With the COVID-19 changing how we work, where we work from, and how we take care of ourselves, the pandemic also saw the rise of freelancers and gig workers as many companies laid off employees, cut down on budgets, etc.

ASSOCHAM predicts that India’s gig economy is expected to grow to $455 billion by 2024 at a CAGR of 17%, with the potential to grow at least double the pre-estimates for the post-Covid-19 period. A person who performs work outside of a traditional employer-employee relationship, is usually termed as a gig worker, with the gig usually lasting for a specified period of time.

For instance, freelancers, delivery people, consultants, cleaners, bloggers, project-based workers and temporary or part-time hires. By 2025, India is likely to have 315 million gig worker jobs. As per Niti Ayog report on ‘India’s Booming Gig and Platform Economy estimates that gig workers will form 4.1 per cent of the total workforce in India by FY30, from 1.5 per cent now. Many organizations in fact, are also now keener on getting specialist gig workers in their fold rather than investing in a full-time employee.

The Need

Gig workers, by nature of their work, are vulnerable to fluctuation in demand and are not covered by standard employee contracts.

With the rising inflation, and steady drop in the take-home salary, most gig workers and freelancers are ignoring, or are too cash-strapped, to invest in a suitable health and life insurance. But is this right?

Financially-strapped solo earners like construction workers, delivery agents, etc with their low-skill level and high dependency for household income, look for key job choice drivers such as good salary (even if for limited time) and regularity or continuity of job. They also seek non-monetary benefits like health insurance to save money in the long term, notes BCG in its report ‘Unlocking the Potential of the Gig Economy in India’.

Being your own boss is definitely a perk that most of us will happily jump at, but without the safety net of regular income, corporate group medical insurance, PF, gratuity, etc, it becomes important to think about and manage one’s financial needs and uncertainties.

Moreover, gig workers and freelancers - often paid by the hour or assignment - do not have the option of taking a sick leave for the fear of losing wages, and continue to work till their health situation gets really bad. There is financial insecurity since it’s common to have irregular cash flow.

Therefore, an investment in corporate wellness programme and employee benefits offerings such as corporate fitness programmes, mental wellnesss, to avoid medical costs for gig workers and freelancers can be very crucial to ensure continuity of gigworkers. Wellness programmes will not only improve morale and loyalty, increase productivity by reducing stress, help them reach milestones, increase happiness with their work, but also reduce chronic diseases and the risks of health problems by encouraging a culture of exercise and healthy eating.

