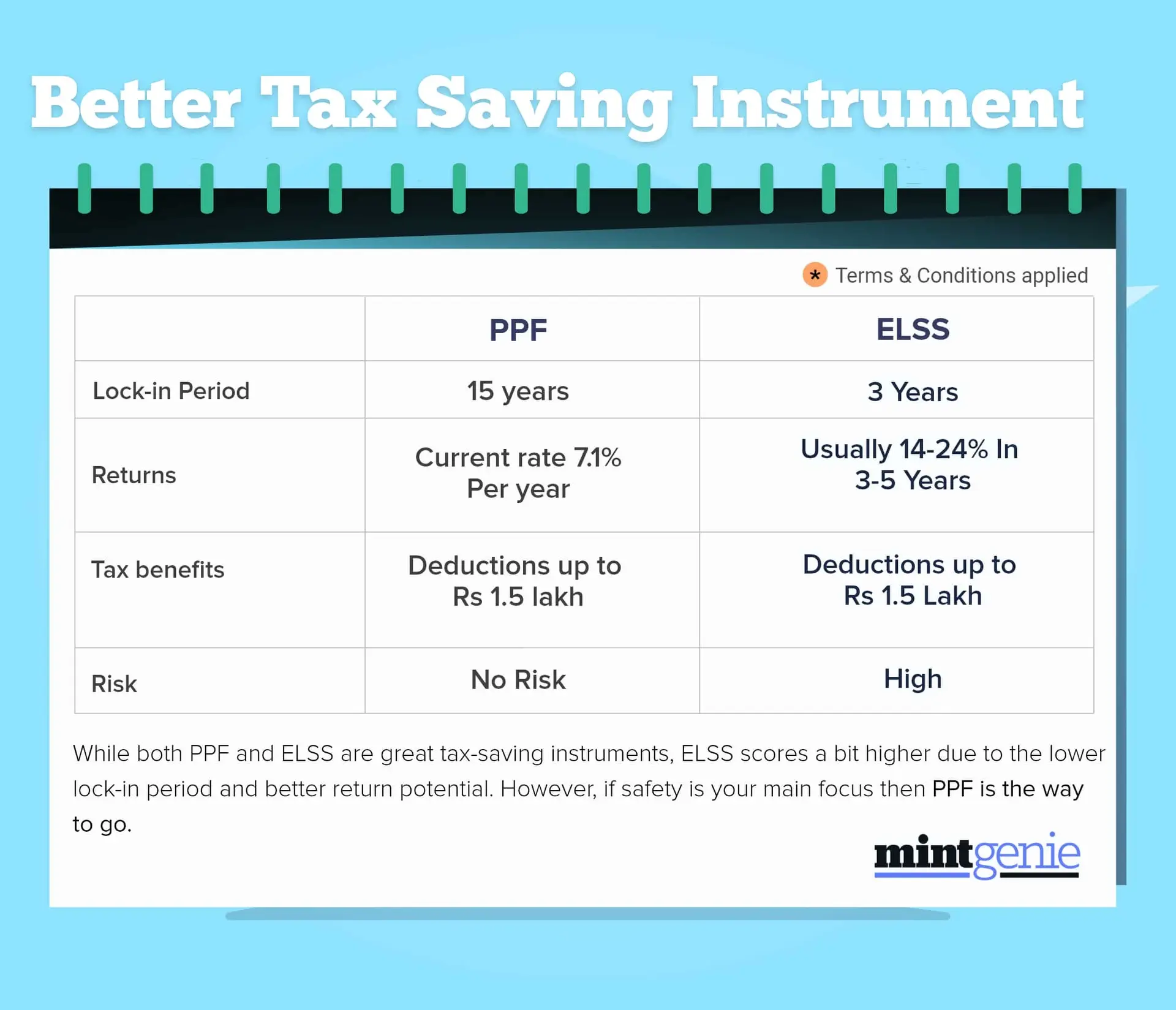

Public Provident Fund (PPF) for many is the first step to growing their money sans any risk. It is also an effective tax-saving measure, which is why, it is popular not only among the salaried people but also among businessmen who prefer putting a part of their earnings in this fund.

The investment can be made on a monthly, quarterly, half-yearly or annual basis depending on the investors’ financial viability and outlook. The maximum investment allowed in this fund is ₹1,50,000 a year.

Though most of us are aware of this investment’s ‘Exempt-Exempt-Exempt’ (EEE) benefits, many still wonder if it is possible to build up a sizeable corpus using this option. The answer is “Yes”, provided one begins investing early.

Here's an example:

Case 1: Assuming that you start investing in PPF at the age of 18.

Monthly investment: ₹12,500

Interest rate: 7.1%

Investment tenure: 15 years

Then, you have

Invested amount: ₹22,50,000

Estimated returns: ₹17,70,301

The total value of the investment: ₹40,20,301

This means that you have a corpus of ₹40,20,031 as you turn 33 years old.

Assuming that you start a fresh PPF investment again.

You will again have ₹40,20,301 (at the same rate) when you turn 48 years old.

Another fresh PPF investment at the age of 48 will yield you ₹40,20,301 again when you are 63 years old. This way, you end up accumulating a corpus of ₹1,20,60,903.

Your dream of becoming a “crorepati” is accomplished with a simple PPF investment.

Case 2: Some may also argue that PPF investments can be extended by another five years.

You already have a corpus of ₹40,20,031 as you turn 33 years old which you leave for another five years in the PPF account to continue earning the 7.1 percent interest. This means:

Total deposited amount: ₹40,20,031

Total earnings: ₹16,44,666.93

The total value of your corpus: ₹56,64,697.93

At the age of 38 years, you have ₹56,64,697.93 in your savings account.

Some people may not like to keep their earnings idle, which is why they may continue to invest in the extended five-year investment period too.

Invested amount: ₹30,00,000

Estimated returns: ₹36,30,221

The total value of the investment: ₹66,30,221

This means that at the age of 38 years, you have ₹66,30,221 in your savings account.

Assuming that you again invest in a fresh PPF account at the age of 38 years, with investments remaining the same, you will again have ₹66,30,221 as you turn 58 years old. This way, you will have a lump sum amount exceeding a crore even before you turn 60 years old.

You reach your financial goals quickly; your journey towards achieving financial independence is free of unwanted obstacles, thus, leaving you free to focus on other investments or other important aspects of your life.

Contrary to the conceived idea of PPF being just another investment, statistics prove that even a small investment of ₹12,500 done every month, without fail, can help you amass an amount that only a few can imagine.