Shares of Havells India, an electric equipment company, have the potential to reach Rs.1,621/share from its previous closing price of Rs.1,232 implying a 31.57% potential upside, ICICI Securities said in its equity research report. As of Tuesday, the stock is trading at ₹1,254, up 1.84% on the BSE at 12:15 PM (IST).

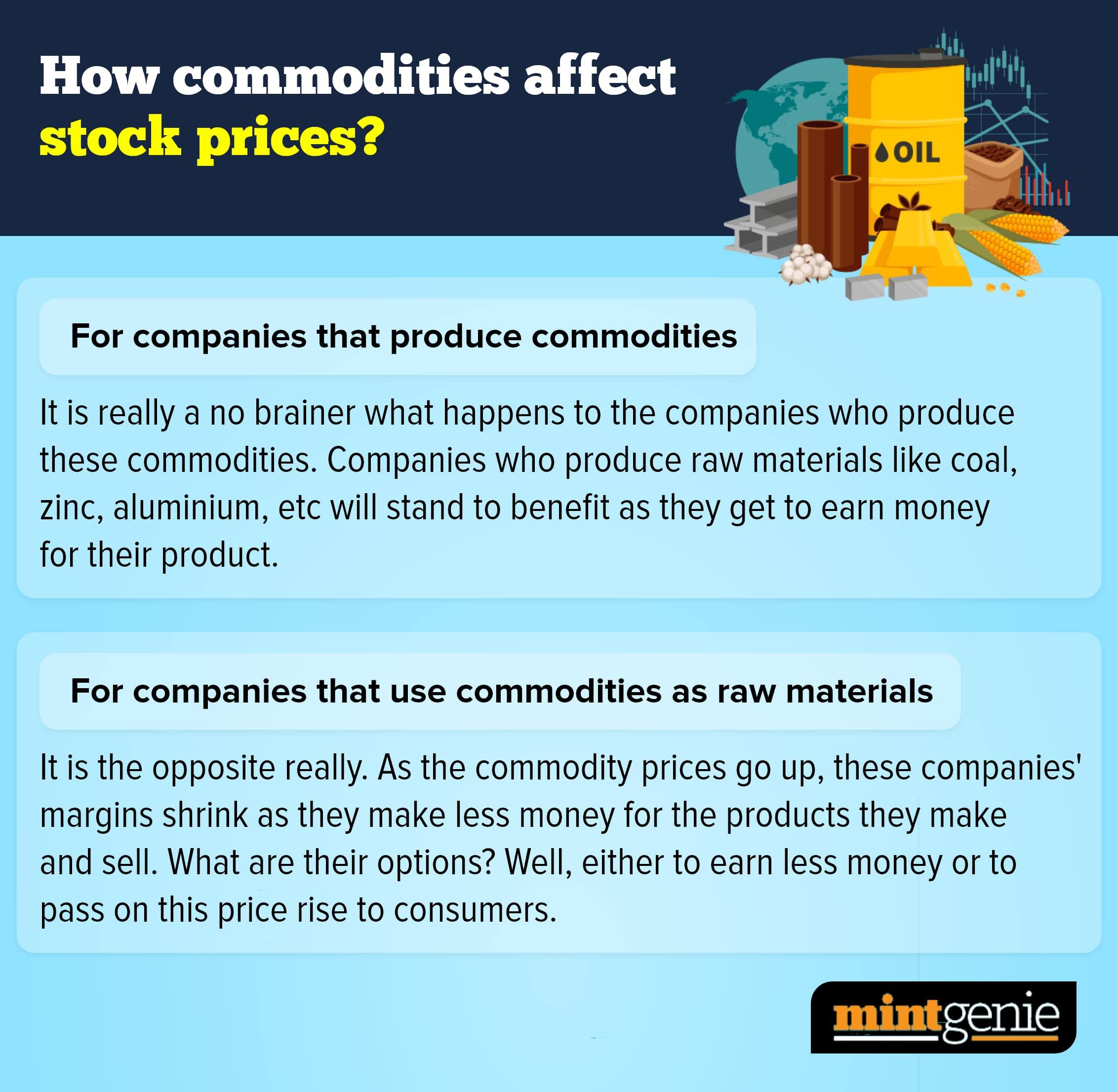

Analysts at ICICI Securities noted that there is a strong positive correlation between copper prices and revenues and the EBITDA of Havells. While copper prices increased at a CAGR of 8.5%, the company’s revenue grew at a 15.3% CAGR over the same timeframe. The brokerage added that a rise in copper prices may damage Havells' margins in the near term, but the company has historically been able to initiate pricing action to pass on the additional costs and maintain or improve margins.

With steady earnings growth, the stock price has also improved in spite of volatility in copper prices. Hence, the brokerage said that while the fear of higher copper prices is not necessary, there is no reason to cheer about the correction in copper prices.

The stock price has also moved in line with higher copper prices. Havells’ stock price has compounded at a CAGR of 40.1% over FY09-22 in spite of an increase in copper prices over the past decade, said the brokerage.

However, the brokerage pointed out that there is a correlation coefficient of -0.61 between Havells’ 1-year forward P/E and India's 10-year bond yields over FY09-22. Higher yields directly translate into an increase in the cost of capital, pulling valuation multiples down. “We believe any further rise in bond yields might hurt the near-term stock price performance of the company,” it added.

Due to the company's strong moats and growth opportunities, the brokerage anticipates Havells to report a PAT CAGR of 22.9% over FY22-FY24E and RoE to be higher than 20% over FY22-24.

Meanwhile, Ashika Research, another domestic brokerage firm, is bullish on Crompton Greaves Consumer Electricals and has initiated a 'buy' recommendation on the stock with a target price of ₹485/share, representing a 26.96% increase from the stock's previous closing price.

The company has acquired Butterfly Gandhimati (Butterfly is amongst the top three kitchen and small domestic appliances players in India) with plans to strengthen its position in the southern market.

The brokerage said, the company has shown its aspiration to become the largest kitchen appliance manufacturer in the country. Crompton has had numerous opportunities to add new growth levers, generate additional business synergies, deepen its market presence, and improve its margin profile.

Consumer preference is shifting towards smart, intelligent, and connected products and Crompton has made significant efforts towards R&D. The company remains on firm ground with diversified product offerings, leadership in the fan segment and encouraging growth in the lighting segment, apart from a recent foray into kitchen appliances, it said.

The company enjoys a 28%, 8%, and 17% market share in fans, LED lighting, and pumps, respectively, with industry-leading positions in all three segments. Moreover, the company generates more than 50% of its revenue from new products.

In the fan segment, Crompton has been able to gain market share with strong growth in premium and decorative products as well as the adoption of energy-efficient fans, Ashika Research said.

Going forward, the brokerage said the company will maintain its leadership position through cost-effective BEE implementation, building competency in electronics, and producing energy-efficient and premium products.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.