Auto major Tata Motors reported a higher-than-expected consolidated loss at ₹ ₹945 crore for the quarter that ended September (Q2FY23) due to semiconductor woes. However, despite missing analyst expectations, the loss narrowed from ₹ ₹4,442 crore in the year-ago quarter. The Street had estimated the company's net losses to shrink to ₹655-755 crore.

Tata Motors Q2 Earnings miss expectations: Analysts cut earnings estimates; stock falls 5%

TL;DR.

Shares of Tata Motors fell as much as 5.4 percent in intra-day deals to hits the day's low of ₹409 as earnings missed Street expectations. Overall, in the last 1 year, the stock has lost 15 percent as against a 10 percent jump in Nifty Auto and half a percent rise in benchmark Nifty.

Its consolidated revenue from operations rose 29.7 percent on a year-on-year basis to ₹79,611.3 crore for the quarter under review as against ₹61,378.82 crore from the year-ago period. Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA) margin, also improved by 130 basis points (bps) YoY in Q2FY23 to 9.7 percent.

The company, in its investor presentation, said that its revenue, profitability, and cash flows improved despite lower-than-planned volumes due to chip supply.

On a standalone basis, the company reported a net loss of ₹293 crore. It had posted a net loss of ₹659 crore in the year-ago period. Total standalone income rose to ₹15,142 crore in the second quarter, as compared to ₹11,197 crore in the same period last year.

Jaguar Land Rover (JLR), a part of Tata Motors, reported revenues of 5.3 billion pounds in the second quarter, up 36 percent from the year-ago period. Its wholesale volumes (excluding China JV) stood at 75,307 units in the July-September period, up 17.6 percent as compared to the same period last year.

The wholesale increase was lower than planned, primarily due to a lower-than-expected supply of specialised chips from one supplier which could not be readily re-sourced in the quarter, Tata Motors said. JLR is continuing to focus on signing long-term partnership agreements with chip suppliers which are improving the visibility of future chip supply, it added.

For India's business, domestic wholesales stood at 93,651 vehicles, up 19 percent year-on-year. However, exports were at 6,771 vehicles, lower by 22 percent, affected by the financial crisis in a few export markets, it said.

"Going forward, we continue to remain in the agile mode and are keeping a close watch on the evolving geopolitical, inflation and interest rate risks on both supply and demand," Tata Motors Executive Director Girish Wagh said.

The passenger vehicles business continued its strong momentum with wholesales at 1,42,755 vehicles, up 69 percent YoY, amid strong festive demand and debottlenecking actions, the automaker said.

On the overall business outlook, the automaker stated that demand continues to remain strong, however, it will remain a key monitorable in the wake of global uncertainties.

"Improving chip supply and cooling commodity prices will aid revenue and margins recovery and hence aim to deliver strong improvements in EBIT and free cash flows in H2 FY23," it added.

Stock price trend

Shares of the auto major fell as much as 5.4 percent in intra-day deals to hits the day's low of ₹409 as earnings missed Street expectations.

Overall, in the last 1 year, the stock has lost 15 percent as against a 10 percent jump in Nifty Auto and half a percent rise in benchmark Nifty.

On a YTD basis, the stock is down 14 percent versus a 19 percent gain in Nifty Auto and a 4 percent jump in Nifty.

In the 10 completed months of 2022, the stock fell in 4 of them and rose in the remaining 6. It tanked the most in September 2022, down 14 percent followed by in February, down

12 percent. Meanwhile, it lost 7 percent and 4.5 percent in June and March, respectively.

On the other hand, it rise the most in July, up 9 percent followed by in January, up 7 percent.

Tata Motors stock price trend

Here's what brokerages say

Motilal Oswal

The brokerage maintained a 'buy' call on the stock with a target price of ₹500, indicating an upside of 15 percent.

"TTMT’s 2QFY23 performance was an all-round miss. JLR continues to struggle with semiconductor shortages, which has been impacting its performance for the last five-to-six quarters. Its India CV and PV businesses were hit by residual commodity cost inflation, which should reverse from 3QFY23. The ramp-up in JLR’s production is key as demand is strong, especially in its most profitable products of Range Rover (RR), RR Sport, and Defender (72 percent of the order book)," said the brokerage.

It also cut the stock's consolidated EPS estimate for FY23 (to a loss from a profit) and FY24 (by 6 percent) to account for a slower production ramp-up at JLR.

Going ahead, the brokerage believes TTMT should witness a gradual recovery as supply-side issues ease (for JLR) and

commodity headwinds stabilize (for the India business). It will benefit from: a) a macro recovery in India, b) company-specific volume and margin drivers, and c) a sharp improvement in free cash flow and leverage in both JLR as well as the India business, said MOSL.

Emkay

The brokerage retained its buy call on the stock but cut its target price to ₹490 from ₹515 earlier. The new target indicates a potential upside of 13 percent.

Tata Motors’ Q2FY23 consolidated EBITDA grew 53 percent YoY (3-yr CAGR: -5 percent) to ₹6,200 crore, missing our estimates by 9 percent mainly due to cost pressure in India. Consolidated revenue grew 30 percent YoY (3-yr CAGR: 7 percent) to ₹79,600 crore, standing 3 percent% above our estimate because of JLR’s improved mix. JLR’s order book is strong at 2,05,000 units. Models such as new generation RR/RR Sport and Defender form >70 percent of the order book which should lead to product-mix improvement ahead," noted the brokerage.

It further added that JLR production ramp-up is expected to improve at a slower pace in H2FY23 versus earlier expectations, due to supply constraints. Owing to lower volume (JLR) and margin assumptions, Emkay reduce FY23-25E consolidated EBITDA by 5-14 percent.

