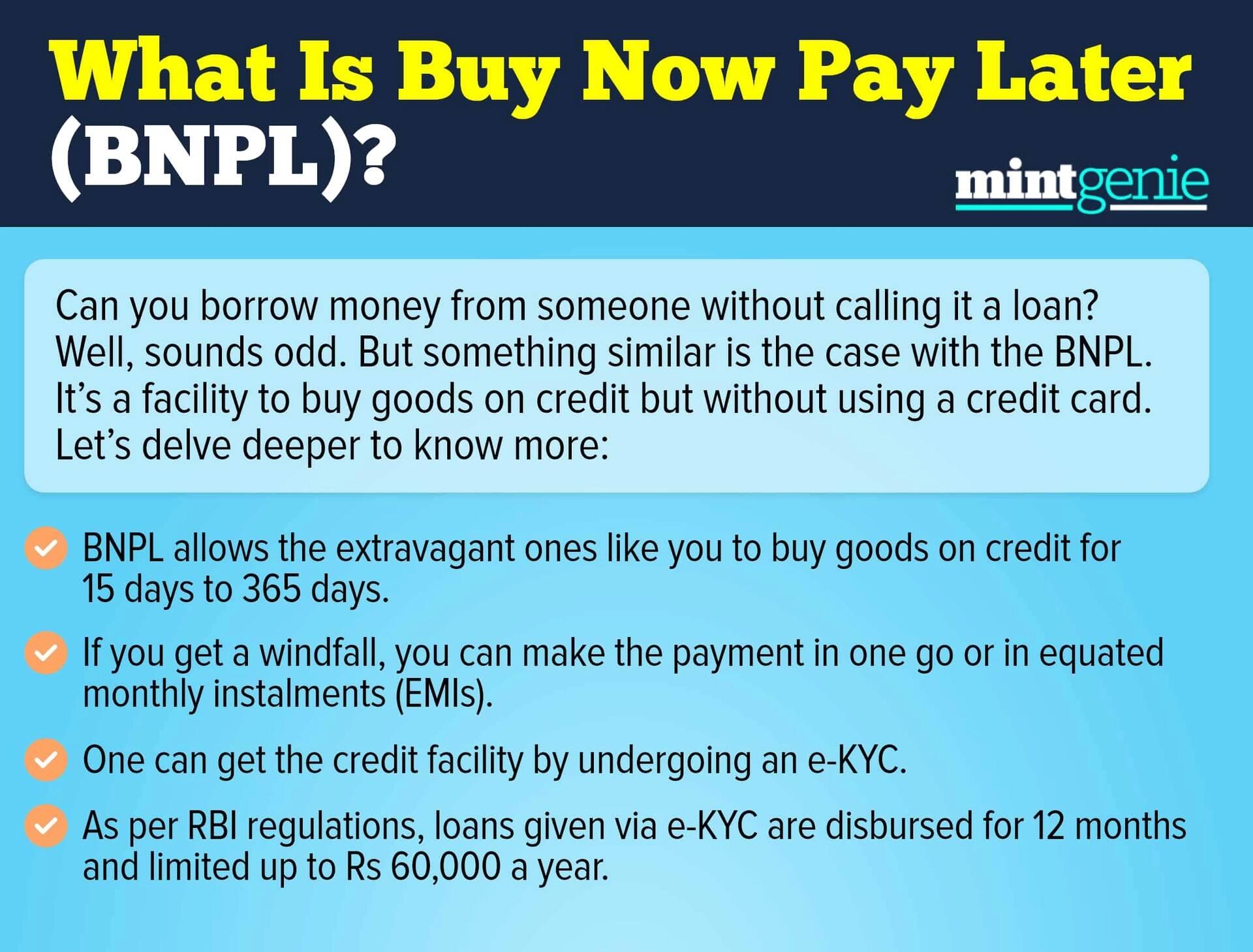

The Reserve Bank of India (RBI) released a regulatory framework for digital lending recently. The set of rules are applicable to the entities regulated by the banking regulator and any lending service providers (LSP) that these entities engage.

It all started in June this year when the banking regulator directed the non-banking fintech firms that the prepaid payment instruments master directions do not permit the loading of prepaid payment instruments from credit lines. And the impact was immediate. The number of new prepaid cards issued by these firms dropped to lower than a lakh against 5-7 lakh in the month of May.

During that time, the flexibility which fintech firms implicitly enjoyed was seen as their misinterpretation of RBI’s master directions and hence, the industry players felt that a proper regulatory framework was the need of the hour.

And here they come!

However, it is vital to mention that the Reserve Bank on January 13, 2021 had constituted a Working Group on ‘digital lending including lending through online platforms and mobile apps’ (WGDL). And these rules are borne out of this working group after a number of suggestions from various stakeholders were incorporated into it.

“This regulatory framework is based on the principle that lending business can be carried out only by entities that are either regulated by the Reserve Bank or entities permitted to do so under any other law,” stated the RBI.

For borrowers’ protection

The banking regulator has categorically mentioned that any fees or charges, etc that are payable to the LSP in the process of credit intermediation will be paid by the regulated entities directly and not by the borrower.

RBI also clarified that all loan disbursals and repayments will be executed between the bank accounts of borrower and the regulated entities without any pool account of the lending service providers (LSP) or any third party.

When a borrower takes a loan, it will be mandatory for the lender to provide a standardised Key Fact Statement (KFS) to the borrower before executing the loan contract.

Something that will come as a relief to borrowers is that automatic increase in credit limit without explicit consent of borrower will now be prohibited.

Borrowers will now be given an opportunity to avail a cooling off period during which they can exit digital loans by paying the principal and the proportionate APR without any penalty as part of the loan contract.

The regulated entities will make sure that the lending service providers have a nodal grievance officer to deal with complaints. The details of these grievance officers will have to be prominently indicated on the website of these entities as well as those of lending service providers.

The borrower will have an option to escalate the complaint to the ombudsman in case it is not addressed within 30 days.

The regulations are seen as a welcome move by the industry players.

While commending the latest regulations, Vishal Dhawan, Founder of Plan Ahead, an investment advisory firm, says, “The benefit of an explicit consent of the borrower is that credit behaviour of the investor can be controlled, as the investor has the ability to actively decide whether or not he wants access to more debt, and whether his financial position permits him /her the additional burden of interest.”

“We welcome the digital lending guidelines announced by the RBI. We see these guidelines as extremely positive measures for customers and thereby fintech companies who follow industry best practices. Specific to digital lending, we also believe the guidelines make it abundantly clear that India will not be a market where regulatory loopholes can be exploited to build businesses,” said Lizzie Chapman, CEO & Co-founder, ZestMoney and President, Digital Lenders Association of India (DLAI).

“Overall, the recommendations identified for implementation is good news for serious and credible fintech companies who believe in scale against a backdrop of high levels of consumer protection,” she added.