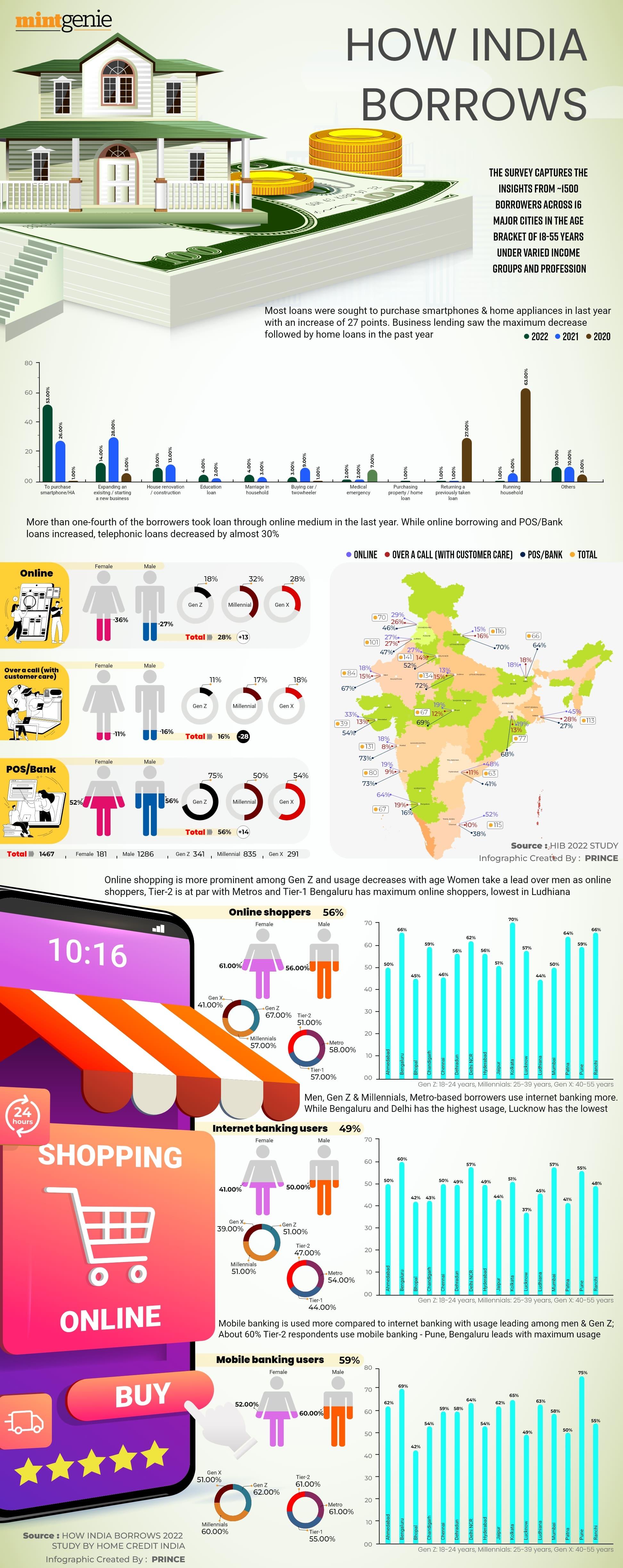

So much is being written about increased interest rates on home loans and their effect on home loan tenures that many borrowers are now turning to personal financial advisors to get rid of the loans faster. Repaying the loan within the predetermined loan tenure is important.

Consequent to higher interest rates, borrowers may choose between higher equated monthly instalments (EMIs) and extended loan tenures. Choosing the lower EMI option will result in more disposable income. However, a reduced loan tenure translates to greater interest savings.

At the outset, while it may seem that higher interest rates do not affect EMIs too much, assessing the total interest outgo highlights how increasing interest rates can cause a tremendous dent in our pockets. Take, for example:

At 6.5 percent interest, a ₹50 lakh loan taken for 20 years translates to ₹39,46,879 in interest.

