The recent BankBazaar report titled “Moneymood Retail Credit Trends” highlighted how the growth of the credit market in 2022 underlined a sustained rise in bank credit during the year. The statistics indicate an increase in the number and size of loans sought and disbursed, indicating that many people relied on credit to meet their financial needs.

The report in its 2022 trends shared, “The demand for credit remained high despite massive rate hikes. Home financing had a great year as pent-up demand was serviced. Credit cards became indispensable as the first line of credit. Secured loans such as loans against FDs grew rapidly, indicating a mature borrower segment that does its homework before accessing credit. Small unsecured loans grew the fastest.”

Dev Ashish, Founder, Stable Investor, said, “Given the rise in disposable income and low rates of home loans till just a few months back, there was a solid recovery in real estate demand. But while the recent uptick in loan rates has still not hurt the demand much in the housing space, there might be some demand moderation if loan rates rise further on the back of RBI rate hikes in the next few months. The rate hikes have anyways made home loans dearer. So a further increase in loan EMI outgo may put rate-sensitive borrowers in a dilemma.”

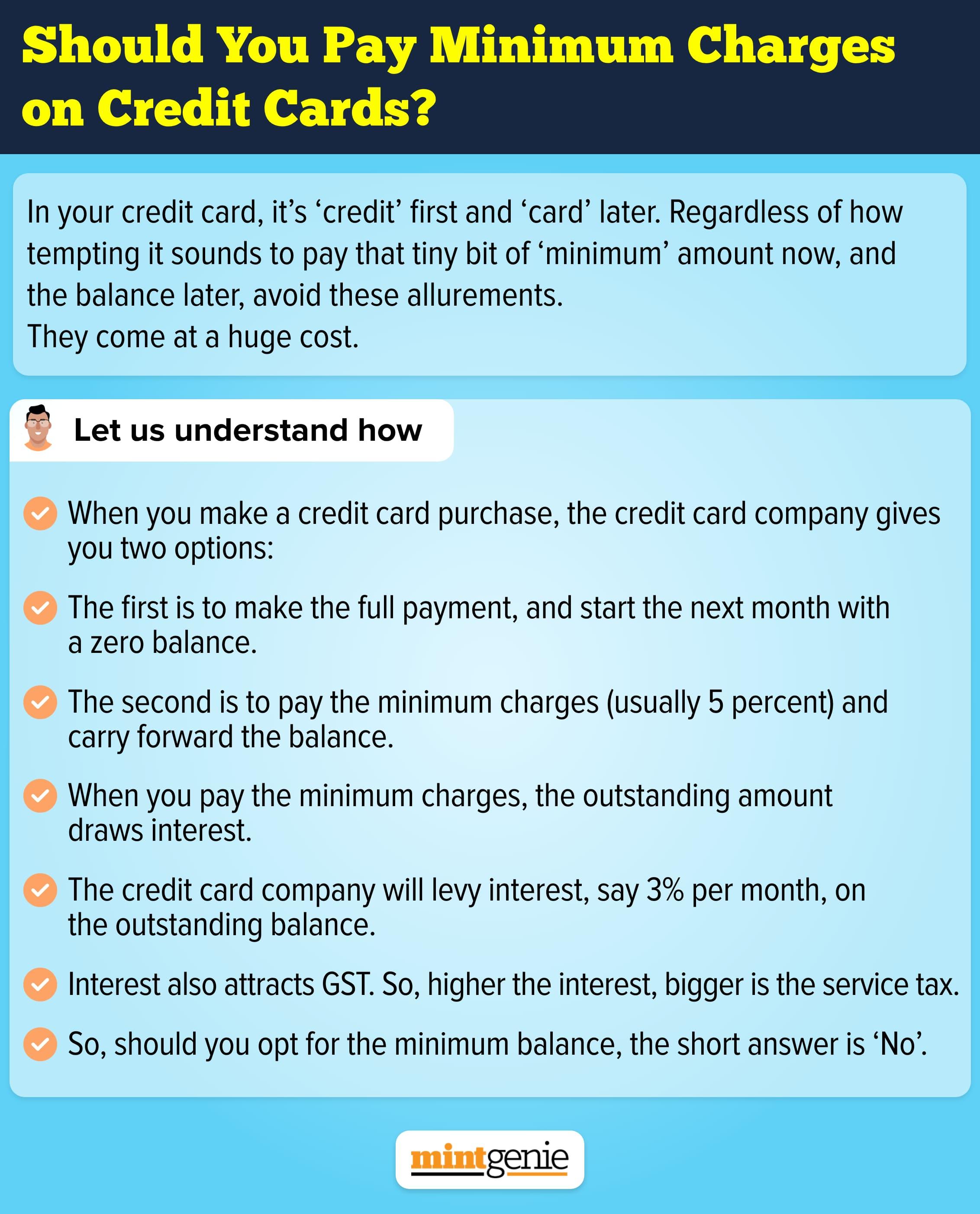

Dependence on credit cards set to rise

Investors are looking forward to an economic recovery in 2023 though the fear of inflation and recession continues to engulf their minds. However, recent repo rate hikes and policy measures signal the easing of inflation, which in turn will encourage people to seek small unsecured loans. In all, one can expect the credit segment to continue doing well barring the effect of unforeseen macro factors like war or disease that may cause an unexpected upheaval in the country’s economy.

The credit card segment has done exceptionally well as the card issuing companies lured credit-seeking customers with their “Buy Now Pay Later” schemes. Banks and fintech organisations came together to launch co-brand cards that quickly found their way into customers’ wallets. Given how quickly prices rose due to inflation, many people relied on credit cards to keep up with the rapid rate hikes in the prices of daily necessities. The data shared by BankBazaar reveals credit card disbursals grew up by 103 percent while reward card issues went up by 48 percent. The love for premium cards continued unabated while the use of fuel cards went up by 22 percent to mitigate the effect of rising petrol costs.

Viral Bhatt, Founder, Money Mantra, said, “In my view the BNPL segment will increase more in coming years and specially 2023. BNPL is ideal for new-to-credit customers or young Indian millennials who don’t possess credit cards but need quick, hassle-free access to short-term credit. But, while it does sound enticing, you need to read the fine print and understand the repercussions of missing payments. All-in-all, it’s a perfect scheme for the responsible consumer.”

A testing time for property buyers

