Shares of Steel Authority of India Ltd (SAIL) have lost over 70 percent of its investor wealth since hitting its peak in 2007.

From its record high of ₹293, hit in December 2007, SAIL has lost as much as 70.5 percent to currently trade around ₹86.

The stock is a perfect image of volatility. While it has given multi-bagger returns in the last 3 years, up over 100 percent, it has fallen 11 percent in the last 1 year.

However, from its 52-week low of ₹63, hit in June 2022, the stock has advanced 35 percent.

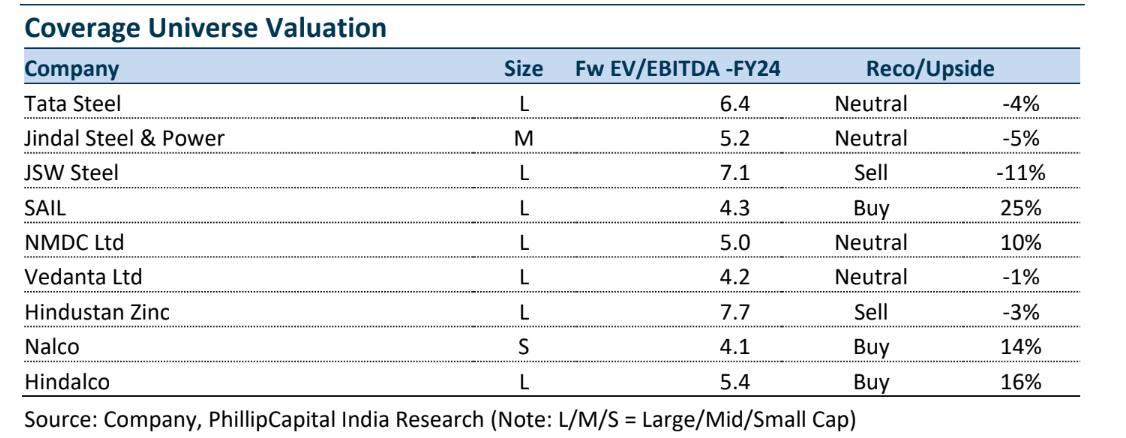

Despite the strong turbulence in the stock, brokerage house Phillip Capital recommends buying the stock and sees a 25 percent upside in the next 1 year. It has a target price of ₹105 for the steel stock. The brokerage believes SAIL is trading at attractive valuations.

SAIL is a maharatna company which is engaged primarily in steel manufacturing business in the country. The Company's segments include Bhilai Steel Plant, Durgapur Steel Plant, Rourkela Steel Plant, Bokaro Steel Plant, IISCO Steel Plant, AlloySteels Plant, Salem Steel Plant, Visvesvaraya Iron & Steel Plant and Others. It manufactures and sells a range of steel products, such as pig iron, cold rolled products, pipes, semis, structurals, TMT, galvanised products, bars, rods, rebars, plates, railway products, wheels and axles, hot rolled products, stainless steel products, etc. It was incorporated in 1973.

In the December quarter, the firm posted around a 65 percent fall in its consolidated net profit at ₹542.18 crore on account of higher expenses. It had reported a net profit of ₹1,528.54 crore in the same quarter last year. Its total expenses soared to ₹24,825.11 crore, compared to ₹23,209.88 crore a year ago.

Its total income also fell marginally to ₹25,140.16 crore from ₹25,398.37 crore in the year-ago quarter. In a statement, SAIL said it's crude steel production was at 4.708 Million Tonne (MT) in Q3 compared to 4.531 MT in the year-ago period. While sales were at 4.151 MT against 3.840 MT in the year-ago quarter.

"The challenging global situation and economic scenario all over the world had its impacts on the steel prices affecting the margins of the steelmakers," SAIL said.

"As expected SAIL reported good improvement in its 3Q performance driven by lower cost of production. However; increase in debt due to working capital requirement are a bit negative in the short run. With steel prices continuing to increase following the jump in raw material prices, SAIL would be relatively better than some of the peers as it saves on iron ore cost and has higher operating leverage which will benefit in the medium to long run," it said.

Phillip Capital believes debt has already peaked out while EBITDA has more room to grow. SAIL continues to trade at discount to its peers and historic valuation, it added.

Apart from SAIL, the brokerage has buy calls only on Nalco and Hindalco from its metal coverage universe with 14 percent and 16 percent upside expectations, respectively. Meanwhile, it recommends selling JSW Steel and Hind Zinc, where it sees 11 percent and 3 percent downside, respectively.

Meanwhile, recently brokerage house Sharekhan had maintained a hold call on the stock with a target price of ₹95.

The brokerage expects that a gradual margin recovery would support improvement in earnings of steel players, but thesteel upcycle (as seen in 2020-2021) may not be around the corner given demand concerns in the US/Europe and concern of rising coking prices. Although SAIL has guided to lower debt, but we believe that the major balance sheet deleveraging cycle is largely over as the company would focus on capex to expand capacities, it added.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.