The key function of central banks is to maintain price stability, which is accomplished through the use of monetary policy instruments. Any move by the central bank usually has an impact on the economy and on financial markets. Before making such decisions, the Reserve bank of India will conduct a series of forward-looking surveys on a quarterly basis to learn more about - How consumers are reacting to inflation, how businesses are dealing with input cost pressure, and what they anticipate about future cost pressure and about bank lending growth. Answers to these important questions will help the central bank's policy decisions.

What do the RBI's forward-looking surveys reveal about the Indian economy?

TL;DR.

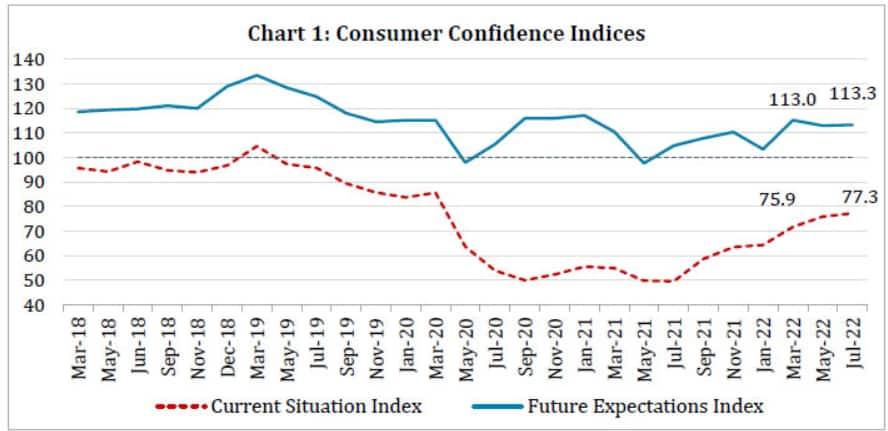

The current situation index (CSI) has improved by 1.4 points from 75.9 in May 2022 to 77.3 in July 2022. In addition to that, the future expectation index registered only a marginal improvement, rising to 113.3 in July from 113 in May.

Here is a look at the key findings from the recent survey results released by the RBI on August 05.

Consumer Confidence Survey

The consumer confidence survey shows how confident consumers are about the economy, financial conditions, demand, and consumption.

The survey was conducted from July 07 to July 14, 2022, in 19 major cities, covering 6,083 respondents.

The survey collects current perceptions as well as one-year forecasts of the general economic situation, employment scenario, overall price situation, and personal income.

There are two Indices in the CCS one is the Current Situation Index (CSI) and the other was the Future Expectations Index (FEI).

Consumer Confidence Survey

The RBI said that consumer confidence continued to recover in successive rounds of the survey after the historic low recorded in July 2021, though it remained in the pessimistic zone.

The current situation index (CSI) has improved by 1.4 points from 75.9 in May 2022 to 77.3 in July 2022. Generally, index figures below 100 are considered to be in pessimistic territory, but if the index is above 100, it indicates optimism.

The respondents are negative about inflation, job creation, the economic situation, and income levels in the current year.

In addition to that, the future expectation index registered only a marginal improvement, rising to 113.3 in July from 113 in May. The majority of the households reported a rise in their current spending and anticipated that the trend would continue for the year ahead, the survey showed.

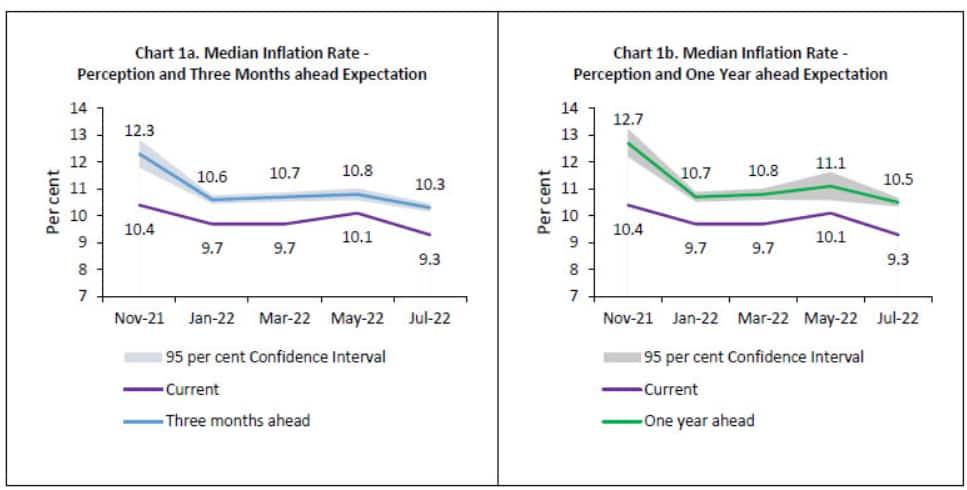

Households’ Inflation Expectations Survey

The HIES survey was conducted in 19 major cities. The results are based on responses from 5,935 urban households.

