After nearly 40 months, India's banking system's liquidity has slipped into a deficit as credit demand in the economy rises exponentially. On Tuesday, the Indian central bank made the biggest financial infusion into the banking system since 2019. The RBI injected ₹21,800 crore into the banking system, according to central bank data.

As the Indian economy recovered from the COVID-19 slump, credit demand has grown substantially. Credit demand for personal loans, industrial loans, service sector loans, and loans for agricultural and allied activities has increased strongly.

When the Indian economy was doing well, the Russian-Ukraine conflict broke out in February, and as a result, commodity prices skyrocketed, with crude oil prices approaching $140, pushing inflation to multi-decade highs, leaving central banks with no choice but to hike interest rates.

On May 04, the RBI raised its key lending rate by 40 basis points to 4.40 percent with immediate effect. The central bank also raised the cash reserve ratio by 50 basis points. This was the first rate hike in policy rates since August 2018.

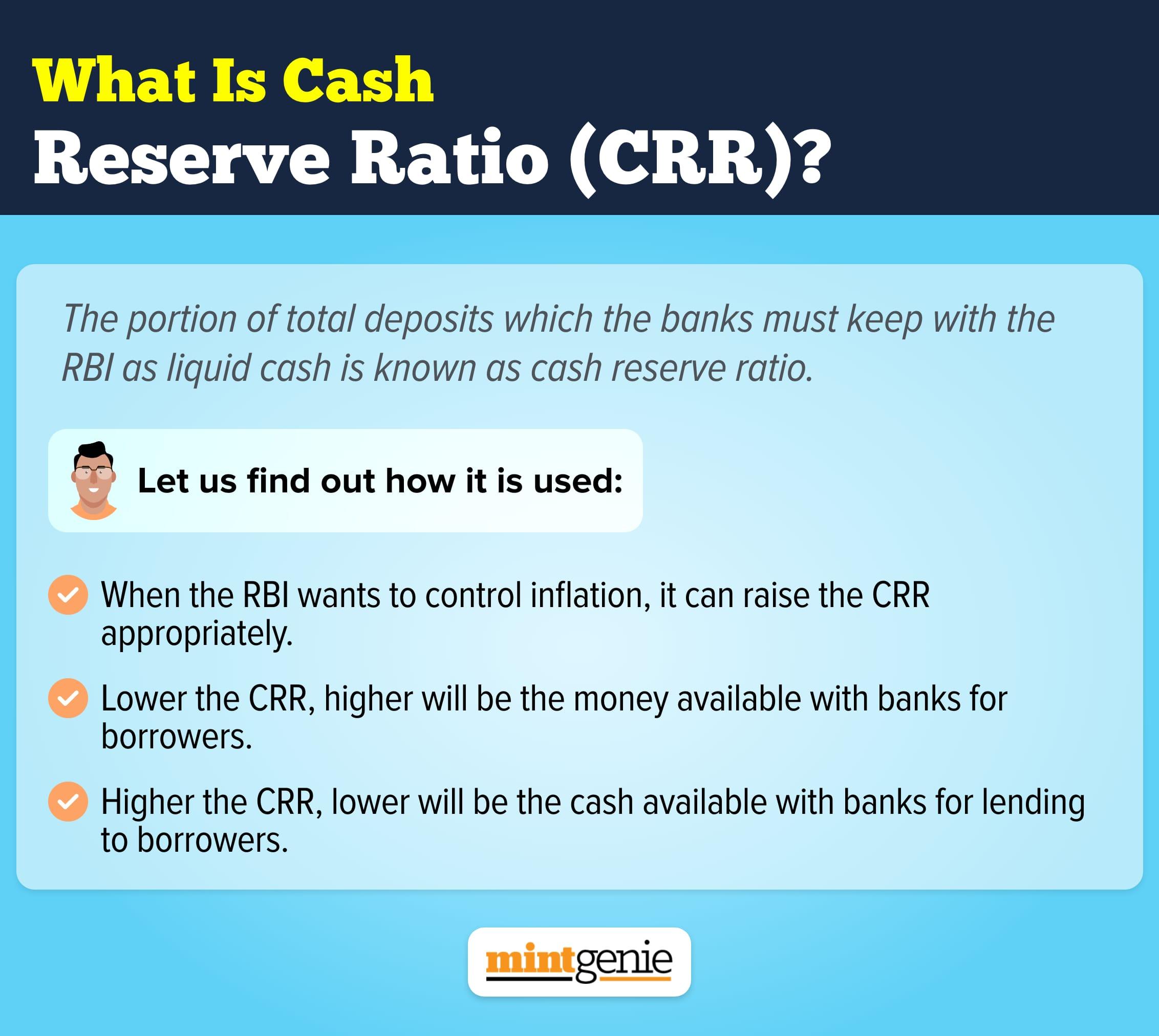

The cash reserve ratio is the percentage of deposits that banks keep with the RBI, and with the announcement of the CRR increase to 4.5%, it sucked approximately ₹90,000 crore from the system. This has kept banks' liquidity tight and hampered base money growth.

In June, after excess liquidity fell to nearly ₹3.5 lakh crore, the Indian Banks' Association requested the RBI not to raise the CRR threshold in the upcoming monetary policy. Banks also requested the RBI to allow them to spread provisions for mark-to-market losses over several quarters in order to support credit growth, but the RBI turned down the banks' request.

In response to the Bank's request, the RBI governor, Shaktikanta Das, said that " Banks cannot always rely on the central bank's money and they must mobilize deposits to fund credit offtake in the economy."

Meanwhile, the yield on the Indian 10-year government bond traded close to a 3-year high of 7.6% in June as a result of the rise in crude oil prices. Major public-sector banks' margins have been significantly impacted by this in Q1FY23.

