A long-term debt cycle is less understood and even less spoken about. Ray Dalio, the founder of Bridgewater Associates, popularised the concept of the long-term debt cycle in his book “How the economic machine works”.

In the book, he talks about how the ‘debt swing’ occurs in two cycles -short-term (5 to 8 years) and long-term (75 to 100 years).

Most of our conversations are around short-term debt cycles as they are easier to track and are more immediate.

Let us understand the short-term debt/credit cycle which lasts for about 5-10 years.

During an economic expansion, the system's debt level keeps increasing until the economy becomes susceptible to an economic shock. A negative catalyst eventually triggers the shock leading to economic contraction and deleveraging.

Policymakers usually respond by offering lower rates and fiscal stimulus to offset this otherwise deflationary period. Many defaults occur, leading the system to clean out some of the excesses of malinvestment and unproductive leverage (for example, the tech bubble of 2000).

Then again, it is lend - borrow - repeat!

Policymakers in the developed economy have typically overused monetary policy, encouraging the use of leverage. As a result, every short business cycle in modern US history has ended with higher debt (as a percentage of GDP) and lower interest rates compared to the previous cycle.

The debt/GDP makes higher highs and the interest rate make lower lows. As these short-term debt cycles string together, debt levels become unsustainable and interest rates become zero bound –marking the end of a long-term debt cycle.

Since the debt levels are too high – the usual policy tools no longer work as they could lead to an unprecedented deflationary burst. Hence, policymakers are forced to use unconventional tools.

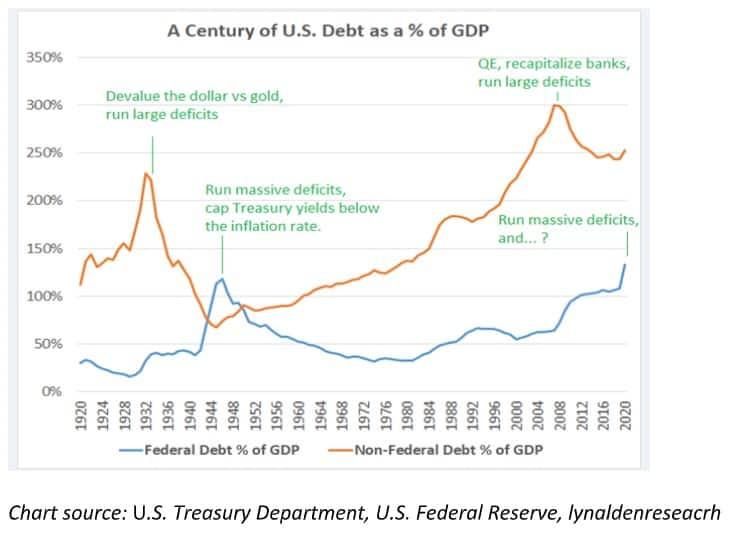

Take a look at the chart below. The US has witnessed two long-term debt cycles over the last century. The Great Depression in the 1930s and the Great Financial Crisis in 2008 -10 marked the peak of private debt/GDP and a banking crisis.

The 1940s (WW-II) and 2020 (war against COVID) resulted in an unprecedented fiscal response, marking the peak in fiscal debt/GDP and leading to inflation. The private debt peak preceded the public debt peak in both cycles.

The debt levels today are similar/higher than the peaks seen during WW-II – indicating that the developed world could be at the cusp of a long-term debt cycle.

Russel Napier, a renowned market strategist and the co-founder of ERIC (a well-known platform for research) also believes that the following decade will be similar to the 1940s and the “unconventional policies” used to deflate the long-term debt bubble without crashing the economy will be similar to that time.

Policymakers may attempt to reduce debt/GDP by increasing the denominator (nominal GDP, which is real GDP+inflation) through higher fiscal policy and inflation.

The interest rates will be capped to levels much below inflation which will allow governments to borrow and service their debt.

The cash savers and debt investors will end up bearing the brunt as the real yields become negative (inflation and interest rate).

Their purchasing power will get eroded over the long term. When these policies were deployed post-1940s, they resulted in negative returns for over three decades.

Few financial experts like Russel believe that there will be a government-directed capex boom, driven by energy dependence, reshoring and climate change whereas long-term yields will be capped.

This view is already starting to play out although Fed is still hawkish unlike other central banks (ECB and BOE). They have intervened to keep long-term yields under check despite high inflation. Bank of Japan has already capped its yield to 0.25%.

The unfolding of the long-term debt cycle and the stated policy response may result in the reversal of multiyear investment trends.

The macro backdrop could do a full 360-degree turn when compared to the last few decades. It could mean an era of inflation over stagnation and the domination of fiscal policies over monetary policies.

This typically means that investments which have done well in the past, may or may not do well in the future.

Investors may have to get “comfortable” investing in strategies or investments which could have underperformed over the past 10 – 15 years.

Conversely, not every dip is an investment opportunity. Preference should be for economies with more conventional and traditional policies with lower debt than the western economies.

The focus should ideally be on real returns and on the protection of purchasing power, especially in an inflationary environment. It would be wise to build real assets and inflation hedges in the portfolio.

Mark Twain once quoted that “History does not repeat itself, but it does rhyme”. The monetary/credit cycle is no exception as we see glaring similarities between both debt peaks.

Lastly, the world never comes to end. So, don’t fall prey to any doomsday predictions. It has seen these unprecedented levels of inflation and debt levels before and has managed to navigate through them.

(The author of this article is Senior Executive & Vice President, IIFL Wealth)

Disclaimer: The views and recommendations given in this article are those of the author. These do not represent the views of MintGenie.