In all fairness, we all find ourselves trapped in a situation someday that makes us realize the futility of not having planned well in advance. But then, irrespective of how prepared we may think of ourselves to be, the unprecedented Covid-19 pandemic in 2020 and the subsequent crisis sent us reeling into disbelief and scepticism.

More than the disease, it is the financial inadequacy to pay for treatment that took millions of lives. Unplanned business shutdowns and consequent loss of jobs destroyed livelihoods and pushed many on the verge of seeking unwanted debt. Many people could not cope with the prolonged financial distress synonymous with emergency situations.

In situations like these, one can only hope to lie down low and let the circumstances pass without causing too much damage. However, looking at the same in hindsight, it is a clear revelation of the imperative need to be financially prepared to deal with all emergencies, unbiased of their roots and timing.

The key learning that we all took is the need to be financially secure at all times. This we can do by being aware of our earnings, savings, investments and most importantly how much we set aside to meet exigencies. Ensuring financial security has more to do with smart saving and effective risk management strategies than focusing on continued earnings. To start with, you must plan to

Build a corpus for emergencies

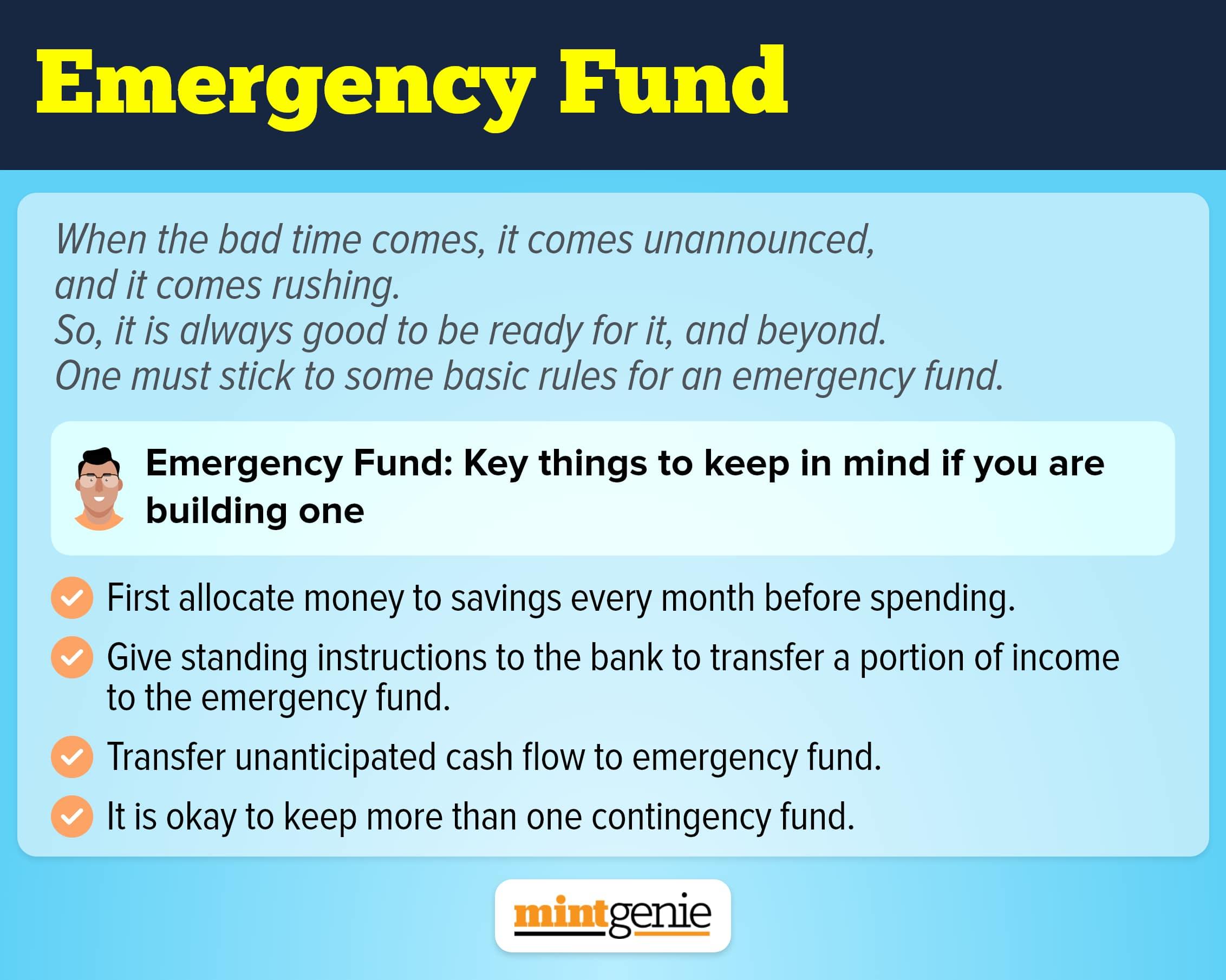

There is no point in having lots of investments that cannot be liquidated as and when required. This pushes us to the understanding of planning an emergency corpus consisting of liquid funds and enough cash to help mitigate the crisis and pay toward unexpected situations without having to break down our investments or draw on unnecessary debt.

How much money we must secure in our reserve funds depends a lot on our lifestyle habits, necessary expenses and loans that we must repay. The rule of thumb says that you must secure an amount equivalent to three to six months of your monthly expenses that also include fixed expenses including rent, school fees, daily utilities, essential bills on electricity, water, gas connections, medicines and travel apart from the equated monthly instalments that get deducted from your accounts toward your loans and liabilities. To ensure a greater safety net for your family, you may extend the reserve amount worth a year of your expenses.

Not all money reserved in the emergency fund must be kept in cash. Instead, opt for a decent 10:20:70 allocation towards your fund. This means that you must allocate 10 per cent of your reserves in cash, 20 per cent of the money in bank deposits for quick remittances with the remaining 70 per cent parked in low-risk options like liquid funds and other money market instruments. You may tweak your fund allocation depending on your needs; the idea must have enough to use as and when you need it.

Buy enough insurance