Households’ median inflation perception for the current period moderated by 80 basis points to 9.3 per cent in the latest survey round, the RBI said

Further, for the three months and one year ahead, median inflation expectations also declined by 50 bps and 60 bps, respectively, from the May 2022 round of the survey.

Inflation Expectation Survey

The share of households expecting higher inflation has declined for all product groups from the previous survey round.

Meanwhile, the top concern for all households in the country is inflation, which is currently running at about 7 per cent. In June, India's retail inflation came down slightly to 7.01 per cent, as against 7.04% in the previous month.

However, the CPI has breached the upper limit of the RBI target range of 2–6% for the sixth consecutive month and has remained above 7% for the third consecutive month. So far this year, the Reserve Bank of India has raised interest rates by 145 basis points, to 5.40%.

OBICUS Survey

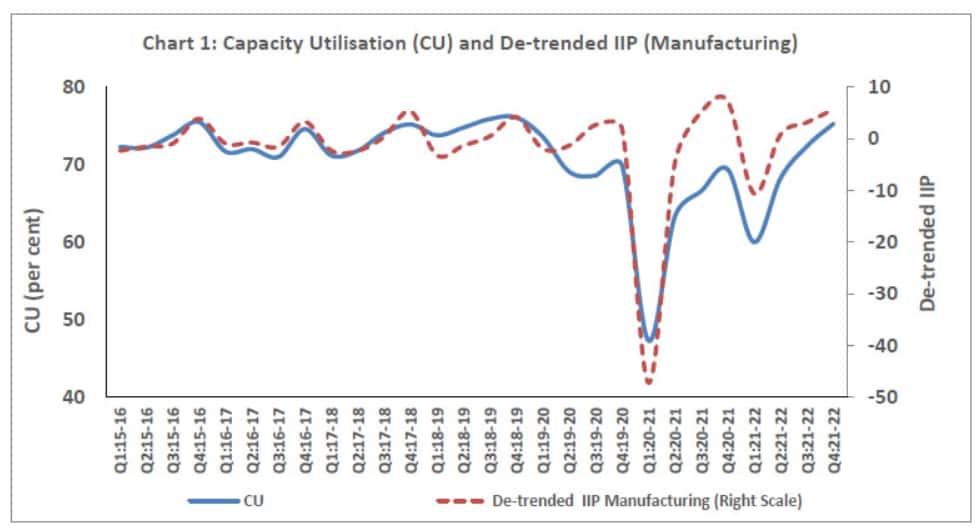

The Order Books, Inventories and Capacity Utilisation Survey (OBICUS) provide a snapshot of demand conditions in India’s manufacturing sector. The survey covers the reference period between January and March 2022 and covers 765 manufacturing companies.

As per the survey, capacity utilisation has picked up pace from 68.3 per cent in Q2, 2021-22, to 72.4 per cent in Q3, and 75.3 per cent in Q4, indicating economic recovery and improving demand conditions.

However, new order book growth has fallen to 5.6 per cent in Q4 FY22 from 10.5 per cent in Q3 FY22.

OBICUS Survey

Further, RBI’s OBICUS also showed that the growth in backlog orders stood at 4.7 per cent quarter-on-quarter in Q4 as against 3.5 per cent in October-December 2021 (Q3, 2021-22), while pending orders growth was seen at 4.6 per cent in Q4 as against 7.8 per cent in Q3.

The average amount of new order books for 207 companies in January-March this year stood at ₹222.4 crore compared to ₹224.4 crore in October-December 2021 for 205 companies.

