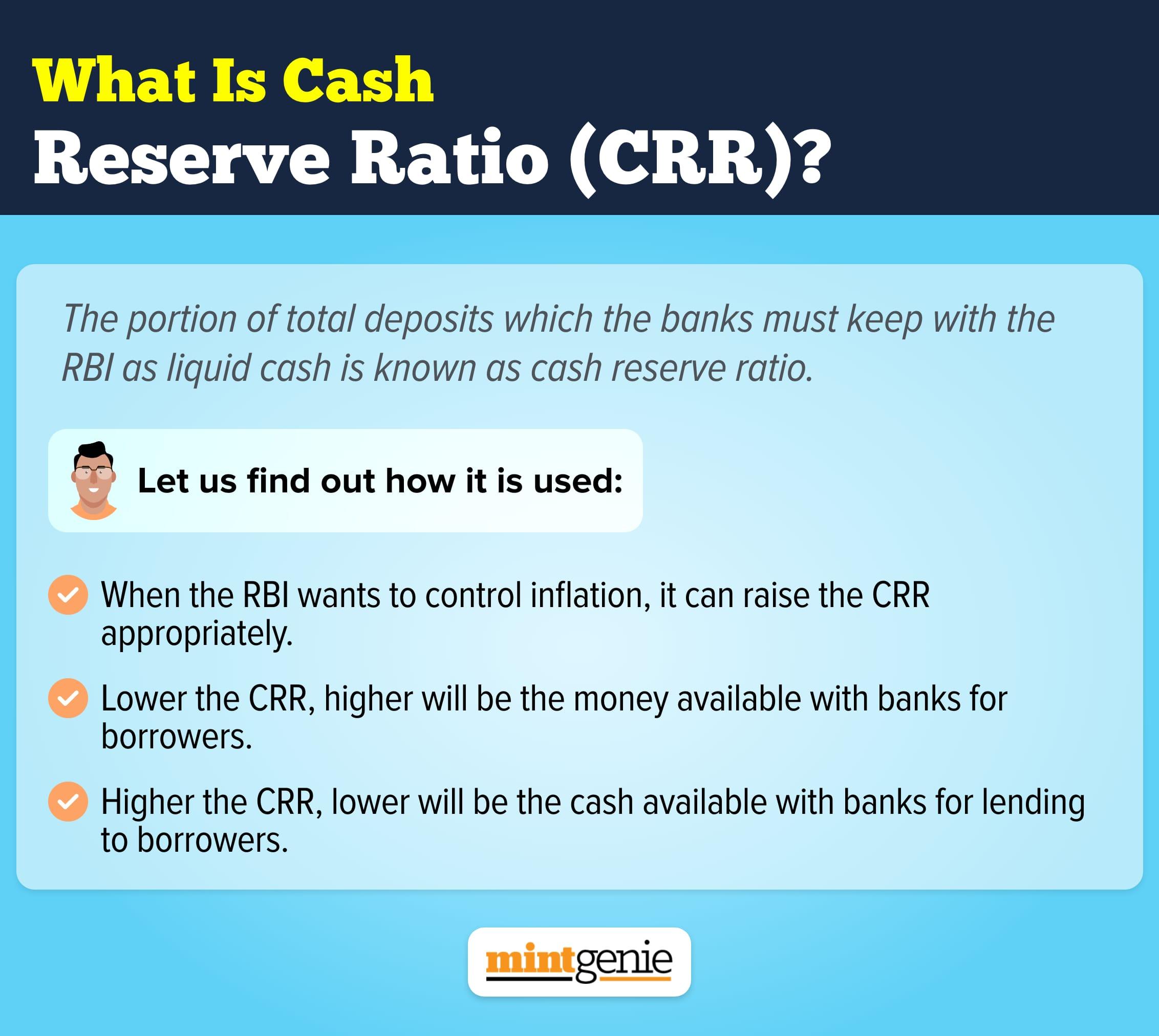

Cash Reserve Ratio (CRR) is the proportion of total deposits which the banks are supposed to keep with the Reserve Bank of India (RBI) in the form of liquid cash. Cash Reserve Ratio is calculated as a percentage of the bank’s NDTL (Net Demand and Time Liabilities). Demand liabilities include current deposits, savings accounts, demand drafts and cash certificates while time liabilities include fixed deposits and gold deposits, etc.

Since the money is parked with the RBI, it ensures complete safety of deposits. Cash Reserve Ratio is also used as one of the key rates to determine the base rate, which is the minimum lending rate below which a bank is not permitted to lend funds to borrowers.

To control inflation

When the central bank is geared to control rising inflation, it can use the weapon of CRR in its armoury, and raise it appropriately. As a result, the banks are left with relatively less available cash for lending to borrowers. With liquidity sucked out of the system, inflation is likely to cool down as an aftermath.

On the other hand, when the RBI wants to inject more money into the system to spur inflation, it slashes the CRR. With this, the banks get more money in their coffers that they can lend to borrowers. In other words, lower the CRR, higher will be the money available with banks for borrowers. And higher the CRR, lower will be the cash available with banks for lending to borrowers.

Meanwhile, there is a flip side to keeping a high cash reserve ratio (CRR) for too long. As we know that banks earn their income by lending loans to borrowers, so when a high percentage of money is parked with the RBI in form of CRR, the banks do not fetch any interest on it. However, it is one of the vital tools through which RBI regulates the banking sector – and maintains stability, security, and keeps inflation under control.