As an experienced swimmer will understand, the experience of swimming in a pool is vastly different from that of open waters. While the pool is predictable, open waters can be subject to strong currents, extreme temperatures and low visibility.

Those who train to compete in a pool may doubt their own ability to achieve a certain goal, whereas open water swimmers may have to deal with unforeseen circumstances that could lead to the non-completion of their swim. Unlike a pool, open waters don’t offer immediate safety such as lifeguards or a solid floor for one to stand on.

Indian fixed-income investors have been experiencing stormy weather and unchartered waters in recent times.

Since the Russia-Ukraine conflict, the dominant global macro theme has been inflation and a significant re-pricing of the yield curve, with market participants adjusting to both the speed and quantum of monetary policy reactions.

Since March 2022, the FOMC has raised the federal funds rate by a cumulative 225 basis points, the fastest pace of tightening in nearly 30 years while RBI has effectively moved the policy rates by 180bps since April 2022.

The tightening of monetary and fiscal policies, rising income squeeze from high commodity prices and ensuing asset market corrections due to the tight financial conditions have brought up the spectre of a synchronised growth slowdown.

These factors have led to the possibility of a sharp global economic recession.

Concerns of a global slowdown and the subsequent fall in commodities (from their March 2022 highs) have led to a bond rally on expectations of “peakflation” and consequent softening in RBI policy normalisation in the near term (further catalysed by the possible inclusion of India in global bond indices).

However, there are still lingering concerns that inflation can persist. The continued Ukraine conflict, OPEC+ protecting its pricing and China implementing rigorous lockdowns can keep supply chains disrupted.

In other words, the main drivers of our domestic monetary policy are likely to be commodity prices (mainly crude) and a sharp global recession, which can thaw aggressive policy normalisation by the Fed.

Assuming crude prices remain range-bound, let us examine the other variable i.e., easing of the global central bank policy path.

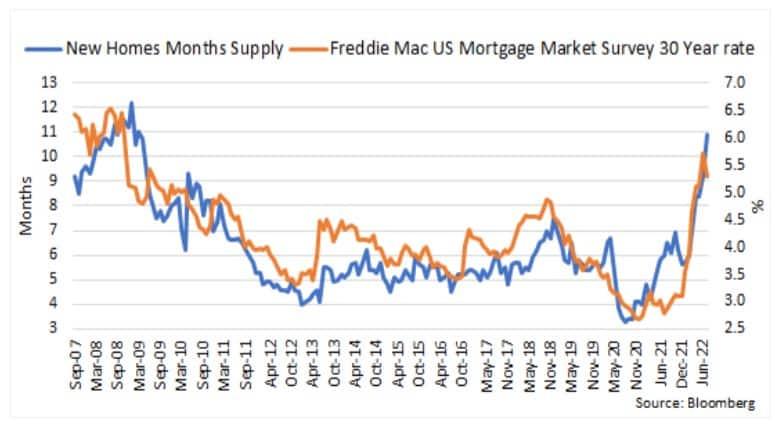

In a matter of months, the pandemic and red-hot US housing market are pulling back. As can be seen from the chart below, new homes inventory in months of supply has gone back to March 2009 levels.

Given housing’s 16.6% overall share of US GDP (Source: Bureau of Economic Analysis, 2QCY22), the decline in real estate activity, if continued, can have wider repercussions on broad economic growth.

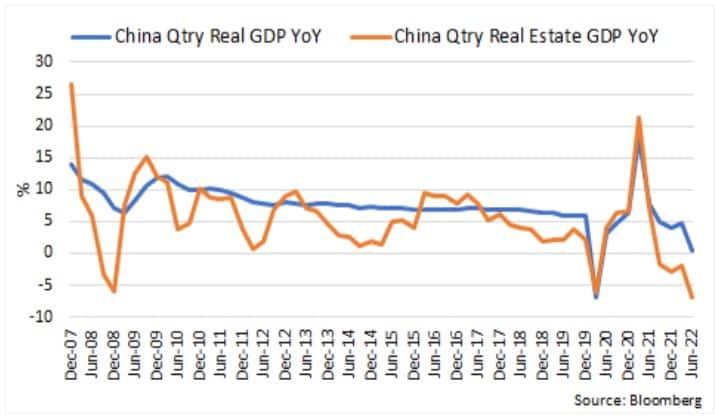

Fears of a hard landing in China, especially after cracks appeared in their real estate sector, have further sparked rising concerns of a vicious global slowdown.