Bank Lending Survey

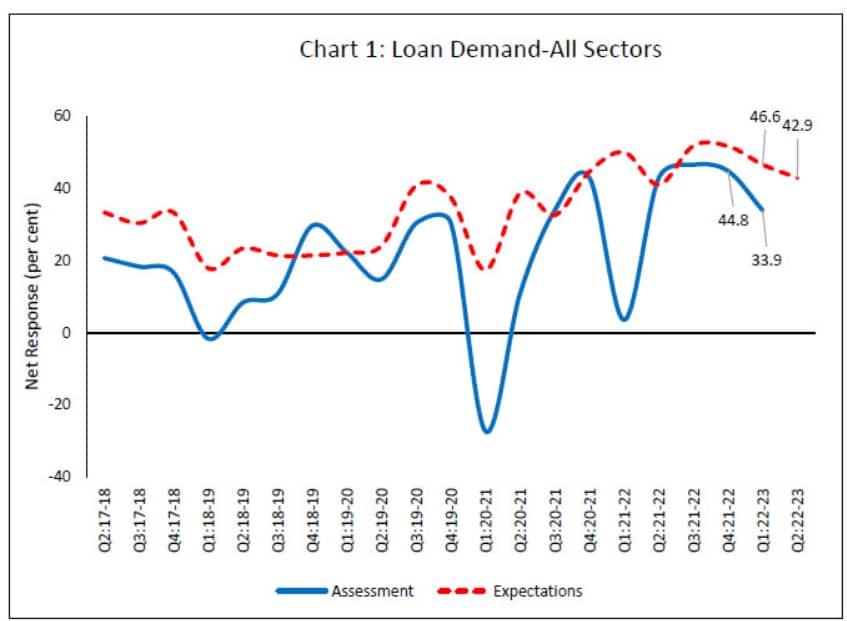

The Reserve Bank of India released its 20th round of its quarterly Bank Lending Survey. The survey captures the qualitative assessment and expectations of major scheduled commercial banks on credit parameters (viz., loan demand and terms & conditions of loans) for major economic sectors.

The survey showed that bankers’ assessment of loan demand for the period remained positive for all major sectors. However the sentiments were somewhat toned down from the level reported in the previous quarter, RBI said.

Bank Lending Survey

Bankers were positive on loan demand from all major sectors during Q2:2022-23 though the level of optimism was somewhat lower than the previous survey round.

Sentiments on overall loan demand in the second half of 2022-23 remain upbeat across the major categories of borrowers, the RBI said.

Industrial Outlook survey (IOS)

This survey captures a qualitative assessment of the business climate of Indian manufacturing companies for Q1:2022-23 and their expectations for Q2:2022-23. Overall 1,239 companies have participated in this survey.

The survey said that businesses were optimistic about demand conditions as revealed in their positive assessment of production, order books, capacity utilization and foreign trade.

However, Manufacturers assessed a rise in costs of raw materials as well as in salary outgo during Q1:2022-23; they also perceived a rise in the cost of funds.

Sentiments on selling prices hardened in consonance with input cost pressures; respondents’ perception of profit margin turned marginally positive during the quarter.

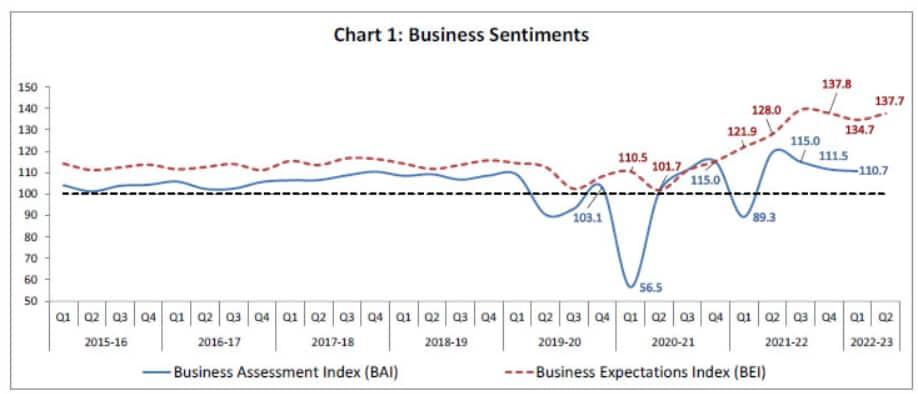

IOS Survey

Overall, business sentiments in the manufacturing sector remained positive; the business assessment index stood at 110.7 in Q1:2022-23 as compared with 111.5 a quarter ago, the survey showed.

On the expectations front, Businesses retained their optimistic outlook on demand conditions as reflected in their expectations on production, order book, and employment for Q2:2022-23.

They expect a rise in raw material cost, staff cost and cost of financing likely to continue in the Q2FY23.

