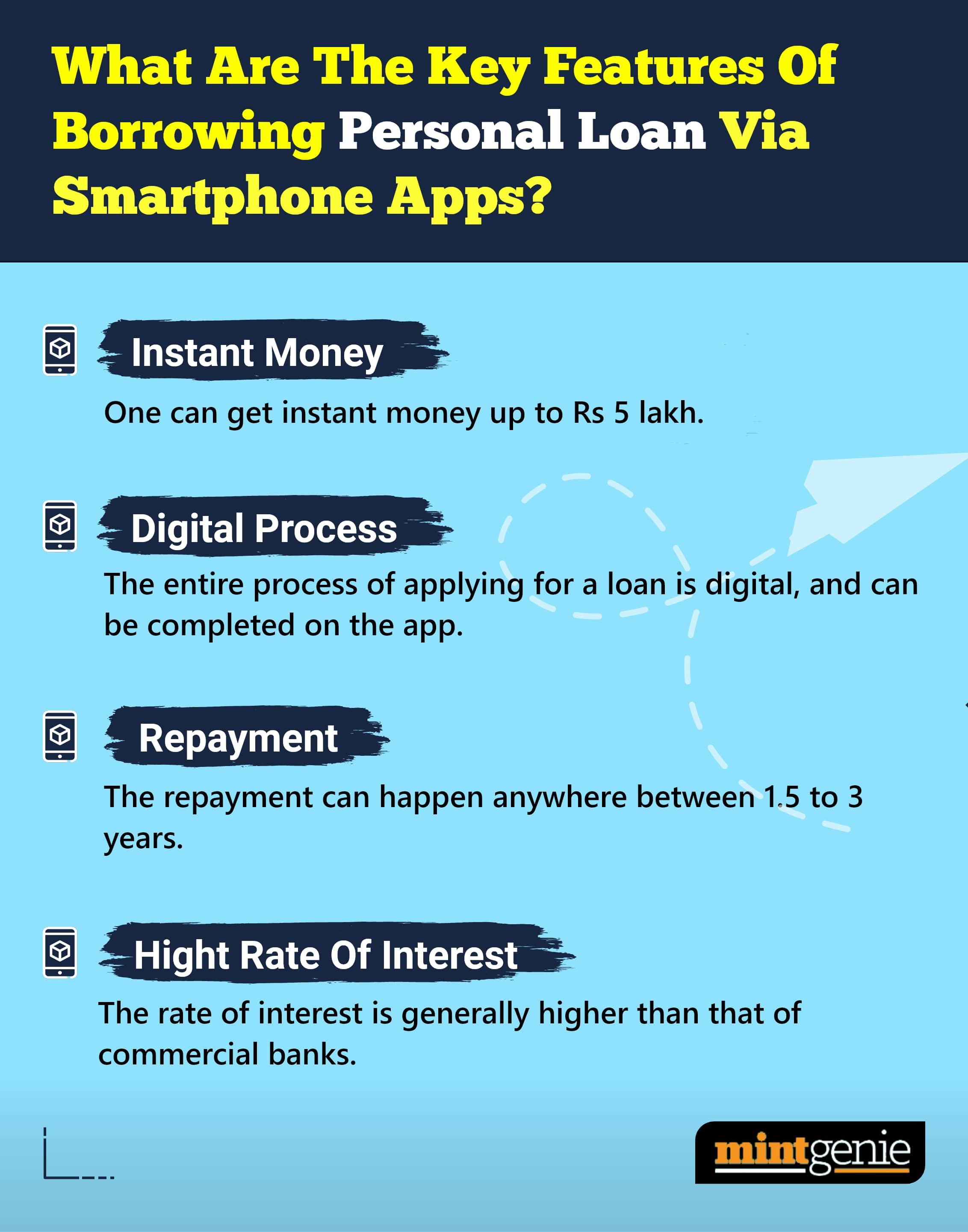

There is no dearth of people seeking loans to either meet financial needs or buy assets. Some people also take loans to reduce debt, pay for current expenses or to invest in options with the potential to earn income in future. There are myriad types of loans including home loans, vehicle loans, credit card loans, etc. Irrespective of the reasonable interest rates that banks and financial institutions now charge, one must not ignore the fact that any kind of loan equates to debt that must be repaid someday or the other.

It feels good to be able to close your loan. Closing, especially foreclosing your loan, means that you are ridding yourself of unwanted debt. Also, you are relieving yourself of the hassle of having to pay the interest along with the principal component, which leaves you debt-free in the end. Being able to foreclose your loan enhances your credit score and saves you from future inconveniences. However, the joy of being completely debt-free must not override your tendency to miss out on essential details that may lead to unwarranted legal issues in the future.

Keep the following facts while closing your loan to shield yourself from sudden unforeseen trouble. These include:

- If you are foreclosing on your loan, you must inform your bank representative and check for any unpaid levies or penalties. Many banks charge between one and five per cent of the outstanding loan balance. Also, when you have paid that, check if you have submitted all necessary documents supporting your loan repayment and whether the bank has returned you all the documents in compliance with the loan agreement.

- Many banks and financial institutions doling out home and vehicle loans put a lien on the collateral to avoid losses from bad loans. Not many know that a lien is the legal right of the banker (or any creditor) to sell the collateral property of the borrower in the event of non-repayment of the loan amount. It would be wise for the borrower to visit the banker’s office and get the lien removed. The credit then issues a No Objection Certificate (NOC), which means that the debtor has cleared all dues and need not pay anything more. Also, the creditor now has no right over the property or collateral.

- In the case of a home loan, borrowers are complacent with receiving back the documents of their respective properties. However, they must seek a detailed statement of all the transactions related to the property called the Non-Encumbrance Certificate to ensure zero liabilities from the borrowers’ and creditors’ end in future.

- Taking a loan affects your credit score. Repaying it on time or prepaying the loan amount reflects on your credit score, thus, making you more eligible for another loan in future. The borrower must ask the bank to update the CIBIL score on the site. Though this takes time, borrowers must pursue in this direction to avoid difficulties while borrowing in future.

Taking a loan means incurring debt and inviting the possibility of losing your asset (kept as collateral) to the creditor. That is why borrowers must ensure that all documents are in place and that no part of the entire loan process must be left incomplete or at the mercy of the creditor. Post repayment of the loan, borrowers must take care that the creditors (banks or non-banking financial companies) have any right to the collateral submitted by the collateral.