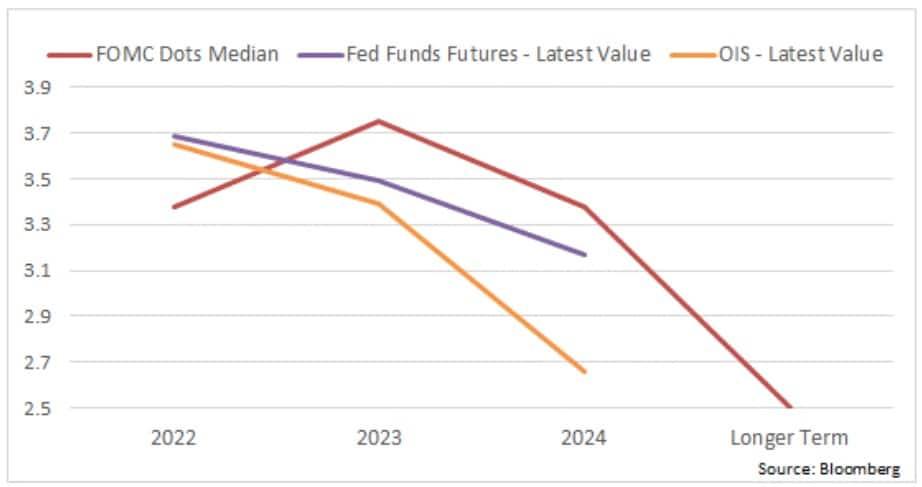

As can be seen in the chart below, the OIS curve is pricing in a rate cut in 2023 and 2024 to take the Fed fund rate to 2.65% compared to the FOMC Median of 3.375% at the end of 2024 (as on August 29, 2022).

While we may be looking at a global slowdown in the next 12 months, the current climate is too premature to declare the collapse of inflation and subsequent monetary easing, with too many moving parts. The strongest unemployment rate since the 1950s still portends a robust labour market.

Firstly, healthy private sector balance sheets are providing support that can be bolstered in by fading supply-side drags and additional fiscal stimulus.

Secondly, inflation is falling but it’s yet to move to central bank comfort levels, as rising wages and inflation expectations can offset the declining commodity prices.

Thirdly, the lack of inventory buffer in commodities leaves the market vulnerable to unplanned supply outages.

We may also need to distinguish between a technical recession (consecutive GDP contraction) and an economic recession, which may manifest in the form of (1) severe unemployment (the 1930s, US), (2) institutional failures (example: LTCM 1997, Lehman Brothers 2008), (3) sovereign debt crisis (example: Greece 2010) which may require the central bank to shift the focus to growth.

However, the extent of intervention could still depend upon the deviation of inflation from the target.

We must keep in mind that central banks are already in the middle of narrowing their ‘credibility deficit’, i.e., their inflation targeting credentials, which may necessitate more restrictive rates.

Their premise — that a sustainably lower inflation can be “purchased” with a modest slowdown — is still being tested and its full impact may remain unknown for years.

Conclusion: Hold on to your anchor

Just like an anchor helps creates stability in rough waters, fixed income investors can benefit from answering two simple questions when markets get swayed by the push and pull of daily information:

(1) What is the terminal rate expectation from RBI and has any data point emerged to challenge the view?

We continue to expect that given the sanguine domestic growth drivers and the goal of 4% inflation still a long way away, the terminal policy rate is expected to be in the range of 6-6.5% to maintain a reasonable real rate buffer over FY24 inflation and Fed’s terminal policy rate.

(2) Is the market broadly pricing the risks and opportunities?

We believe that the terminal policy rates are largely priced in the majority of the yield curve, most notably in the one-to-five-year space.

The curve has flattened in the near term due to lower SDL supply and possibilities of bond index conclusion. The 5–10-year part of the curve could once again steepen as we get closer to the end of the RBI hike cycle.

Given the meaningful correction in money market and bond yields in the last six months, we believe investors with tolerance for intermittent volatility and 6-12 months horizon may consider allocation towards money market and low-duration strategies while investors with more than two years horizon may consider actively managed high-quality short-term or corporate bond strategies.

Lastly, investors with more than three years of investment horizon may consider a staggered allocation towards roll-down strategies.

(Anurag Mittal is Deputy Head - Fixed Income at UTI AMC)

Disclaimer: The views and recommendations given in this article are those of the analyst. These do not represent the views of MintGenie.