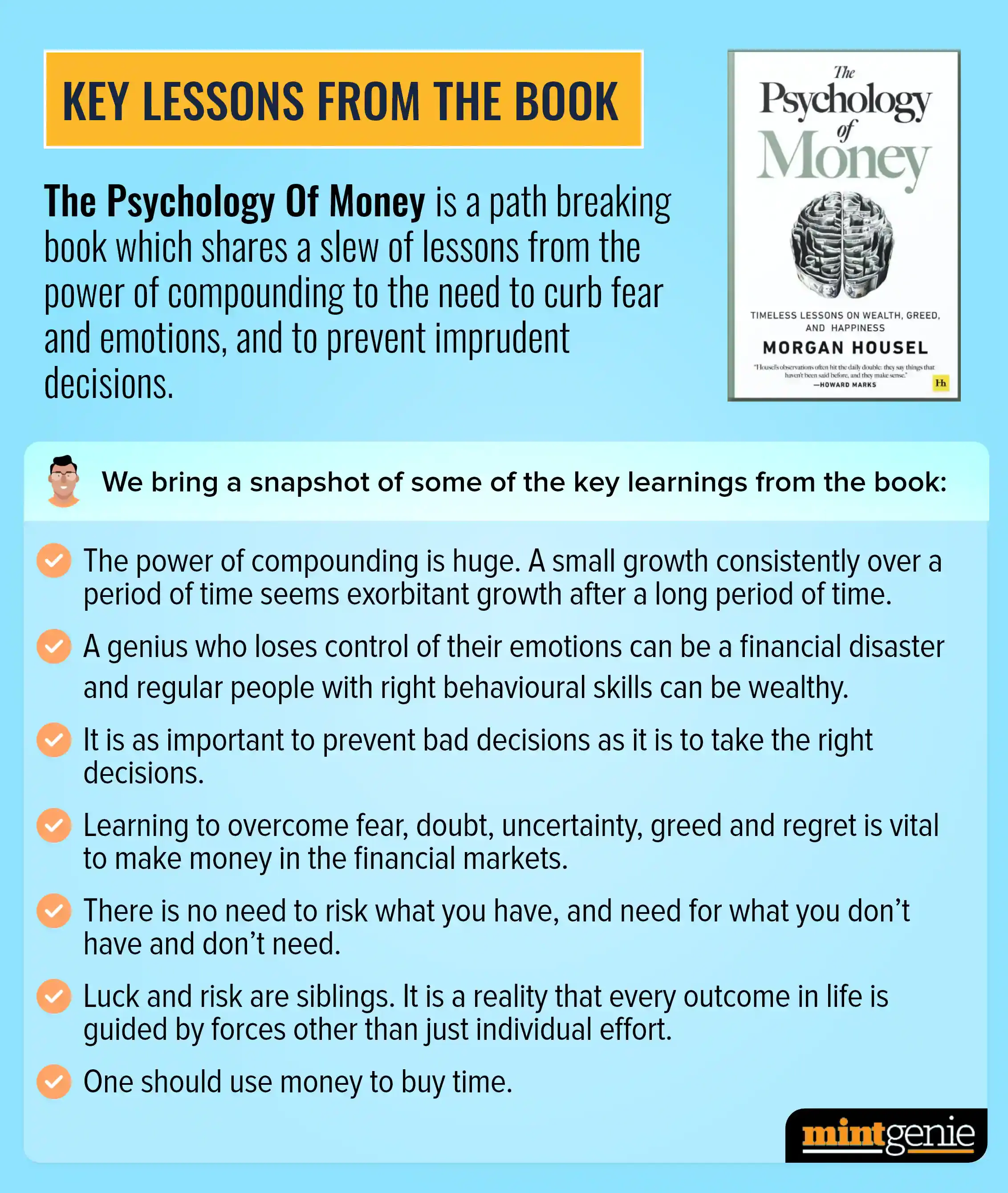

In his bestselling book Thinking, Fast and Slow, Daniel Kahneman wrote that decision-making is plagued with cognitive biases which means objective thinking gets adversely impacted by our tendency to perceive information through a lens of personal experiences and preferences.