Overall, the Business expectation index improved to 137.7 in Q2FY23 from 134.7 in the previous quarter. For the second of FY23, the Business anticipates ease in input cost pressure and a rise in selling prices.

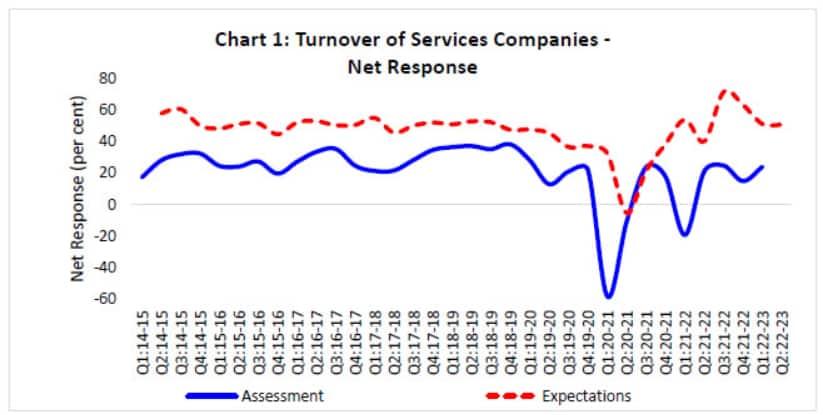

Services and Infrastructure Outlook Survey

This forward-looking survey captures qualitative assessment and expectations of how Indian companies in the services and infrastructure sectors on a set of business parameters relating to demand conditions, price situation and other business conditions.

In the latest round of the SIOS survey 758 companies provided their assessment for Q1:2022-23 and expectations for Q2:2022-23, RBI said.

The survey shows that business in the service sector has seen improvement and employment conditions have improved further in Q1FY23.

Services and Infrastructure Outlook Survey

However, perceived cost pressures emanating from the cost of finance, input prices and wages, and assessed a rise in selling prices, when compared to the previous survey round, the RBI said.

Services companies remained pessimistic on profit margins for the Q1FY23 assessment.

Respondents say that the cost price will continue with gradual easing in the latter half of the year.

On the other hand, Infrastructure companies revealed a positive assessment of the overall business situation as well as their turnover.

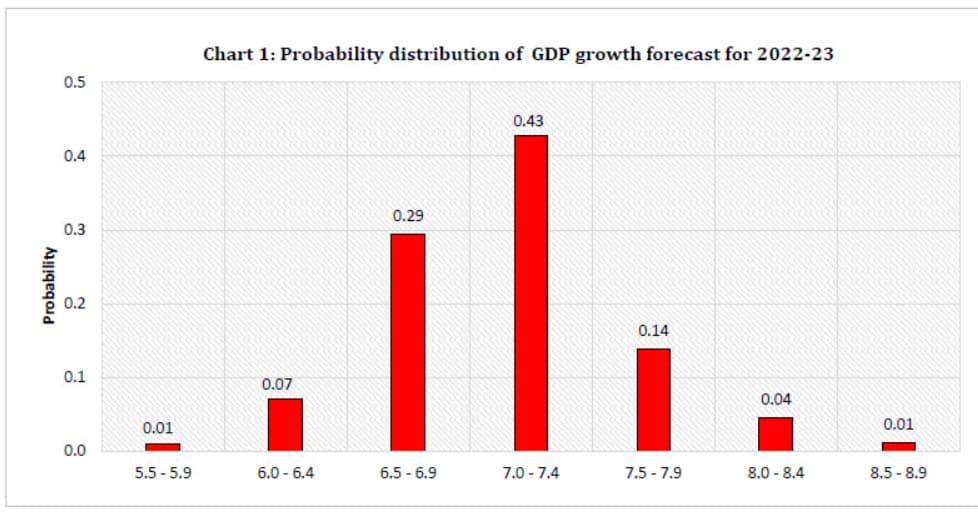

Survey of Professional Forecasters (SPF)

The survey of 42 professional forecasters on key macroeconomic indicators such as GDP growth rate and inflation rate in the current year and the next financial year.

The 42 panellists expected GDP to grow by 7.1 per cent in 2022-23 - projections revised down by 10 basis points (bps) from the last survey round, it is expected to grow by 6.3 per cent in 2023-24, the RBI said.

GDP Forecast

SPF panellists have placed GDP growth forecasts in the range of 6.3 – 8.3 per cent for 2022-23 and in the range of 5.0-7.8 per cent for 2023-24; the range for 2022-23 has considerably narrowed from the last SPF round, indicating more certainty around the median forecast, the survey showed.

