While FSN E-Commerce Ventures (Nykaa) listed at a 78 percent premium from its issue price of ₹1,125, it has witnessed a massive decline since then. The stock has lost over 47 percent in 2022 year-to-date (YTD) and has tanked 57 percent from its record high of ₹2,574, hit on November 26, 2021, its listing date.

What to do with Nykaa? While HDFC Securities sees a 30% downside; HSBC expects an over 95% rise

TL;DR.

Nykaa has lost over 47 percent in 2022 year-to-date (YTD) and has tanked 57 percent from its record high of ₹2,574, hit on November 26, 2021, its listing date.

The stock has fallen below its issue price and is trading around 2 percent lower. Since its listing, it has given positive returns in just 2 months - March and April 2022. It jumped 31 percent in March and around 0.3 percent in April.

The stock has consistently declined each month since May 2022. It has shed nearly 35 percent between May and October. In January and February 2022 as well, the stock crashed by over 21 percent each month.

Just in November (so far), it is down over 2 percent followed by a 9 percent and 8.5 percent fall in October and September, respectively.

Brokerages seem to be divided on the outlook of the stocks. They have contradictory views, while HSBC expects a massive upside, HDFC Securities see the stock continuing to fall.

Nykaa stock price trend

Brokerage Calls

Recently, domestic brokerage house HDFC Securities initiated coverage on the stock with a 'sell' call. The brokerage has a target price of ₹800 for the scrip, indicating a further downside of 27,5 percent from its current market price of ₹1,104.

However, last week, global brokerage HSBC said that Nykaa is likely to cross ₹2,100 in the next 1 year as it sees Nykaa as the structural winner of large-scale beauty and personal care (BPC) and lifestyle opportunities.

The brokerage maintained a 'buy' call on the beauty products firm with a target price of ₹2,170, indicating a massive upside of 96.5 percent from the current market price of ₹1,105. However, this is lower than HSBC's previous target price for the scrip, which stood at ₹2,180.

According to HDFC, when a buzzword (platforms) emerges that affords (GOD)LY valuations, investors and businesses tend to tie themselves in a knot to claim a credible association of their business with the term. Hence, many online businesses are termed as platforms, but not all are.

In this recent note, the brokerage attempted to help investors understand where it believes Nykaa fits in. "In our view, Nykaa has the potential to be a hybrid, but as of now, it shares more characteristics with a busy, efficient, linear online pipeline than a platform," said the brokerage.

A platform’s capability to layer on new revenue streams at low incremental production costs aid its scaling process. This ability is absent in online pipeline businesses, noted HDFC. Nykaa clocked 50 percent CAGR over FY19-22; its EBITDA margin expanded 250 bps and it has a linear asset turn profile (from 2.7x to 1.9x over FY19-22)—all akin to an online pipeline, it explained.

"Nykaa is an efficient online business; its success in part is due to the absence of potent competitors (this is gradually changing). Ex-ad income, lack of non-linear monetization levers forces us to realign our valuation compass somewhere between a linear business and a pure platform," said the brokerage.

It expects Nykaa to clock 31 percent/49 percent/115 percent (overall: 35 percent) revenue CAGR for (beauty and personal care) BPC/fashion/other segments respectively over FY22-25. Annual Unique Transacting Customers (AUTC) will remain the anchor growth variable across segments, it added.

The EBITDA margin is expected to expand by 370 bps to 8 percent by FY25 as (1) BPC product margins improve from -1 percent to 5.6 percent, courtesy of higher private labels; (2) scale-led operating efficiencies; and (3) fashion losses ebb (building in a breakeven in FY26). RoE/RoCE is likely to more than fully recover by FY25 (built-in: 21/15 percent), it added.

However, HDFC listed out some positives too. As per the brokerage, in a very short time, Nykaa has become the go-to destination for beauty and personal care (BPC) and cosmetics retailing. Founded in 2012 by Mrs. Falguni Nayar, Nykaa successfully addressed two bottlenecks: (1) product authenticity issues via its inventory-led model in a category (BPC) historically plagued with counterfeit products; (2) accessibility issues at both ends (brands and consumers) through broadening of distribution pipe (via its predominant online business model), it noted. Further, Nykaa's online content-led BPC product discovery certainly aided category building (especially within the more active Genz & Millennial set), in turn aiding its scorching growth, added the brokerage.

However, it pointed out that while Nykaa Fashion is a marketplace, it is still a budding segment targeting a premium customer base. Its right-to-win is not yet established.

In a contrarian view

According to HSBC, the stock has corrected partly due to the global tech sell-off on rising yields and more recently due to the imminent lock-in expiry (10 Nov). The brokerage believes the valuation is now even more appealing and under-appreciates the structural growth opportunity in beauty and personal care.

It further believes BPC and e-commerce are the perfect match and expects a 30 percent CAGR for the BPC e-commerce market in the coming decade, followed by a subsequent decade of double-digit growth.

