In an initial public offer (IPO), a company invites public to invest in its equity shares, thus increasing the number of outstanding shares. Later, the company could invite those shareholders to sell some of the shares back to the company under a process known as ‘share buyback’.

In simple words: a share buyback is a transaction wherein an organisation buys back its own securities. A company, at times, does this because its leadership believes that its share prices are undervalued. There are essentially two options to carry out a share buyback: company can either buy directly from the market or gives shareholders the option of tendering their shares directly to the organisation. For instance, TCS has offered a buyback of 4 crore shares worth ₹18,000 crore at ₹4,500 per share.

The share buyback reduces the number of outstanding shares, which increases the demand for shares, and consequently the share price. As a result, demand for share increases, thus pushing its price higher. For instance, soon after Amazon authorised a $10 billion buyback plan on Wednesday, company's shares rose 7 percent in the extended trading. However, there is a risk that share price could even fall after a share repurchase.

What are the immediate fallouts?

There are immediate after effects of share buyback of a company. On one side, the amount of available cash reduces on company’s balance sheet — equivalent to the sum company spent on buying back of shares. At the same time, shareholders' equity also declines on the liability side of balance sheet.

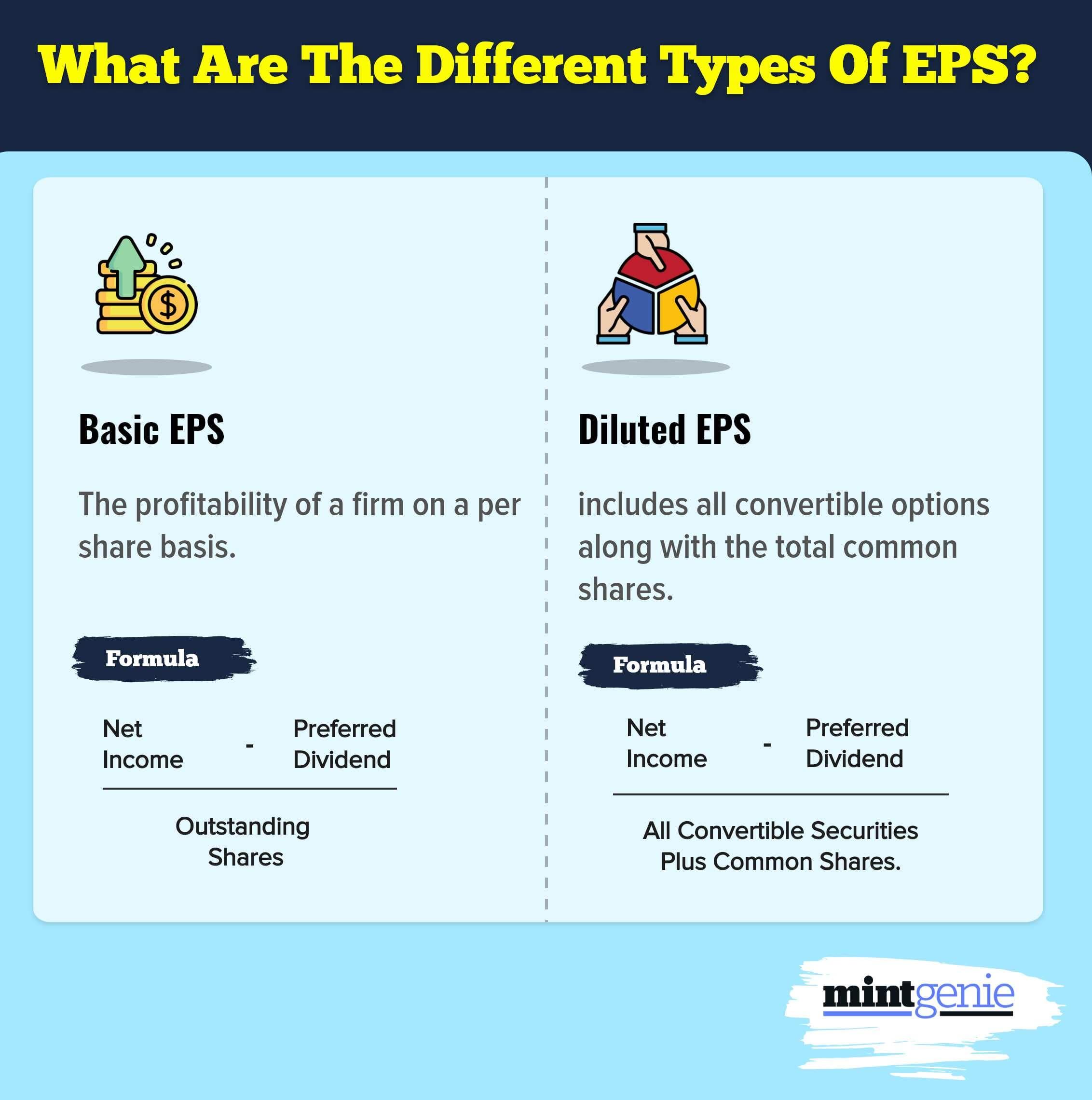

One key benefit of share buyback is that it is reflected positively in the earnings per share (EPS). When the number of outstanding shares falls while the total dividend payout remains the same, earning per share stands to increase. EPS is calculated by the formula: total net income/ number of outstanding shares).

Not only this, buyback can even obliterate fall in net income as the decline can be compensated by the increase in EPS. Sample this: Let’s suppose a company XYZ’s net income falls by 10 percent from ₹10 crore to ₹9 crore in fiscal 2021.

Soon after this, the company announces a share buyback which reduces the number of outstanding shares from 100,000 to 90,000. This can be made possible by huge cash reserves despite the company’s fall in income.

So, before the buyback, the earning per share is calculated by the formula i.e., total net income/number of outstanding shares = 10 crore/ 1,00,000 = ₹1,000. After the buyback, the EPS= ₹9 crore/ 90,000 = ₹1,000.

In both the cases, the EPS stays the same despite a fall in net income.

Some of the advantages

It is usually done when the company’s management sees further scope in the increase of share price. After share buyback, share’s earning per share (EPS) increases, which pulls price-to-earnings ratio (P/E) downward — assuming the stock price remains the same.

The lower P/E ratio could imply the share price represents a better value, which makes the stock more attractive to potential investors.

Disadvantages of buyback

Although the disadvantages are not many, but a share buyback might give an impression —and rightly so — to the investors that the company does not have other profitable opportunities for growth, an issue for growth investors who are eyeing revenue and profit increases.

Repurchasing shares can even put a business in a vulnerable situation if the economy takes a downward spiral, and the company stares at some financial obligations which it cannot meet.

However, there are a range of criticisms of share buyback. The sceptics say that buyback restrains companies to reinvest profits more meaningfully in the company in terms of putting new factories, R&D, equipment, higher wages, and worker retraining.

Whereas the proponents say that the share buyback puts moneyback back to where it belongs — shareholders.