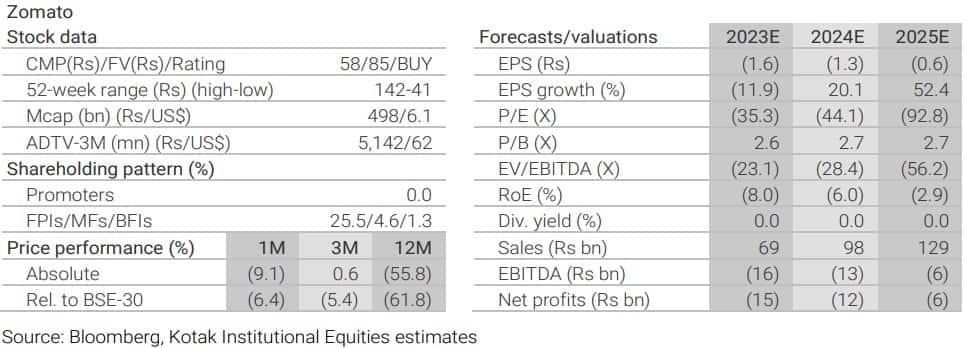

Kotak Institutional Equities (Kotak Securities) has maintained a 'buy' call on Zomato but cut the target price to ₹85 from ₹100 earlier. It said food delivery GMV (gross merchandise value) growth may remain subdued in the near term owing to weak demand.

The brokerage firm remains positive on the food delivery player due to its market share position in a duopolistic market and believes the Indian delivery market has legs to grow despite a near-term slowdown.

"Lower growth forecasts drive a revised DCF-based fair value of ₹85 ( ₹100 earlier). Zomato is our preferred pick among internet stocks, given the duopolistic market structure and large market potential," said the broking firm.

Zomato stock has seen a sharp fall in 2022. It is down 58 percent in the year as of December 26 close.

After posting 35 percent year-on-year (YoY) food delivery GMV growth in the first half of the current financial year (1HFY23), Kotak expects Zomato’s food delivery growth to decelerate to 21 percent YoY in the second half of the year (2HFY23).

Although AOVs (average order values) are likely to hold up due to inflation and relatively higher delivery charges, Kotak said slower growth in orders will lead to slower GMV growth. This, in turn, is owing to weak consumer demand in what otherwise is a seasonally strong quarter for outdoor food consumption.

"We reckon the weakness is pan-India, with a slowdown in demand in metro and non-metro geographies. The fact that restaurant chains are also witnessing a slowdown indicates the slowdown is across channels and delivery is not necessarily losing share to in-store dining," said Kotak.

Kotak highlighted that post-Covid quarterly earnings reports of global food delivery companies suggest that GMV growth has come off meaningfully in the calendar year 2022 (CY2022), as Covid-induced demand receded. In comparison, Zomato’s growth trajectory has still been much better, given the relatively underpenetrated Indian market, and the convenience and variety offered by Indian delivery companies.

"We bake in slower food delivery GMV growth forecasts of 26/24/22 percent over FY2023/24/25 versus 32/30/30 percent earlier. We revise our CM (contribution margins) assumptions upward to 4.3/4.5/4.9 percent from 4/4.2/4.6 percent of GMV, but continue to be substantially below Zomato’s mid-term guidance of 8 percent CM," said Kotak.

According to a MintGenie poll, an average of 23 analysts have a ‘buy’ call on the stock.

Disclaimer: The views and recommendations given in this article are those of the broking firm. These do not represent the views of MintGenie.