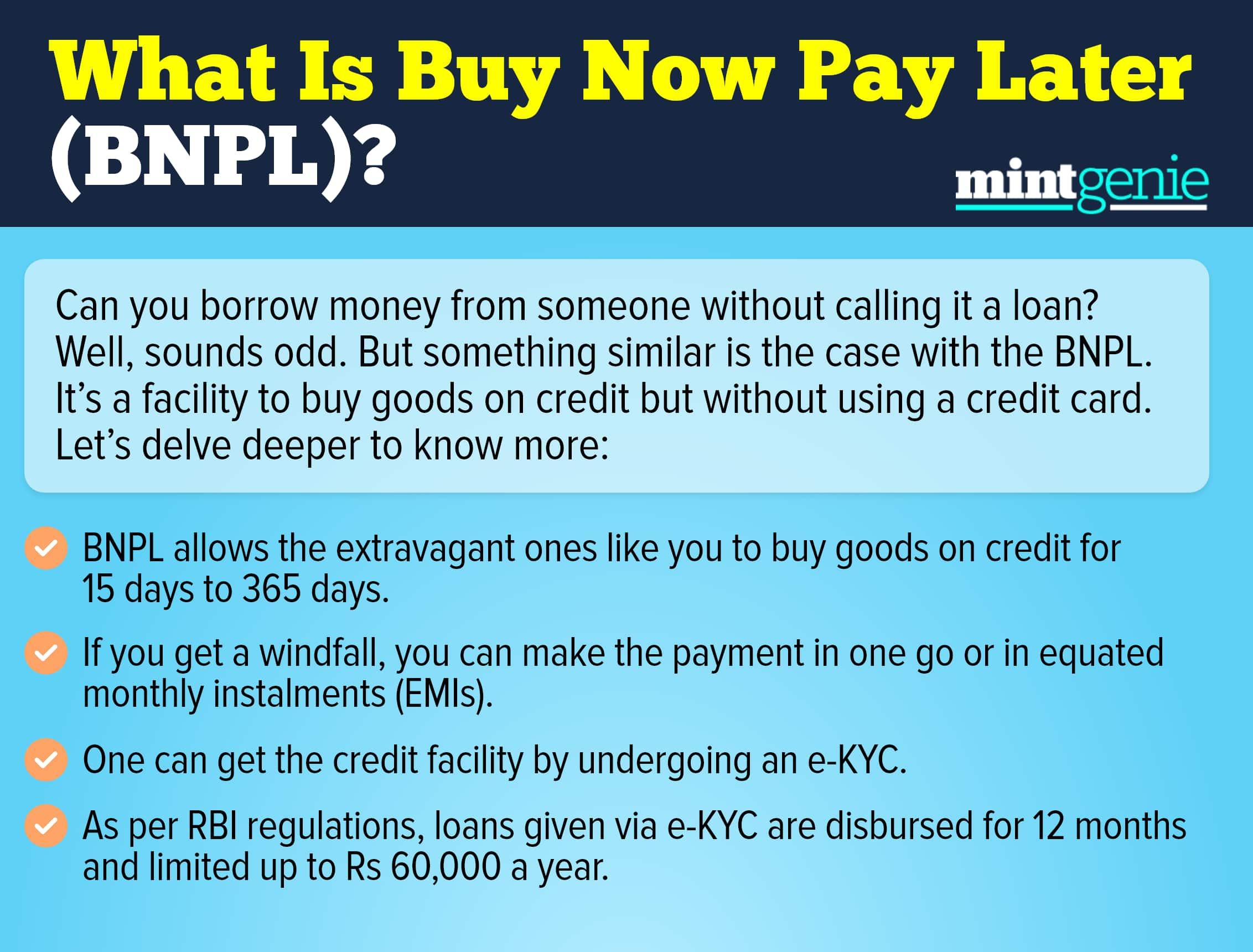

As a youngster, you are that segment of the payment and transactions industry whose credit scores are not yet established. To target that consumer base, FinTech players have launched BNPL services.

What is BNPL?

It is a payment option that enables you to buy anything without using your own money. You need to sign up with the company that offers you the service of making payment on your behalf at the point of sale. However, you need to repay the amount to your lender within the stipulated period of time. Generally, BNPL offers an interest period ranging from 15 to 45 days. You need to pay monthly interest if you delay repayment, which will also be harmful to your credit score.

BNPL vs Credit Cards

Annual percentage rate

In the case of credit cards, if you pay after the interest-free period average APR might be as high as 45%. While if you make a purchase for the same duration, you will have to pay the highest delay penalty, up to 30% APR.

Credit score

Companies can allot your BNPL card without analysing your credit score, but the bank will not do the same. It might be the reason why BNPL gained popularity among youngsters the most. But, if you haven't built your credit score yet, any delay in repayment to your lending company would destroy your score before even building it. It will take more time to gain the trust of credit rating agencies as a BNPL consumer than in the case of a credit card user.

Minimum amount payment

Banks allow you to pay a minimum amount if you are unable to pay the full balance due on your credit card. The bank will charge a late payment fee if you cannot pay even the minimum amount. Your statement balance is used to determine a flat fee. In the case of BNPL, such a facility is not available. You have to settle the full unpaid amount, or your lender will levy a late fee.

While opting out of any one of two options, always have a look at your financial requirements. If you want to buy an expensive product with longer EMIs, your credit card probably gives you better offers than BNPL.

On the other hand, if you are looking for short purchases on credit, BNPL might have something better for you than credit cards. Assessing your requirements should be the first step in evaluating which option would be best for you.

However, you need to keep in your mind while opting out for BNPL that timely payment of your bills would not improve your credit score, but delay in such will affect your credit score adversely.

Anushka Trivedi is a freelance financial content writer. She can be reached at anushkatrivedi.com