As an Indian, we trust people so easily that we are habitual of reading papers before signing it. Just because someone says, “don’t you trust me”. Well you realise the mistake soon when you have to go through the consequences. Well, it doesn’t happen because of our trusting habits, it happens because of our lack of awareness about the consequences that we could face at the time of our need.

In this article, we will understand the importance of reading papers before signing it from the perspective of your health insurance claim.

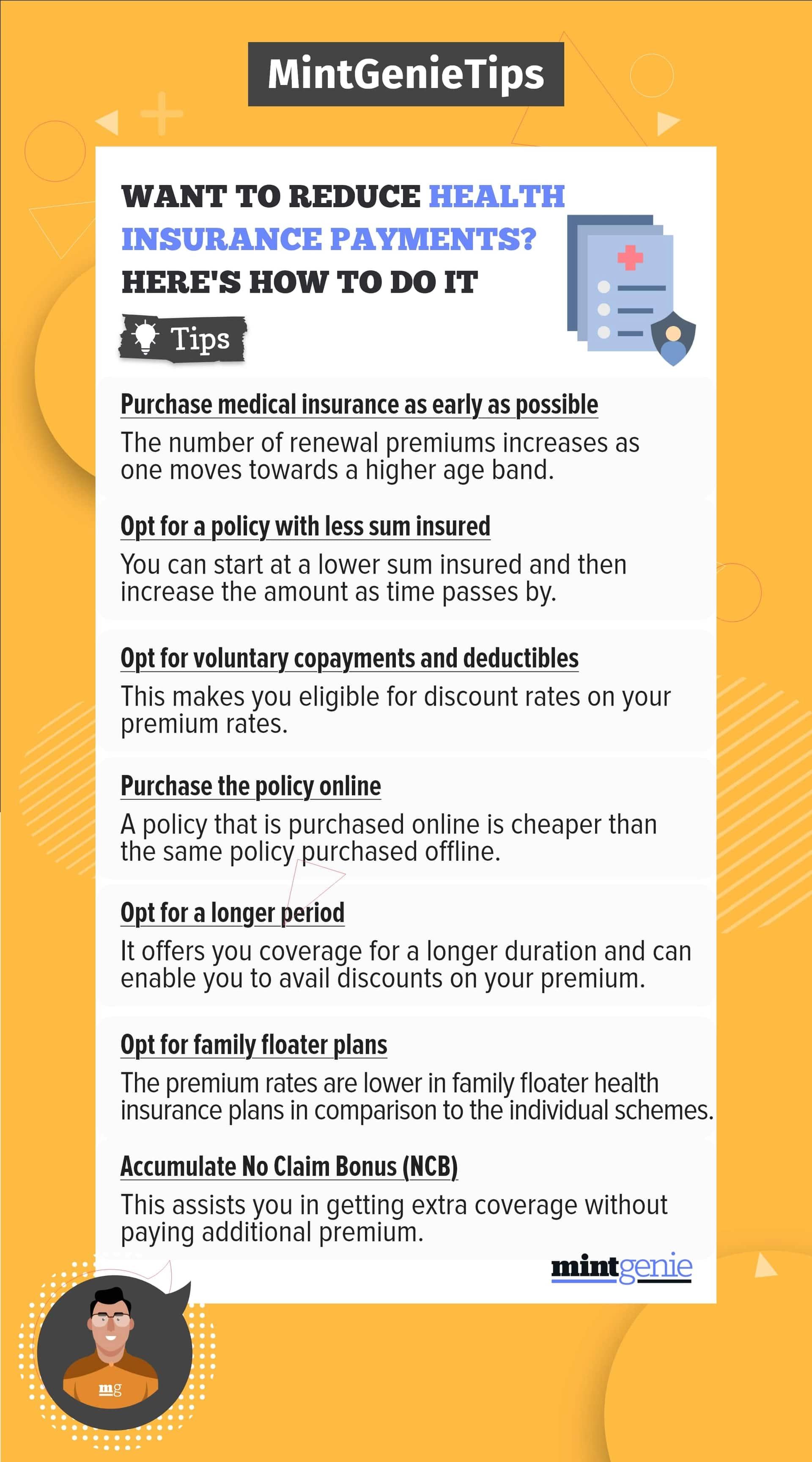

READ MORE: Medical Insurance: This is how delays in approving claims can be avoided

Non-disclosure of the existing disease

At the time of buying a health insurance policy, you need to disclose your pre-existing diseases to the insurance company as it is a part of the mandatory field. Additionally, there is a waiting period given by the insurance company for the expenses incurred due to pre-existing diseases. Suppose your waiting period is 3 years and you get hospitalised due to your existing disease only after 1.5 year of buying the health insurance policy, you will not be able to get a claim as your waiting period is not over yet.

Falling into the exclusions

Every insurance company has some terms, conditions, and exclusion clauses. Falling into the category of exclusions and not following the terms and conditions of insurance policy might cost you the whole amount of insurance claim. The majority of health insurance plans do not offer coverage for a number of conditions. These are clearly listed as "not covered" in the policies. These are essentially the diseases for which you cannot submit a claim.

READ MORE: 9 things to consider before filing a health insurance claim

Crossing the limit of sum assured

In any case, you will not receive the amount more than you have assured. If your medical claim exceeds the limit, you will only receive the amount up to the assured sum. Always keep a track of your diseases and expected inflation rate of healthcare expenses prevailing in your country. For instance, if your sum assured in your policy is ₹10 lakhs, and your medical expenses goes to ₹17 lakhs. You will only be able to receive claims up to ₹10 lakhs.

Non-renewal of your policy

It is the most important aspect of your health insurance, which could be ignored and cost you the whole healthcare expenses plus premiums. Typically, health insurance coverage is in effect for a year. The insurance will become void after a year. An out-of-date health insurance coverage serves no purpose for the insured. As a result, you must renew the policy. There will be further advantages to renewal.

READ MORE: Know the essential tips to ensure seamless claim settlement of your insurance policy

For instance, if your policy expires in March 2022, and You have not renewed your health insurance policy after the expiry of your policy. You got hospitalised in April, now, your insurance company will not give you the claim as you haven’t renewed the policy.

Financial security is the first and last thing you aim for when you buy any type of insurance policy. Make sure that you don’t waste an opportunity to achieve the target of financial security by not making the above-mentioned mistakes.

Anushka Trivedi is a freelance financial content writer. She can be reached at anushkatrivedi.com