Regardless of how many financial experts advise against buying a home, many Indians continue to harbour the dream of owning a home early in their lives. Apart, government-backed subsidy schemes and cheaper loans helped till inflation came knocking at our doors and the Reserve Bank of India responded with recurring repo rate hikes. However, despite rising loan rates, the demand for home loans has not subsided. Though many borrowers continue to complain about increased EMIs or extended loan tenures, RBI data shows home loans grew 8.4 percent between March and October, faster than the preceding six-month period during which there were no hikes.

Suresh Sadagopan, MD & Principal Officer, Ladder7 Wealth Planners, said, “Buying a home is a major goal for most people. Buying a home without a home loan is virtually impossible for most. Hence, home loans will continue to have traction irrespective of the interest rates going up and is expected to continue in the years ahead as well.”

At the current rate, the segment is expected to grow to ₹20 trillion and maintain its share through the new year as real estate continues its post-pandemic upswing.

Personal loans get dearer

Too many small loans hitting the market have refrained many people from seeking personal loans. Though the retail credit demand has hit pre-pandemic levels, personal loan demand is way down compared to the pre-pandemic period.

As post-pandemic life unfolds, the demand for unsecured debt will remain high as people look to restart their businesses, travel, shop, or buy big-ticket items like vehicles or electronics.

Ashish adds, “While an increase in loan rates of small-ticket-sized loans isn’t felt much at the monthly EMI level, a lot will depend on how the job market pans out in the next few quarters. If India remains a safe haven for growth and there is no major slowdown, the demand for unsecured loans will continue to see growth”

Opting for loans against assets

Loans secured by fixed deposits, gold, stocks, and bonds constitute a minor portion of the retail credit market. These were, however, rapidly expanding markets. Indians borrowed wisely as interest rates rose, pledging assets in exchange for lower rates. Loans against fixed deposits have grown 54 percent since the end of 2020, while gold loans have grown 58 percent in the same time period.

The data shows people have realised the value of securing loans by using their assets as collateral, allowing them to obtain lower-cost loans. As opposed to the earlier behaviour of liquidating bank deposits, gold and mutual fund investments, borrowers have found a way around getting loans without losing their investments. They simply seek loans against assets, thus, allowing them to benefit from both loans and earnings from their investments.

Slow demand for education loans

Among the retail loans, the rise in the demand for education loans remained the lowest. One may attribute this to the difficulty students face in accessing education abroad.

Sadagopan adds, “Education loans can get affected due to the rupee weakening and consequently the cost of education itself going up. Also, with the spectre of a recession looming in many countries like the USA, Canada, Eurozone, etc. students will be far more circumspect and cautious while considering education abroad. As a result, demand for education loans may fall in the near term.”