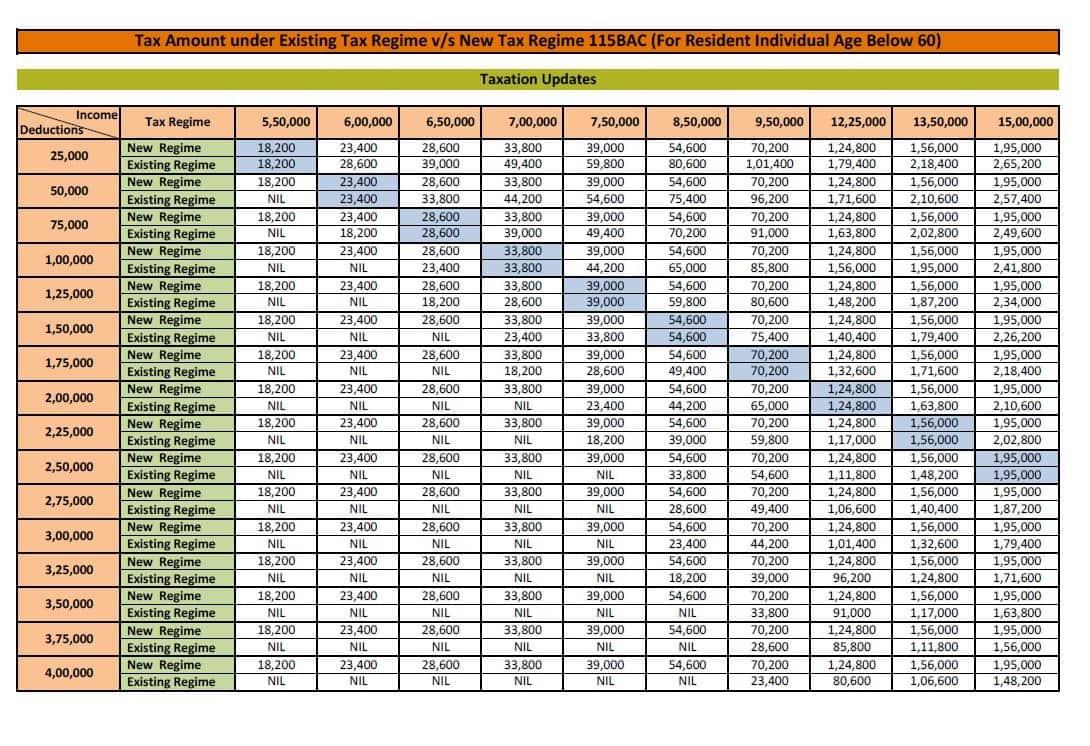

Finance Minister Nirmala Sitharaman, while announcing the Budget 2023 on Wednesday, said that the new tax regime will now be the default tax regime though taxpayers can avail of the deduction and exemption benefits of the old tax regime too. This explains the newly announced income tax slabs that ring in the much-needed relief to salaried taxpayers.

Income tax slabs reduced

In a move clearly aimed at boosting middle-class morale, Finance Minister Nirmala Sitharaman not only charted out new income slabs under the new tax regime but also enhanced the tax exemption limits.

The new income tax slabs under the new tax regime include:

-Income of ₹0-3 lakh: nil.

-Income above ₹3 lakh and up to ₹6 lakh: 5%

-Income of above ₹6 lakh and up to ₹9 lakh: 10%

-Income above ₹12 lakh and up to ₹15 lakh: 20%

-Income above ₹15 lakh: 30%

Further, the government has rejigged the limit set under Section 87A of the Income Tax Act, 1961. The rebate under section 87A of the new income tax regime has gone up to ₹7 lakh.

Gaurav Rastogi, Co-founder, Kuvera, says, “It is a balanced budget for individuals. The intent is clear - to simplify the tax code and to close tax loopholes where possible. So, while the minimum tax slab has been raised to ₹7 lakh in the new tax regime, and the top tax rate has been reduced for high net income taxpayers, the efficacy of some of the other tax breaks earlier available through Section 80C and other schemes have been curtailed.”’

More benefits for salaried taxpayers

The tax exemption limit has been enhanced to ₹25 lakh on the leave encashment amount received by non-government salaried employees. Also, taxpayers earning ₹15.5 lakh or more are eligible for a standard deduction of ₹52,500 in the new tax regime. Currently, the standard deduction is ₹50,000 in the old regime, and the maximum deduction for professional tax is ₹2,500.

An individual with an annual income of ₹9 lakh will have to pay only ₹45,000 tax. The surcharge rate is now 25 per cent from the earlier 37 per cent, thus.

Akhil Chandna, Partner, Tax, Grant Thornton Bharat, said, “Regarding tax proposals, rationalization of the tax rates and slabs under the new tax regime is one of the major proposals which would surely bring cheer for salaried professionals who will have more cash in hand. Reducing the surcharge from 37% to 25% for taxpayers with income above ₹5 crores and opting for a new tax regime would bring some cheer for high net-worth individuals. The government’s focus is clearly to make new tax regime as default tax regime with phasing out of various deductions and exemptions.”

Old versus new income tax slabs

The government’s intent is clear – Encourage people to assess their income tax liability under the new tax regime. This explains the oversimplification of the tax slabs and doing away with the multiple rebates on offer under the old tax slabs.

Manish Khanna, Co-founder, Unlisted Assets says, “Though the new tax system will be the default, taxpayers could choose the previous one. In the new tax system, the FM has also decreased the number of tax slabs. A salaried person currently has the choice to choose the old tax system and keep using the standard tax deductions and exemptions. Otherwise, he or she might choose the new, more favourable income tax system, which does not offer any typical tax breaks or exemptions. The person will have to forego 70 tax deductions and exemptions under the new tax law, such as the HRA tax deduction, LTA tax deduction, and Section 80C deduction of up to Rs. 1.5 lakh, and so on. For people who were unable to take use of the existing tax deductions and exemptions, a new tax regime was announced. Additionally, it assists in reducing the burden of compliance for salaried taxpayers. The benefit in tax slab may give rise to savings and overall investment in the economy.”

A boon for India’s middle class

Many experts from the personal finance sector have hailed the new income tax rules as nothing short of a blessing for India’s middle-income taxpayers who often complained of the hassles they faced while evaluating their tax liability.

Yogesh Agarwal, Founder and CEO, Onsurity Technologies, says, “This is a budget that’s truly designed for India’s Aam Aadmi, one that promotes growth and consumption. Enhancement of the income tax rebate limit from ₹5 lakhs to ₹7 lakhs will greatly boost the country’s middle class, including the rapidly growing gig economy. Extending the benefits of standard deduction under the new tax regime is a move that will give huge respite to salaried individuals. Overall, the government has given India’s hard-working middle-income demographic some substantial reasons to celebrate.”

However, those investing in savings cum insurance policies are unhappy as the new rules render the maturity proceeds from insurance policies taxable. This is because the maturity proceeds of all life insurance policies issued after April 01, 2023 with yearly premiums exceeding ₹5 lakhs will now be taxable.