Forecasters have assigned the highest probability to real GDP growth in the range of 7.0-7.4 per cent in 2022-23 For 2023-24, the highest probability has been assigned to the range of 6.5-6.9 per cent.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

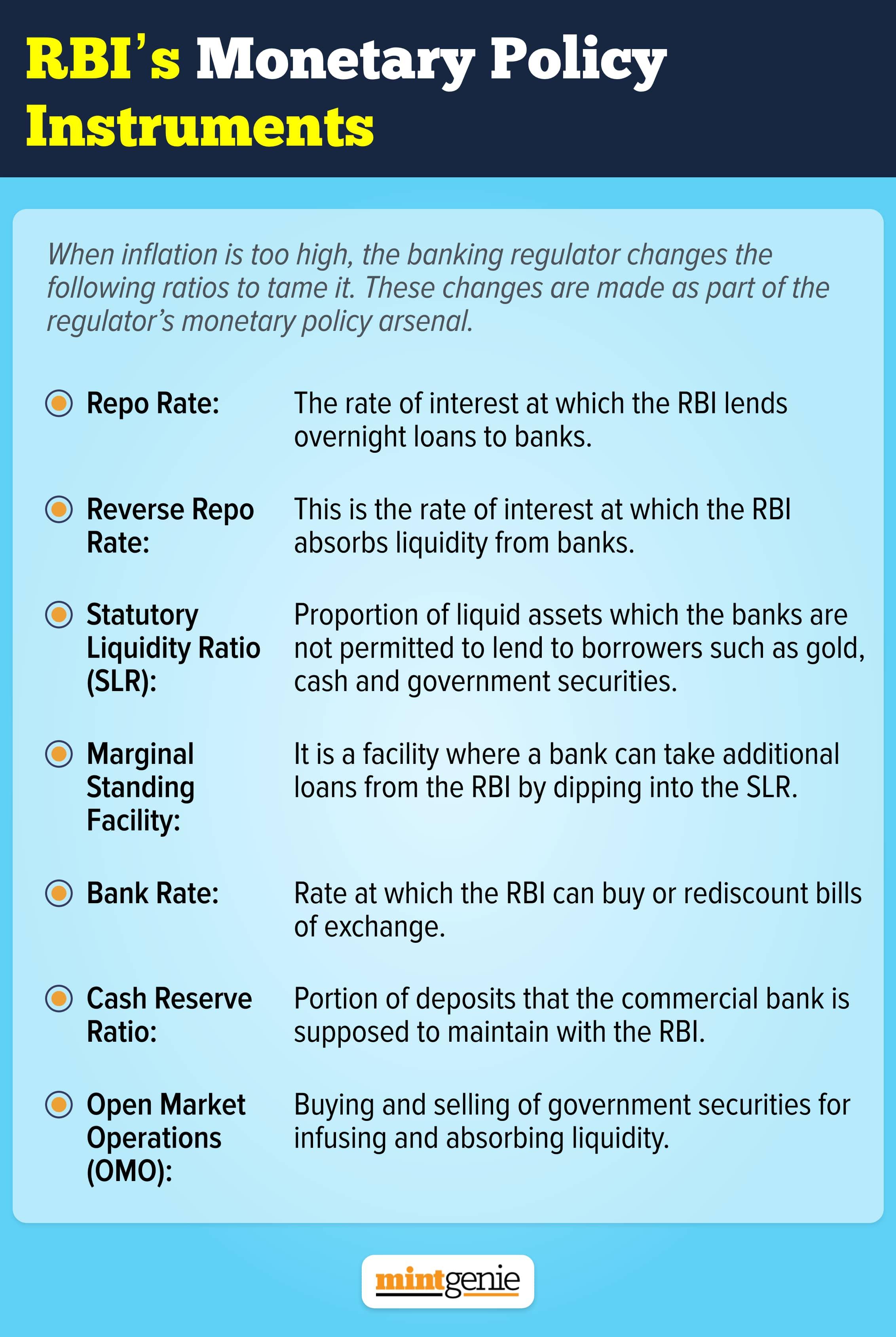

These are the RBI's monetary policy instruments.

First Published: 12 Aug 2022, 09:08 AM IST

Topics to follow

Related Stories

personal finance

How does the RBI influence your borrowing decision by changing the repo rate

Kirti Jhapersonal finance

Fixed Deposits: 7 banks that have raised interest rates in August. Details here

Deepika Chelani