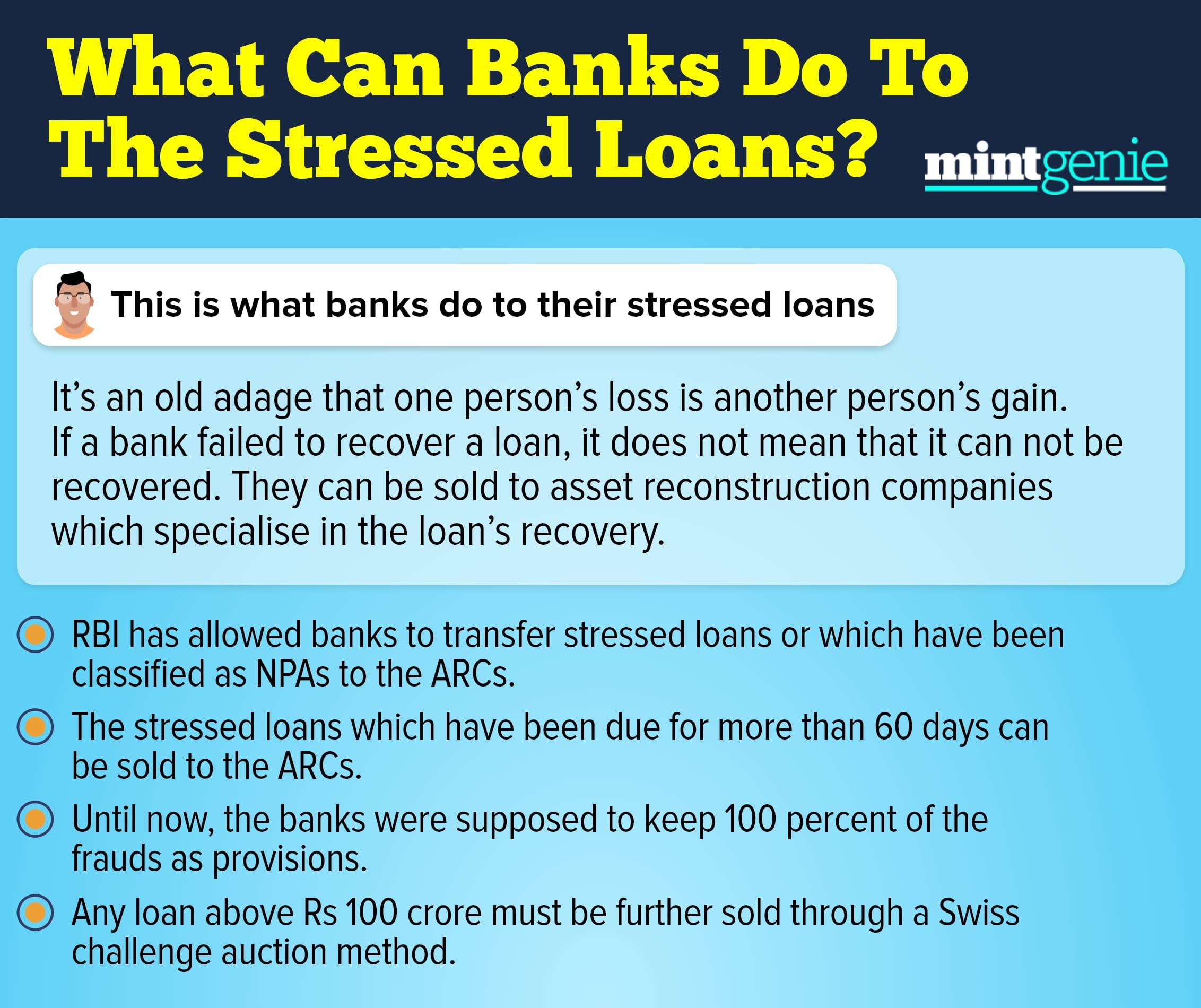

The Indian banking regulator Reserve Bank of India (RBI) has now allowed banks to transfer stressed loans or which have been classified as NPAs (non-performing assets) to the asset reconstruction companies.

The stressed loans which have been due for more than 60 days and the ones under the category of ‘frauds’ can be sold to the ARCs. The RBI issued guidelines for transfer of these loans from banks to these companies in September 2021.

Until now, the banks are supposed to keep 100 percent provision for loans which are categorised as frauds. This effectively means there was no hope of loan recovery. With the transfer of loans, there will be optimism of partial or complete recovery of loan.

The ARCs, at the same time, can buy cheaper debt than the regular loans.

The plan ahead

The RBI has drawn a set of guidelines that will govern transfer of loans. This will create more opportunities for raising liquidity. However, banks are supposed to keep loans for at least six months before they sell them further. The loans with less than two years of tenor must be held for a minimum of three months.

The RBI, in a master direction issued on September 24, 2021, said, “A robust secondary market in loans can be an important mechanism for management of credit exposures by lending institutions and also create additional avenues for raising liquidity. It is therefore necessary to lay down a comprehensive, self-contained set of regulatory guidelines governing transfer of loan exposures.”

Swiss challenge auction

Any loan above the threshold of ₹100 crore decided between buyers (ARCs) and lenders must be further sold through a Swiss challenge auction method. Under this method, the price at which the loan is sold is used as a floor price for further sale to any prospective buyers.

Swiss challenge auctions are popular in awarding government projects and in bankruptcy cases. In this, an interest party first begins a project. Later, the government then shares more details to invite more bids.

After receiving the counter bids, the original contractor is given an opportunity to match the new bid or else, they may back out to pave way for the other contractor who gave a better bid.

These new guidelines spell optimism for the banking industry as it gives them adequate elbow room to move on and not get dragged by their un serviced loans or frauds. As the loans stay outstanding for too long, they can sell them to those companies which specialise in the recovery of loans, and banks — meanwhile — can focus on their core business of banking.