A recently released study on banks in India states that BNPL (Buy now pay later) schemes are gaining healthy traction in the Indian market. The study also observes that BNPL has a lower share of new-to-credit customers. A typical BNPL customer is not very different from a consumer of other unsecured retail loans, states the study carried out by Kotak Institutional Equities Research.

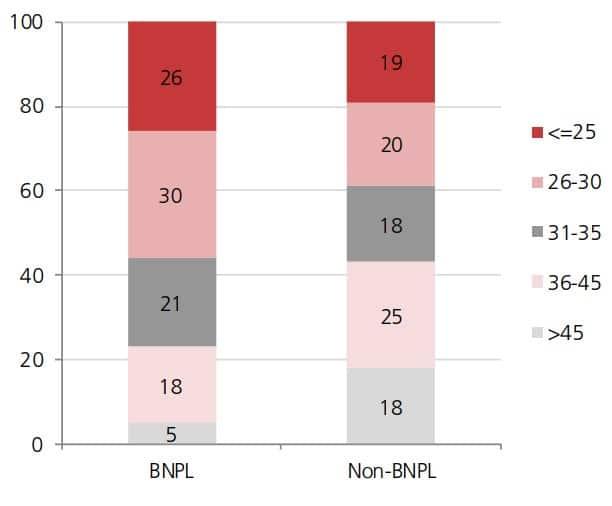

It’s interesting to note that BNPL customer has a strong affinity for other unsecured loans as well. The proportion of borrowers under the age of 25 stood at nearly 26 percent for BNPL and around 19 percent for non-BNPL which include credit cards, consumer durable loans and personal loans.

The business model around BNPL is still at an early stage of evolution and, perhaps, still not fully developed.

Not so different

A typical BNPL consumer, observes the study, is not significantly different from a typical consumer of other unsecured credit products on parameters such as age, risk tier or leverage. Average credit balance for a BNPL consumer (around ₹0.19 million) is very similar to that of a non-BNPL consumer. The proportion of new-to-credit consumers was also similar for BNPL and non-BNPL originations of unsecured consumer credit.

Despite these similarities at the time of origination, consumers who have a BNPL account show a higher delinquency performance on their credit card and personal loan accounts.

BNPL customers are skewed towards the younger age groups

No impact on credit card business

The study suggests that BNPL consumers are more likely (than non-BNPL consumers) to open a new credit card account within six months of BNPL loan origination. Also, the propensity to avail a personal loan also seems higher for BNPL consumers.

These data-points indicate that BNPL is serving as a gateway to credit cards for many consumers, while also giving credit card issuers more comfort on the borrower at the time of underwriting.

Lizzie Chapman, Co-founder & CEO, ZestMoney says, “All loans are sitting on NBFC or banks with full KYC and credit bureau reporting. 90% of BNPL in India is done like that. In rest of the world, a lot of pressure coming onto the space because unregulated and poor underwriting checks. In India, most BNPL products do full underwriting, KYC and bureau reporting and checking.”

About profitability, Chapman says that at scale, this business can be more profitable than credit cards because it has very low fixed and operating costs. “This gives huge massive operating leverage. You can get credit card like economics but 1.5X better return ratios,” says Chapman.

Laxmikant Vyas, Co-founder and CRO, Uni Cards says the apprehensions that used to exist among Indian consumers do not exist anymore. He also speaks about the availability of opportunity because of lower penetration and greater acceptability of credit cards.

“A lot of people would shy away from taking a product because it was difficult for them to consume because of monthly repayments and opacity of charges. People now understand credit cards better. That is reducing apprehensions. Number of cards per customer is also low in India, but from geography and customer segment perspective, there is opportunity everywhere. Under-penetration exists even in urban and metro areas,” says Laxmikant Vyas, Co-founder and CRO, Uni Cards.