In a country where financial literacy is still isn't part of school curriculum, teaching about money to kids solely becomes responsibility of their parents. Although, some state governments like Maharashtra have taken steps in introducing financial literacy as a subject in schools, there's still a long way to go.

This is why, teaching about money and making them responsible about their spending habits is a key role parents discharge in their duties towards their children.

Now, financial-technology (FinTech) startup space is doing its bit to make your lives easier.

There are a number of pocket money cards which enable parents to know how much money their child is spending, and importantly on what service.

Also known as prepaid cards for teenagers, these cards are linked to the apps downloaded on the parents' cell phones. The adults, through the app, can monitor the spending habits of their growing — but yet not grown — children.

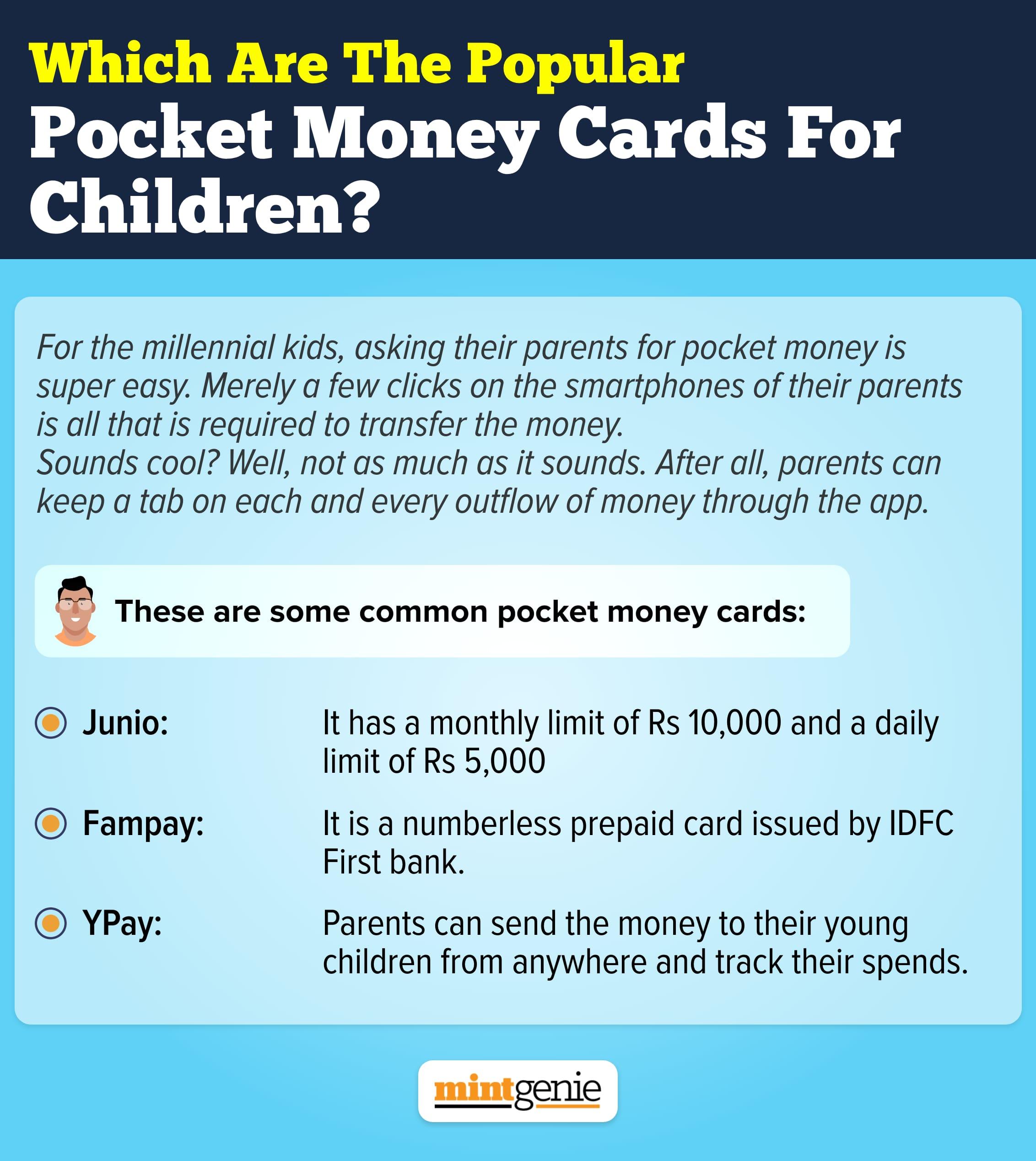

Junio: It is a smart card that enables parents to give pocket money to children connected to the junio app. Parents need to upload money on the app and the card can be used for making online and offline payments.

As a matter of fact, there are no monthly or annual charges for the card. To be able to use it, one must reload it just as any other prepaid card. The charges are ₹99 as a one-time fee for ordering delivery of physical cards. However, the virtual card is free.

The card’s daily limit is ₹5,000 while the monthly limit is ₹10,000. You can set up pocket money on a weekly, bi-weekly and monthly basis.

Fampay: Issued by IDFC First bank, it is a numberless prepaid card. It is secure and easy to use card that follows an end-to-end encrypted system. One has to use two-factor authentication for payments.

The online card can be accessed as soon as you create an account with Fampay. In case the user wants to make purchases at an offline market, one has to place an order for the physical card. One can swipe the card or use the tap and pay feature to transfer money digitally on online marketplaces such as Aamzon, Netflix, Swiggy and Zomato.

The physical card has no numbers printed. The card numbers and CVV are stored in the FamPay app. This makes the card secure. In case the card is lost, it can be blocked anytime from the app. The young users can make offline purchases upto ₹2,000 on PoS (point of sale) machines in a day.

YPay: This can also be operated from the YPay application on smartphones. The user (minor) does not need a bank account to be able to use the smart card. It facilitates a secure and safe mode of transaction. It is a smart card for students who stay away from the parents who send money to their children from anywhere.

The parents can also place monetary limits on these cards. They can also keep a track on where the money is being spent.

These apps operated smart cards play an important role in preventing the teenagers from over spending the money. They also help them inculcate a fiscal discipline and become financially responsible and independent.

Slonkit: Just as pocket money cards, there is a prepaid card linked to Slonkit, a money management app. After completing the KYC (know-your-client), a prepaid card issued by DCB Bank is sent to the applicant in a week’s time. It can be used at all points of sale that accept Visa cards. One can load ₹1 lakh at any point but not more than ₹12 lakh in a year.

Bank accounts

Aside from these pocket money cards; some banks have also started to allow minors to open banks accounts. These accounts are essentially meant to inculcate the habit of saving and to make them learn the importance of money management among children.

For instance, Federal Bank in 2021, launched Fed First, a special savings account scheme for minors. This was to develop healthy saving and spending habits.

The account is designed to enable children to learn the importance of money management. This offers some unique features and offers.

Likewise, Fino Payments Bank also runs a savings account called Bhavishya for minor children between the age of 10 and 18.

As some parents to facilitate investment for their minor children. In fact, they are allowed to invest in mutual funds, but this can be done only through a joint bank account opened with minor as one of the account holders.

Even capital markets regulator SEBI stated some time ago that mutual fund investment in the name of minor can be made via bank accounts operated jointly by them.