The new tax regime has an array of reasons to appease most salaried tax payers with lower tax rates and higher threshold of ₹7 lakh for zero tax. But one can’t eat the cake and have it too.

So, with higher income in hand, tax payers have lost their entitlement to some of the tax exemptions, e.g., those under sections 80C and 80D of the Income Tax Act.

It is vital, therefore, to ask whether investors should stop or at least slower the pace of investing in these small saving schemes? Well, the answer depends on who you speak with, but most wealth advisors MintGenie spoke to argue against it.

“Financial planning should never be revolved around the tax planning. When you want to create long term wealth and achieve your financial goals you do not need any incentive or compulsion from the government to do so,” says Preeti Zende, a SEBI-registered investment advisor and Founder of ApnaDhan Financial Services.

Sridevi Ganesh, co-founder of Chamomile Investment Consultants, asserts that tax benefits are additional benefits and not the primary reason for an investor to make investments.

"This budget is set to change the behavioural pattern and general investment scenario. It's not fair to focus on taxation for saving and investing. The idea should be to save to meet your long-term financial goals," she adds.

However, Neelabh Sanyal, COO and co founder, Kuvera.in, believes that young investors should compare the tax payable in the new tax regime versus the old and then take a calculated call.

"Youngsters demonstrate tremendous agility while hunting for the best deal on a smartphone purchase. They should approach this in a similar manner and look for what is the best use of their investible surplus. Tax deductions and exemptions, planned correctly, can be a great way to make your money generate higher returns," says Mr Sanyal.

Investing after removal of exemptions

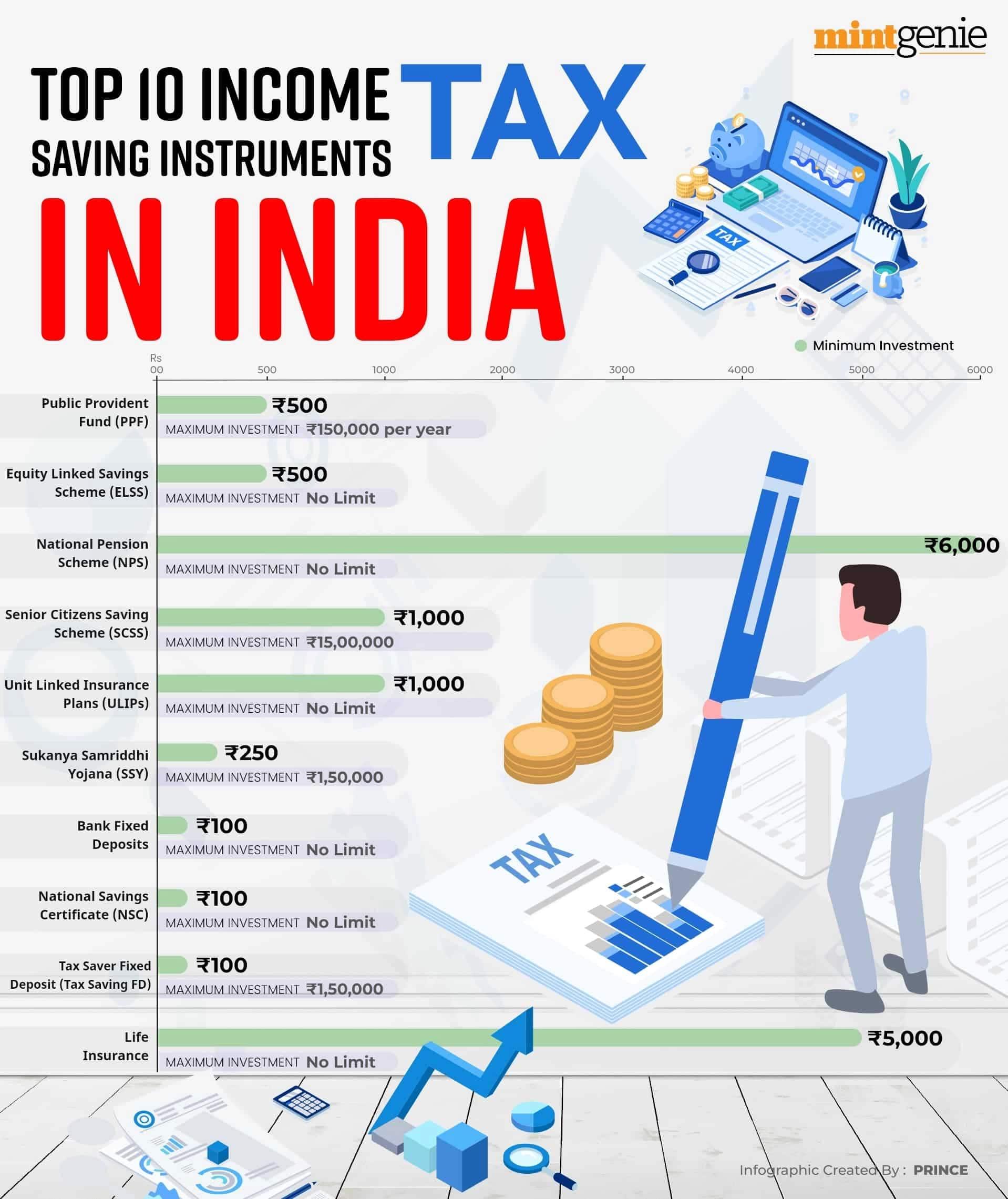

One would wonder if one should still explore to invest in the saving schemes that are no longer eligible for tax incentives under the new tax regime. Some believe that the financial products such as Equity Linked Saving Scheme (ELSS) and Sukanya Samridhi Yojana (SSY) are still attractive for their other features.

“EPF, VPF, PPF and SSY are still the best long-term debt products available today. They still offer tax free fixed interest income and offer real compounding benefit. You should invest in those for your retirement and daughter's education and marriage goals as per your asset allocation,” Ms Zende adds.

“ELSS is one of the important products available under 80C. It helps you buy equity assets and make sure you invest at least for three years. This is still a good product for youngsters to invest and learn discipline for equity investment,” she adds.

Ajaykumar Gupta, president and chief business officer of Trust Mutual Fund, argues that India has been traditionally a nation of savers.

He also sheds light on the ELSS and insurance plans which – according to him – are good investment plans despite the removal of exemptions.

“With the 80C exemption phased out in the new tax scheme, investors should look at ELSS as diversified fund. The reason for young investors to invest in such schemes should continue as investments will take care of you in present and in the immediate future. Buying life insurance protects your spouse and children from the potentially devastating financial losses that could result if something happened to you. The younger you buy, the cheaper your insurance plan,” says Mr Gupta.

One can also explore to invest in National Pension System (NPS) which is a low-cost investment product that lets your money grow up to your 60s. The maturity amount (60 percent lumpsum withdrawal) is still tax-free and can be used as hybrid product towards your retirement.