach | Direct reach of 2 lakh outlets | Direct reach of 1.25 lakh outlets |

| Modern trade penetration | Low penetration | Higher penetration |

| Contribution from Wholesale | 38-40% of revenue | 35% of revenue |

| Rural Penetration | 70% | 65% |

| Gross Margin | 67% | 55% |

| EBITDA Margin | - | 38% |

| Source: Sharekhan Research |

Dermicool has a significant presence in e-Commerce, modern trade channels, and South Indian regions. Rural and other areas are where Emami excels.

Dermicool is a pan-India brand with 1.25 lakh direct outlets and 1.8 million indirect outlets, while the Navratna network has a direct reach of 2 lakh outlets and an indirect reach of 1.8 million outlets.

Emami can take advantage of Dermicool's higher penetration in modern trade (currently, Navratna has a small contribution from modern trade). In the domestic market, Emami has a direct reach of 8.4 lakh shops and an indirect reach of close to 5 million outlets. A third-party manufacturer will produce the brand, which is currently responsible for Navratna Cool Talc for the corporation, it added.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

The FMCG sector is likely to reach ₹16.3 lakh-crore by 2025.

First Published: 31 Mar 2022, 01:14 PM IST