"We maintain our positive stance on expectations of a sales upcycle across segments, aggressive cost savings and debt reduction," it said. Key risks include further delay in production ramp-up due to supply issues, luxury car demand contraction in target markets, lower-than-expected growth in India CVs/PVs, failure of new launches and adverse currency/commodity prices.

Prabhudas Lilladher

"Tata Motors’ Q2FY23 consolidated revenue surprised largely led by improved product mix at JLR. Though JLR reported merely 5 percent QoQ growth in wholesales, ASPs improved 14 percent on the back of improved supplies of New RR/RR Sport. This also led to 400 bps QoQ of EBITDA Margin (10.3 percent) improvement. We expect margins to further improve in 2H led by improved realizations and product mix. The chip supply issue is now sorted out and management expects volumes >160k units in 2H (147k in 1H); supplies should step up in FY23," said the brokerage.

It maintains a positive stance on Tata Motors as the (1) Likely market share gains in the PV segment led by revamped portfolio, customer preference for SUVs and rising EV penetration, (2) CV volumes gains from the cyclical upturn, improving fleet utilization and freight rates and (3) revival in JLR and strong order book to benefit and drive free cash flow generation.

However, it trimed its EBITDA estimates by 9/3 percent for FY24/25 to factor in moderation in volume growth at JLR and cost pressures. It maintained BUY, with a revised target price of ₹520, indicating a 20 percent upside in the stock.

ICICI Securities

The brokerage believes this commentary is below Street expectations with stock expected to open negative despite fundamental levers for better operational performance in its Indian business. The only solace was the company finally securing long-term semiconductor supplies, which could support volumes in CY23E.

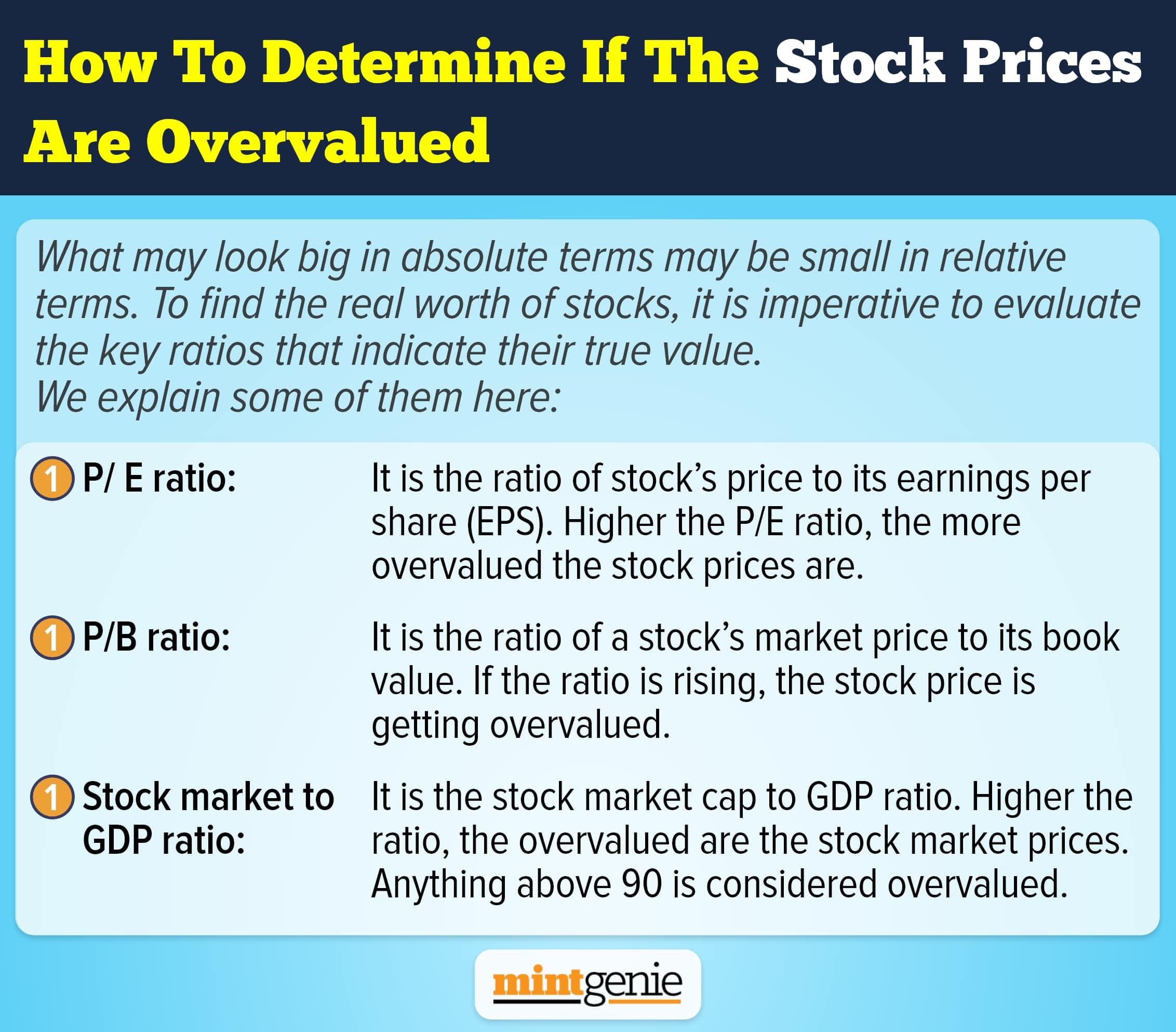

How to determine if the stock prices are overvalued.

First Published: 10 Nov 2022, 12:39 PM IST