At 7.0 percent interest, a ₹50 lakh loan taken for 20 years translates to ₹43,03,589 in interest.

At 7.5 percent interest, a ₹50 lakh loan taken for 20 years translates to ₹46,67,119 in interest.

At 8.60 percent interest, a ₹50 lakh loan taken for 20 years translates to ₹54,89,954 in interest.

At 8.65 percent interest, a ₹50 lakh loan taken for 20 years translates to ₹55,28,083 in interest.

However, prepaying the loan means lower interest outgo

At 6.5 percent interest, a ₹50 lakh loan taken for 15 years translates to ₹28,39,967 in interest.

At 7.0 percent interest, a ₹50 lakh loan taken for 15 years translates to ₹30,89,455 in interest.

At 7.5 percent interest, a ₹50 lakh loan taken for 15 years translates to ₹33,43,112 in interest.

At 8.60 percent interest, a ₹50 lakh loan taken for 15 years translates to ₹39,15,491 in interest.

At 8.65 percent interest, a ₹50 lakh loan taken for 15 years translates to ₹39,41,965 in interest.

Opting for an extended loan tenure versus higher monthly interest outgo has a lot to do with your priorities as you decide between lowering your interest cost and increasing your disposable income.

However, if you decide to prepay your loan and get rid of it early while saving on the total interest outgo, you must be ready to factor in the following necessary conditions.

Do not use your emergency fund

You create an emergency fund to pay for emergencies. Irrespective of how high the interest rates go, you cannot simply use the money set aside in this fund to prepay your loans. The primary goal of maintaining an emergency fund is to deal with financial emergencies or to meet unavoidable expenses during periods of income loss due to job loss, illness, or disability. An emergency fund should ideally be large enough to cover unavoidable expenses for at least six months, such as children's tuition, existing EMIs, insurance premiums, rent, and so on.

To meet financial obligations, using your emergency fund to pay off your home loan may force you to take out loans at much higher interest rates or redeem other investments at sub-optimal prices.

Don’t liquidate investments made to achieve financial goals

Nothing can be worse than redeeming your investments just to prepay your loans. Though you get rid of the loan faster, you will find yourself in a financially sticky situation once you find that you had not saved or invested enough to pay off your expenses in the future.

In order to reduce their overall interest cost, many home loan borrowers redeem their existing investments. However, this can potentially harm their liquidity and long-term financial health. In order to meet their critical financial goals, they may be forced to take out more expensive loans.

Determine the amount of investment required to meet your critical financial goals, such as children's education or retirement funds, using online financial calculators. Make prepayments without affecting your existing investments for these financial objectives.

Be careful during home loan balance transfers

The term home loan balance transfer (HLBT) refers to the process of transferring your existing home loan to another lender with lower interest rates and/or better terms and conditions. It is especially beneficial for those who previously obtained home loans at higher interest rates and are now eligible for home loans at significantly lower interest rates. The lower interest rate obtained by exercising the HLBT will reduce the interest payout while having no effect on liquidity or existing investments.

Before making prepayments, existing home loan borrowers should look into the possibility of transferring their loans to other lenders at significantly lower interest rates. If the new lender offers it, those considering the HLBT should look into the home loan overdraft option, which is a home loan variant.

Prepay from interest on existing investments

The urge to get rid of loans quickly has prompted many to look for alternative investments to repay loans on time or before the predetermined period. While home loans have one of the lowest lending rates of any retail loan category, their interest rates are still higher than the majority of fixed-income instruments' returns. Those who have surpluses in fixed-income products like fixed deposits, short-term debt funds, and so on that are not tied to any critical financial goals can use them to prepay their mortgages.

Prepaying the loan may be difficult but not impossible

Existing home loan borrowers who want to reduce their EMIs and increase their disposable income should select the EMI reduction option. Those looking to save money on interest should consider the tenure reduction option.

Existing home loan borrowers should first consider the HLBT option if they have the potential to save significantly on interest costs by transferring their home loan to another lender with significantly lower interest rates.