Although investors’ behaviour is largely influenced by their actions which are driven by personal biases, some financial experts believe that economic variables, and not these biases, influence the portfolio.

“There would be a rare instance when external forces may not influence someone. Often investors consume external information and form opinions, pessimistic or optimistic, especially during extreme times. These opinions may be biased and create positive or negative impressions. Interestingly, these impressions have no bearing on how the portfolio performs,” Ankur Kapur, founder of Plutus Capital, an independent investment advisory firm.

“The reason is that portfolio is not emotional but instead focuses on the economic variables. When the market crashes, investors want an excuse to sell, and when the market is at an all-time high, investors want to buy. To make sensible investment decisions, an investor must understand the peak and trough of market movements,” he adds.

However, Renu Maheshwari, CEO and Principal Advisor of Finscholarz Wealth Managers believes that investors’ behaviour is paramount in determining the success or failure of their investment.

“There is a saying: There is no risky investment, only a risky investor. Behaviour of an investor is the biggest factor in investment success or failure,” says Ms Renu Maheshwari.

“For instance, the past performance is no guarantee of future performance. Also, it is not rational for investors to invest in an asset class because it is being endorsed by a celebrity. The endorsement can only be a marketing trick, and not a criterion to invest. An investment product should be analysed based on personal financial needs and future macro trends,” she adds.

Here, we list some of these biases which most investors suffer from and also the tips and tricks to deal with them:

A. Relying on recent successes and believing that they set a template for the future:

When something positive happens for a couple of years, some optimistic investors believe that it is the ‘new normal’. However, this is the wrong way to analyse things and the right approach is to see things in the backdrop of long-term trends instead of being carried away with what we witnessed personally as an investor.

The right approach is to pay attention to fundamentals from time to time. Certain economic concepts are nothing short of a foregone conclusion. Merely looking the other way won’t change them such as a direct relationship between money supply and high inflation. Likewise, mean reversion is common and one must keep this in mind before making an investment.

B. The pain of losing one rupee is much more painful than the pleasure of gaining one rupee:

Being emotionally attached to a stock is very common in equity investment. Rather than accepting that loss has incurred, some investors continue to put more money and try to average out the cost of acquisition in order to earn profit at a later stage. This primarily happens because psychologically speaking, the pain of losing one rupee is far more acute than the joy of earning one rupee.

There are several instances where investors bought expensive stocks in triple digits and sold them in single digits because they didn’t accept the ‘loss’ while it was stating them in the eye.

Investors must accept that equity investment is riddled with risk and they should abandon it if they can’t take losses in their stride. Dan Ariely, Professor of Behavioural Economics at Duke University, is quoted often times where he recommends to treat the portfolio value as fresh capital.

Consider if you were to allocate that fresh capital, how would you do it. Would you invest in the same stocks that are at a loss if this were a new investment? This is known as a forward-looking fresh approach to investing minus the burden of past losses.

C. Overlooking statistics and paying attention to a few cases:

According to Michael J. Mauboussin, “Investors who have information about an individual case rarely feel the need to know the statistics of the class to which the case belongs.”

The voices around us and euphoria usually manage to make us overlook the evidence of strong data and statistics. Some investors give priority to the information they have access to instead of seeking the overall macro data that is vital for the right decision-making.

In case of financial markets, fundamentals eventually reign supreme.

Once euphoria dies down, stock prices will revert to their fundamental value. If you are a long-term investor, the only things that matter are data and intrinsic value instead of the popular narrative.

D. Taking a simplified approach when a deeper analysis may be required:

Instead of analysing a company's financial data, investors usually rely on simplistic analogies which are easy to understand. Where difficult number crunching is required to understand the nuances of a company, you can’t simply do away with it by merely ignoring it.

Analysis is not simple. However, skipping this part is likely to be counter-productive. It is advisable to take time to go through some of the grind, or alternatively, one can rely on trusted advisors or analysts that can do the work for you.