Zomato was in focus on Monday after Q4 earnings showed the company's net loss narrowed further, adjusted Ebitda (earnings before interest, taxes, depreciation, and amortization) turned positive and revenue surged in the quarter ended March 2023. On the back of strong results, brokerages also retained their positive outlook on the food delivery aggregator.

On Friday, the company reported a trimming of losses at ₹188.20 crore for the quarter under review as against ₹346.60 crore in the December quarter and ₹359.70 crore in the year-ago period. Meanwhile, its revenue also surged 70 percent to ₹2,056 crore in Q4FY23 versus ₹1,211.80 crore in the corresponding quarter last year.

The company said that its business, excluding quick commerce, turned positive adjusted Ebitda, in the March quarter, further adding that it is aiming to be positive adjusted Ebitda (and also PAT) including quick commerce within the next four quarters.

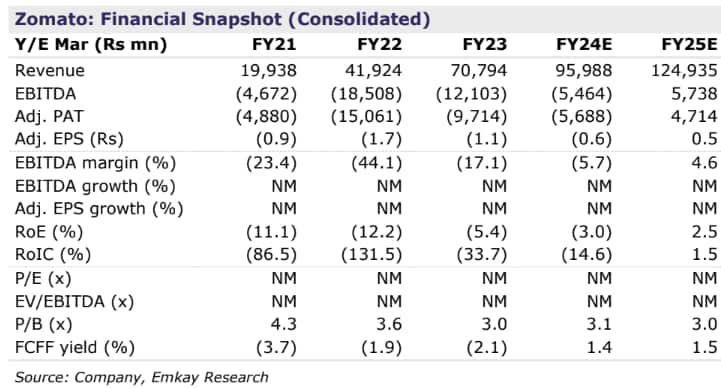

Overall in the financial year FY23, Zomato’s loss narrowed to ₹971 crore from ₹1,209 crore in FY22 and its revenue rose 69 percent to ₹7,079 crore.

The company further informed that the gross order value (GOV) in the food delivery business increased 12 percent to ₹6,569 crore from ₹5,853 crore a year ago, but dipped from ₹6,680 crore a quarter ago.

"In food delivery, over the last five quarters, we have improved our margins meaningfully while further strengthening our market position. We will continue with the same mindset as we look to further expand the adjusted Ebitda margin (from the current 1.2 percent) to our stated goal of 4-5 percent of GOV (which would translate to ₹1,000 to ₹1,300 crore of annual cash operating profit at the current scale of the food delivery business)," said Deepinder Goyal, MD and CEO of Zomato.

“We believe we are the most cost-efficient and the largest quick commerce business in India today,” Goyal claimed.

However, he also pointed out that Zomato's quarterly growth in the food delivery segment was low because of the demand slowdown that it witnessed from late October till the end of January this year.

But now, Goyal added that Zomato has started seeing green shoots of recovery in the first week of February and that recovery has continued and the business has grown well since then and the same should reflect in better GOV growth in the next quarter.

"We are expecting QoQ GOV growth to be in the high single digits in Q1FY24. This could have been higher if not for the industry-wide slowdown that continues to weigh on growth," Goyal added.

In March, Zomato's oldest city Bangalore turned profitable (before allocating central corporate overheads) whereas it shut down one of its cities (Chandigarh) as it did not see the right demand density in that location.