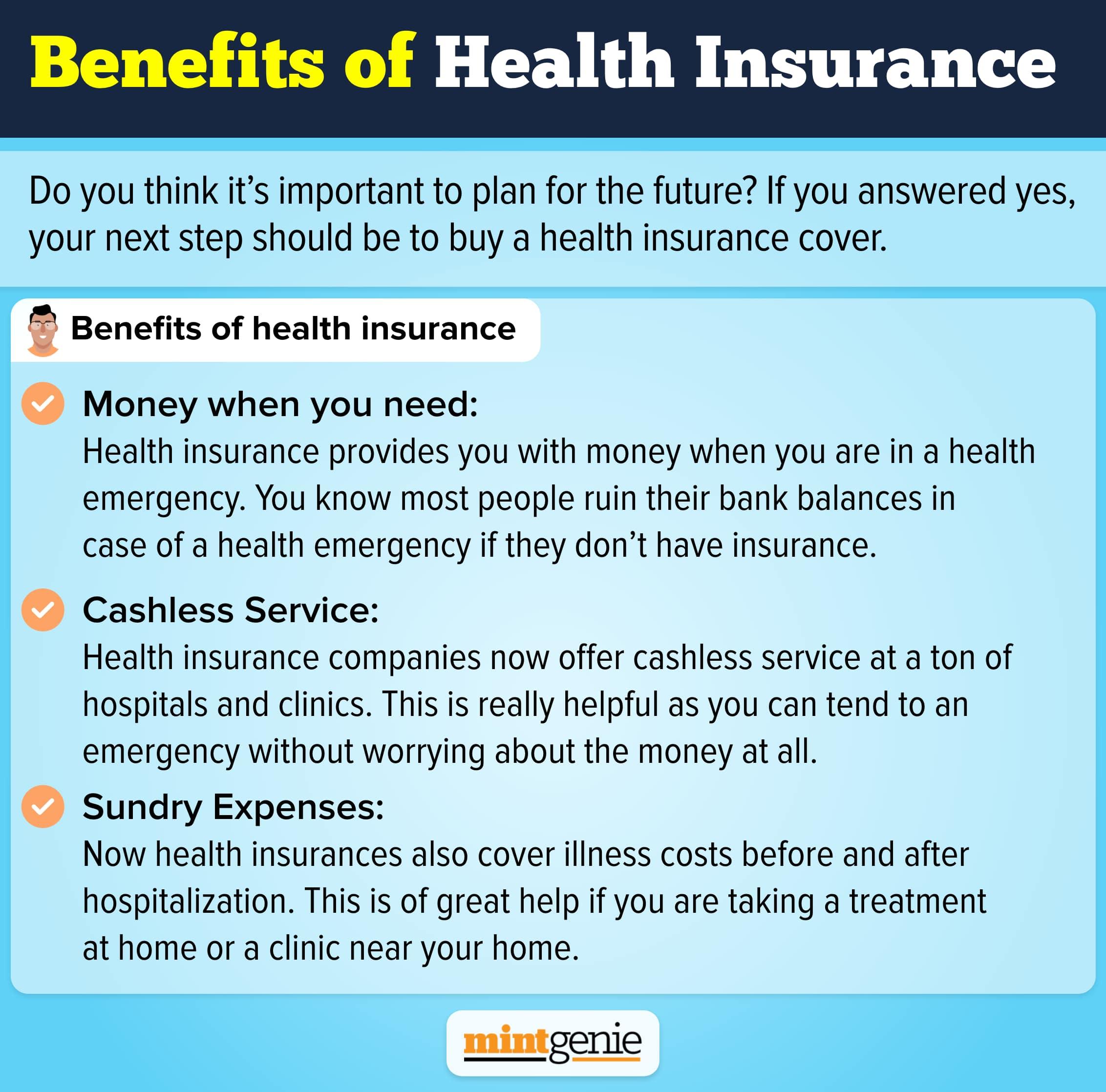

How does health and life insurance help gig workers and freelancers?

Financial security

Irregular income, more so, for freelancers and gig-workers, translates to financial insecurity. It hence, becomes more important for them to safeguard against financial emergencies related to health and life, especially when the work might bring different set of risks. Health insurance for instance, provides a safety net in case of an undue illness or health hazards leading to diseases and costly medical treatments. In absence of regular assignments or gigs, at least the medical expenses for self or dependents - which usually do eat up most of the savings - are taken care of by the insurance.

Workplace injury

In India, where delivery under 20-minutes is gaining prominence, workplace injury cannot be ruled out. In the absence of stipulated contractual agreement between the organization and the gig worker, the risks lie solely on the shoulders of the worker, and not the employer unlike the traditional workplace scenario. Since most gig workers use their own equipment, vehicles and work space, it is important that all these elements including the self are insured in case of fire, theft, or accidents. In absence of corporate protection for a person’s life and health, insurance becomes a bare necessity.

BCG notes that workplace hazard coverage for workers in construction and manufacturing industries will be important to ensure similar levels of coverage as traditional employees.

Human life value

Life insurance is typically attached to the human life value index, which is the present value of all the future income that the gigworker could expect to earn for their family. An ideal limit is arrived at by considering the financial value of the life of a gigworker– the value that one might bring to one’s family and dependents in the foreseeable future.

Therefore, it is not only important for a person to start investing in a health and life insurance plan before or as soon as they decide to become a full-time freelancer or enjoy various gigs, but also critically analyze this amount from time to time.

The way forward

The easiest way to evaluate the health and life insurance coverage would be to calculate (approximately) the yearly earning, yearly medical expenses on self and dependents, anticipated expenses such paying off a mortgage and inflation in the city/country that the freelancer or the gig-worker stays in. So, for instance, typically a gig worker in delivery and logistic segment will earn aprrox ₹30K per month. Hence, they should at least have a life insurance cover of ₹30 - 50 Lakhs and the health insurance of ₹3 lakhs for their family. For consultants, typically their monthly earning is ₹1 Lakh. So, their term life insurance should be ₹1 Crore and health insurance of ₹10 Lakhs.

Freelancers and gig workers are increasingly understating the need of investing in insurance, given the rising medical inflation, job-associated risks, pandemic, etc. While gig work is here to stay, by establishing insurance as a social security tool, India will be abundantly prepared to unlock the sector’s prospects in the times to come.

Yogesh Agarwal is the Founder and CEO at Onsurity