The country's largest lender, SBI, reported a 6.70 percent drop in its standalone profit after tax at ₹6,068 crore for the quarter that ended June after it booked ₹6,549 crore in MTM losses on its investment book. The lender reported a profit after tax (PAT) of ₹6,504 crore on a standalone basis in the April-June quarter of fiscal 2022.

Punjab National Bank, on the other hand, reported a 70% drop in stand-alone net profit to ₹308.44 crore in the June quarter, compared to a net profit of ₹1,023.46 crore in the previous year. It posted an Rs. 1,409 crore MTM loss in the June quarter.

As a part of SLR (Statutory Liquidity Ratio), banks will maintain large holdings of government securities, including state development loans and treasury bonds. Any volatility in the bond market is expected to affect their treasury income.

Despite the Reserve Bank of India's consecutive rate hikes, credit growth continues to rise. In the fortnight ended July 29, the credit growth in the system stood at 14.52 percent. But deposit growth was merely 9.14 per cent during the same period, which led to a spread of 538 basis points.

To fund the incremental credit demand, Indian banks have raised funds via certificates of deposits because banks have seen that CDs are currently the best option for raising funds as bond yields are moving high in line with the repo rates. According to ICRA analysis, banks' outstanding volumes have risen by 243 percent as on July 1, 2022, on a year-on-year basis, to ₹2.4 lakh crore.

As per media reports, in August the liquidity surplus in India's banking system has fallen below ₹1 trillion and averaged around ₹1.4 trillion, down from ₹1.9 trillion in July and ₹2.92 trillion in June.

Further, the year-on-year growth in bank credit growth accelerated to 15.32% in the fortnight ended August 12, 2022, the fastest in three years. Total loans as of August 12 stood at ₹124.3 lakh crore.

After June, RBI in August again rejected the bank's request to allow flexibility in the accounting of MTM losses on their balance sheet, banking sources told FE.

Analysts are now expecting that the liquidity in the banking system will remain in deficit in the second half of this year on the back of rising credit demand and a rise in the circulation of currency notes ahead of the festive season.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.