You may have been one of the lucky ones to escape the brunt of hospitalization and subsequent treatment when most people around you were paying hefty bills to get treated for Covid-19 and related complications. However, many had to dig into their lifelong savings just to pay hospital bills that ran into lakhs of rupees. Still, others lost their loved ones to the disease that is said to have snuffed out the lives of millions of people around the globe. The epidemic has left most families feeling defeated. The effect has been largely on people living on a sporadic income source.

More importantly, we all have our families that must be taken care of. Rising costs of living coupled with increased medical costs have put back the focus on the need to have adequate finances to ensure our overall well-being. This also explains why including health and life insurance plans in our financial portfolio is a must. Care and protection for our loved ones must take precedence over everything, which is why buying insurance is the perfect antidote to tackle tomorrow’s insecurity. Opt for a comprehensive health insurance plan or a family floater policy with adequate cover to pay for sudden hospitalization and unforeseen medical exigencies. Revise your health insurance from time to time. Load up your top-up plans and tick on the add-on riders to insure the health of your loved ones. This might seem like added costs owing to the extra premium payment but will do you much good in the long run.

A life insurance policy takes care of a family’s daily and long-term expenses in the face of an unfortunate event like the demise of its breadwinner. Also, good insurance coverage goes a long way in helping the nominees unload off the burden of debt and loans if any. Though you can ensure that the term insurance cover is at least 10-12 times your yearly income, you must account for the rise in prices owing to inflation.

Effective debt management

It is nothing short of a blessing to be completely free of debt. However, if you have an overriding loan that eats into your monthly earnings, take care to get rid of it soon. You could chalk out a repayment plan that allows you to be free of debt, thus, saving you from the burden of destroying your savings and jeopardizing your future goals. Take only those loans that you can repay with what you earn and refrain from living your life on credit. Limiting your expenses will leave you with more money to prepay your loans, especially, those charging high-interest rates.

Maximizing savings

The conventional method of saving money to invest before you spend may seem cliché but is worthwhile even in today’s times. How much you save or are willing to spend has a considerable bearing on your financial future. You can use the money to save to build a contingency fund or prepay your loans to get rid of them early or invest in some fixed-income plans that would come in handy to tackle sudden financial downturns in the near or distant future.