Also, Nykaa with its leading scale, reach and broad product range is a rare combination of profitability and sustainable exponential growth, said the brokerage. It sees the firm's revenue doubling every 2-3 years in the coming decade.

In the September quarter, Nykaa posted a 344 percent year-on-year (YoY) jump in its September quarter net profit at ₹5.2 crore vs ₹1 crore in the year-ago period. Meanwhile, its quarterly revenue from operations recorded a 39 percent YoY increase to ₹1,230.8 crore from ₹885 crore in Q2FY22.

"During the quarter, we continued to demonstrate strong GMV growth with improvement in gross margin, efficiency in fulfillment and marketing cost lead to improvement in EBITDA margin YoY," Nykaa said in an exchange filing.

Its EBITDA improved to ₹61 crore vs ₹28.8 crore in the year-ago period while the EBITDA margin improved to 5 percent vs 3.3 percent in Q2 FY22.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

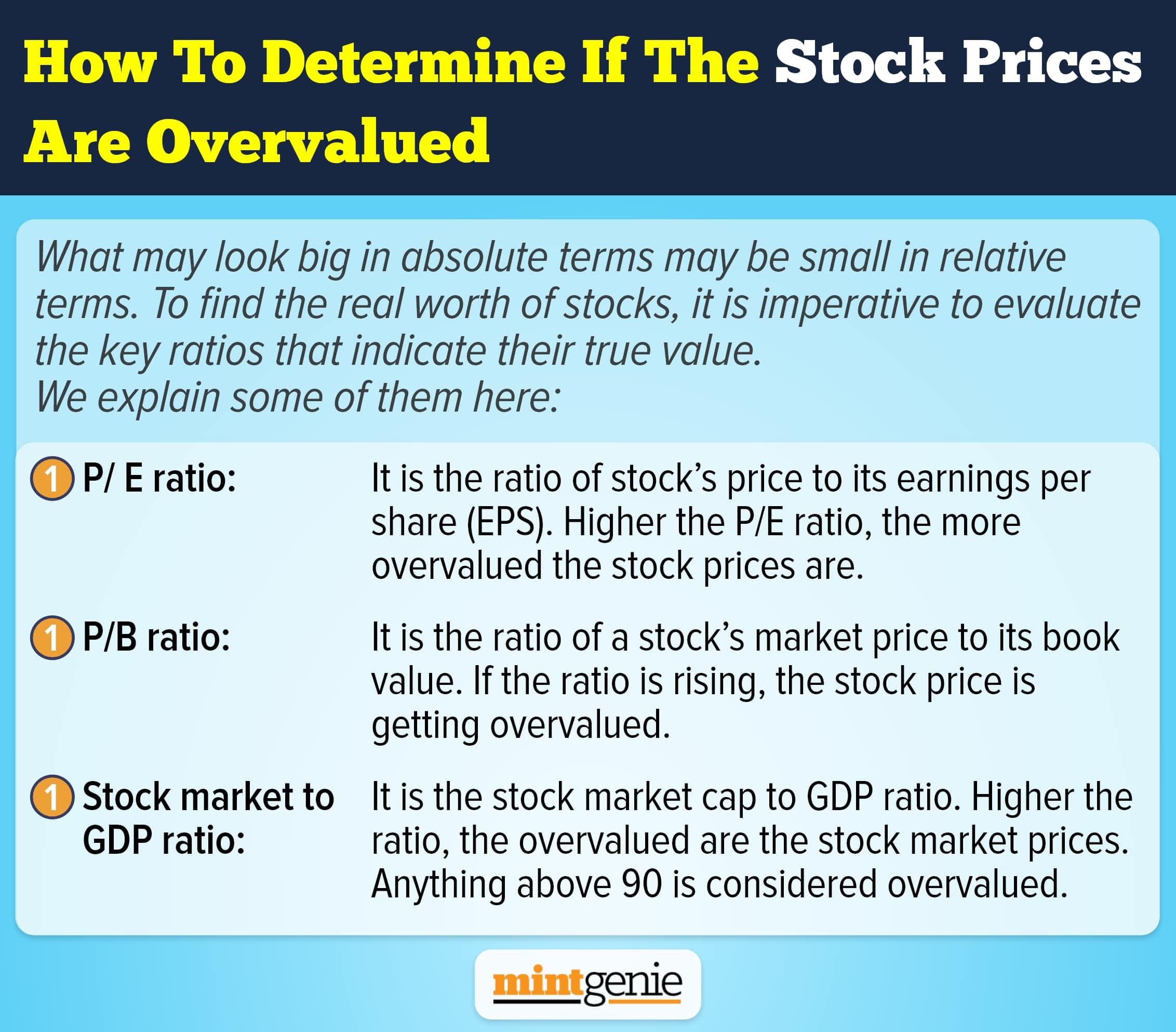

How to determine if the stock prices are overvalued.

First Published: 09 Nov 2022, 09:20 AM IST