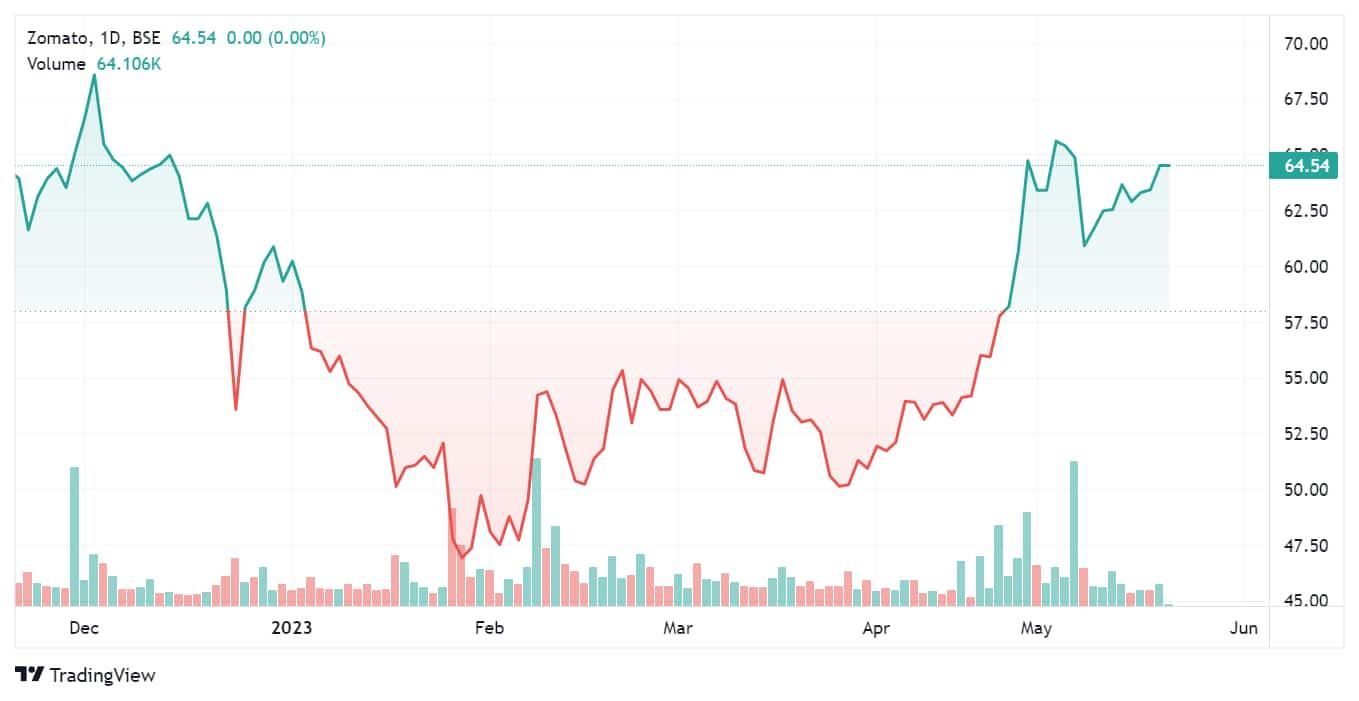

Stock price trend

Post the March quarter results, the stock jumped 3.5 percent to its day's high of ₹66.85.

The stock is up 11 percent in the last 1 year and 12 percent in 2023 YTD. In May so far, the stock is up over 2 percent after a 27 percent rise in April. However, it fell 4.6 percent in March. Meanwhile, the stock rose 7.5 percent in Feb but fell 16 percent in Jan.

The stock hit its 52-week high of ₹79.80 on June 1, 2022, and a 52-week low of ₹40.55 on July 27, 2022. It is now 16 percent away from its 52-week high and has rallied 65 percent from its 52-week low.

Brokerage views

JM Financial: The brokerage has a ‘buy’ call on the stock with a target price of ₹105, indicating an upside of 63 percent.

"Zomato’s core business (ex-Blinkit) turned adj. EBITDA positive in Q4FY23, at the front end of management’s guidance of achieving it by Q2FY24. The cherry on the cake was its commitment to turn both adj. EBITDA and PAT positive on a consol. level (including Blinkit) by Q4FY24. The core business milestone was achieved mainly on the back of solid expansion in the Food Delivery contribution margin to 5.8 percent vs. 5.1 percent in 3Q. This was because profitability levers such as improvement in restaurant commissions and ad income, and lower discounts/variable costs offset the adverse impact of the Gold launch. However, as anticipated, growth concerns in the food delivery business continued, with GOV shrinking 1.7 percent QoQ, albeit lower than JMFe of -4 percent. The decline was due to lower order volume. On a positive note, the company has guided for high-single-digit sequential growth for the business in Q1FY24," said the brokerage.

It believes continuity in these trends along with management commitment to profitability improvement can lead to a significant upside from CMP. Zomato is JM's top pick in the listed internet space.

Emkay: The brokerage also has a ‘buy’ call on the stock with a target price of ₹90, indicating an upside of around 40 percent. Zomato reported better-than-expected operating performance in Q4 – while it registered muted GOV growth QoQ, contribution margin across segments beat estimates, said Emkay. It further noted that the management expects sequential GOV growth to be in a high single digit in Q1FY24, on the back of green shoots of recovery since Feb-23 and guides for positive adjusted EBITDA and PAT on a consolidated basis within the next four quarters, and plans to achieve this driven by profit growth in the food delivery business and a loss reduction in Blinkit.

The superior Q4 performance bolstered Emkay's belief in Zomato’s ability to execute & deliver profitable growth. Further, an improvement in consumer sentiment is expected to drive GOV/MTU growth, it added.

Motilal Oswal: The brokerage has retained a ‘buy’ call on the stock with a target price of ₹80, indicating an upside of 24 percent. MOSL remains positive on the long-term growth opportunity for Zomato and does not expect competition to intensify further despite the entry of ONDC in the space.

The food delivery business is still at a nascent stage in India with a long runway for growth. With dominant market share and strong growth in the food delivery business and Hyperpure, it expects Zomato to report a strong 36 percent revenue CAGR over FY23-25. It further sees Zomato breaking even in Q4FY24, in line with the management guidance.