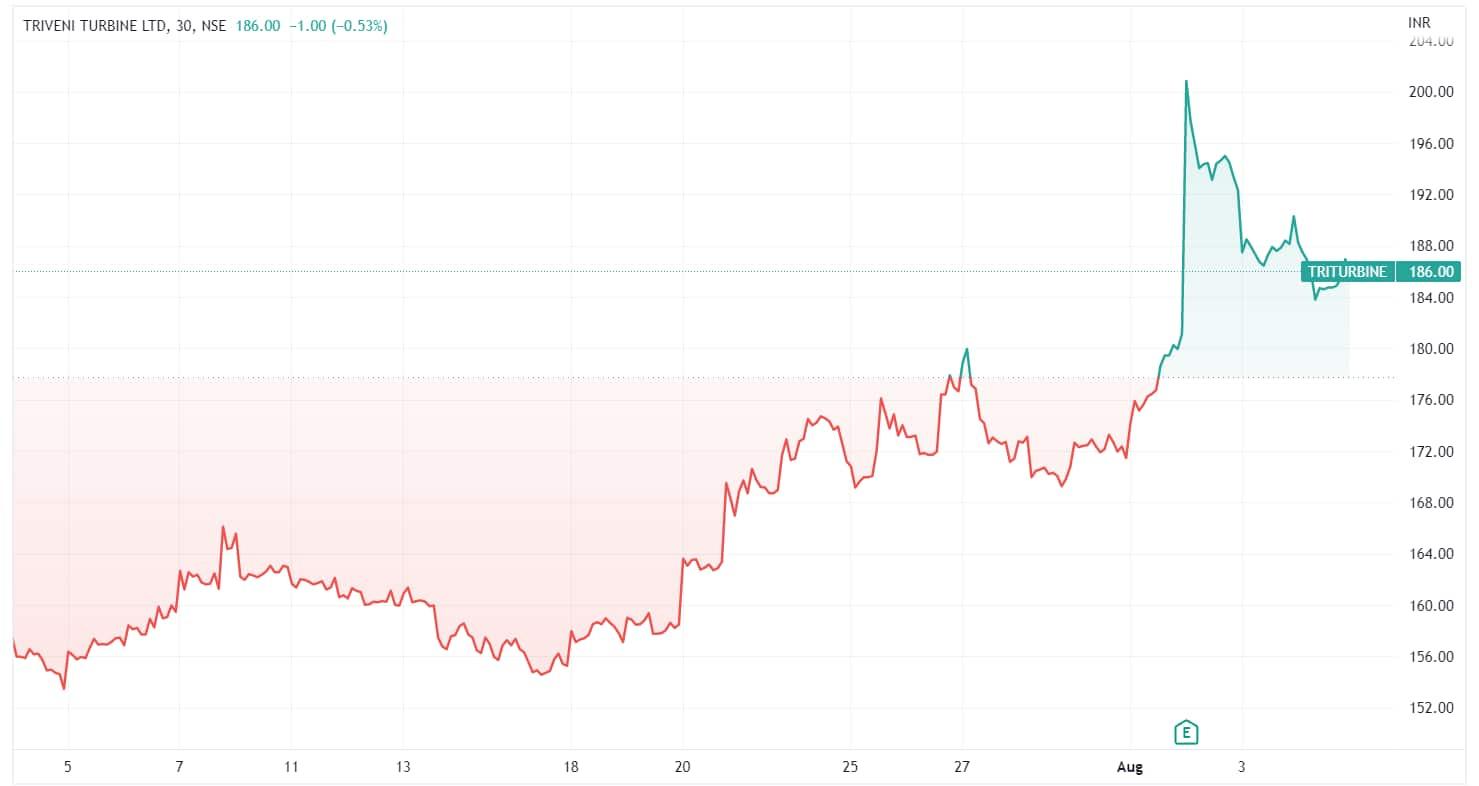

Shares of Triveni Turbines have surged 10% in the last 4 trading sessions after it reported a stellar performance in Q1.

The company posted a 39% jump in its consolidated net profit to ₹38.33 crore for the June-ending quarter as against ₹27.75 crore in the corresponding quarter of the preceding fiscal.

Total revenue increased by nearly 41% to ₹266.5 crore in the June-end quarter of FY23, compared to ₹189.6 crore in the same period last year. The expenses stood at ₹210.04 crore in the June quarter, compared to ₹148.3 crore a year ago.

The operating profit increased 36.03%, from ₹35.8 crore to ₹48.7 crore. The EBITDA margin fell marginally to 18.79% in Q1FY23 as against 19.43% in the corresponding quarter of last year.

The stock has been witnessing remarkable traction in the last one year while the market has been under pressure. The stock gave a 1-year return of 57.6% as compared to the Nifty Midcap100, which gave a return of 8.10% in the same period.

Over the last 3 years, on average, earnings per share have increased by 36% per year, but the company’s share price has only increased by 25% per year, which means it is significantly lagging behind earnings growth. During the same time period, it increased by 83.94 per cent.

Despite such strong gains in a volatile market, domestic brokerage firms are still positive on the stock.

Prabhudas Lilladhar believes a strong order book at ₹10.7bn, a robust enquiry pipeline, incremental opportunity with a foray into the 30-100MW market & API Turbines and a favourable product mix will likely aid margins and drive growth in the medium term. Accordingly, it expects a revenue/PAT CAGR of 27%/34% for FY22–24E.

"The near-term outlook remains positive given strong exports, continued domestic demand from sectors such as distilleries, steel, cement, pharma, pulp, paper, food processing etc., an enhanced addressable market in energy-efficient API turbines for the oil and gas industry, and 30-100 MW turbines and capacity expansion at Sompura plant to meet the increasing demand for the next couple of years," said Prabhudas Lilladhar in its research report.

The brokerage firm has a target price of ₹240/share on Triveni Turbines, which hints toward an upside of 28.72 per cent from its latest close.

On the other hand, Yes Securities is bullish on the stock post Q1 numbers. The brokerage firm has a target price of ₹273/share on the stock, implying an upside potential of 46.77 per cent from its previous closing price.

Yes Securities believes the company’s strong margin profile, lean working capital, healthy cash flows, balance sheet and long-term growth prospects (diversification in new types of turbines) will support its valuations and future projections. It expects the company to generate revenue and PAT CAGR of 25% to 29% from FY21 to FY24E.

Yes securities said the order book stands at a record high of Rs9.7bn, a growth of 64% YoY, of which domestic is ₹5.4bn and export has doubled to ₹4.3bn.

Meanwhile, the company has bagged an order from a prestigious client for a Waste to Energy project in Paris as the European region is witnessing a strong focus on renewable energy space.

An average of 05 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.