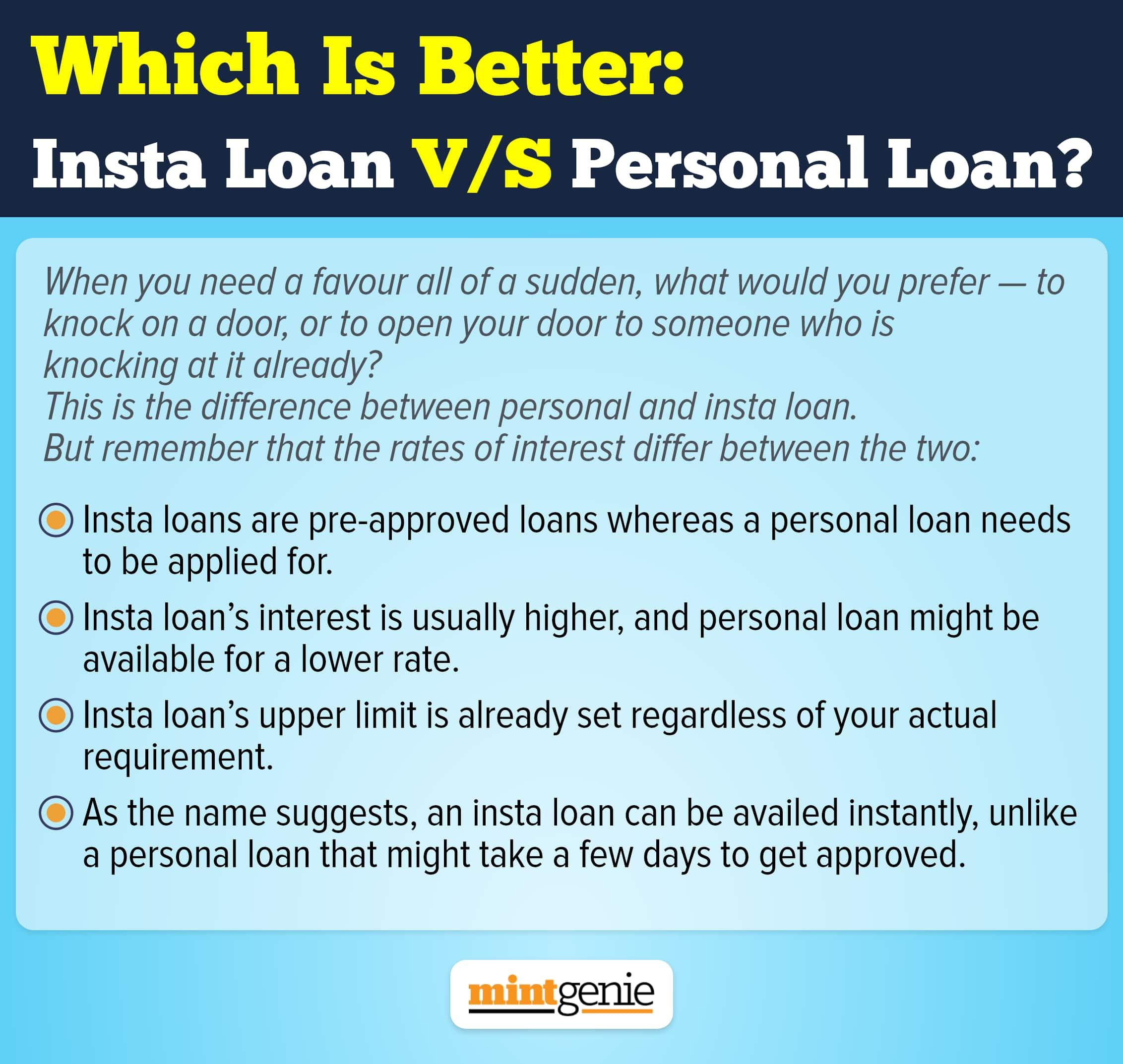

There is a high demand for personal loans lately. Details by CRIF High Mark, a credit rating agency, indicate the personal loans book size to the tune of ₹3.8 lakh crores. The loan book continued to grow consistently at 35 per cent on a year-to-year basis over the past two years. The number of personal loan accounts shot up four times from 39.9 lakh accounts in FY19 to 158.1 lakh accounts in FY22.

There may be myriad reasons for borrowers opting for personal loans. For example, there might be a sudden need for cash to be spent on travel, weddings, medical emergencies or to meet unforeseen business requirements. However, personal loans are not cheap. The interest rates on personal loans are considerably higher than others and went up recently after the repo rate hike by the Reserve Bank of India (RBI). Apart there are terms and conditions that borrowers dare not overlook to avoid risks of default.

Dealing with high-interest loans

With interest rates going up by 0.6 per cent on a three-year loan, it makes sense to adopt ways that would help tackle high interest on personal loans. The onus of high interest would be passed on to the borrowers, thus, forcing them to pay higher equated monthly instalments (EMIs) towards loan repayment. In the event of an inability to pay higher EMIs, borrowers tend to request a longer loan tenure. This, in turn, increases the total interest outgo on the loan amount.

For those who have recently taken the loan, it would make more sense if they assess their loan requirements to relieve themselves of the burden of higher loan repayment. This is also important to escape the risk of penalty in case of non-repayment of the loan and poor credit score.

The first step would be to replace your idea of seeking a personal loan with a secured loan to benefit from lower interest rates.

Loan against EPF amount: If you have an account with the Employee Provident Fund Organization (EPFO), you can always apply for a loan up to 90 per cent of the balance amount in the EPF account.

Loan against PPF balance: More than the relatively high-interest rate and tax-saving measure that your Public Provident Fund (PPF) offers, you can take a loan against your PPF balance. A loan applicant can seek a loan against the PPF in the year following which the account was opened, i.e., from the third financial year.

Pledging gold: Many investors buy gold as a hedge against inflation. However, not many know that the yellow metal can be pledged as collateral to get a loan. This is indeed a better option than opting for unsecured personal loans that charge high-interest rates at often unaffordable terms and conditions. Also, you do not need an exceptionally high credit score to seek a loan against gold.

Loan against FDs: Most conventional investors park their savings in fixed deposits. This fixed-income instrument though does not yield returns good enough to beat inflation is still a safe and sure-shot option to fall back in case of emergencies. Moreover, instead of rushing to banks or financial institutions to inquire about personal loans, loan applicants can simply opt for secured loans against fixed deposits. Lenders usually agree to give loans up to 90 per cent of the balance in your fixed deposits.

Loan against property: If you have a property that you can secure as collateral to get a loan, then why not go for it? More the value of the property, the higher would be your eligibility to opt for a greater loan amount. It is not difficult to secure a loan against property as lenders usually agree to give loans up to 80 per cent of the value of the property.

Loan against mutual funds: Mutual funds can be used to take a loan. Lenders agree to take up the purchased units pursuant to which they then offer the loan.

Loan against life insurance: A life insurance serves more than just securing your loved ones’ future. You can use your life insurance policy to secure a loan, though the interest rate charged on it may be considerably high to the tune of 10.5-12.5 per cent.