I am sure you have read or heard this advice quite often – keep money worth 6 months’ expenses separately as an emergency fund. Haven’t you?

Though the idea of having a contingency buffer is old and simple, it is still a powerful one. You set aside money for emergencies which are uninsured, unexpected, unplanned and most important, can cost a bit of money. These can be sudden repair expenses, medical expenses, travel expenses, etc. At times, your extended family’s emergencies become your own emergency and you need to loosen your pockets.

So you can consider it a rainy day fund. Just like an umbrella. You will not need it on regular days. But when it does, and you don’t have one, then you will struggle.

Coming back to the topic – Isn’t 6 months’ expense buffer enough?

It is for many. But not for everyone.

And that is because due to a combination of different factors, some people should ideally have bigger emergency funds. Let’s see why.

READ MORE: Should self-employed choose a large emergency fund?

Sometimes, having a bigger emergency fund is necessary

Job security & risk of income loss

If you have a safe, sort of guaranteed-for-life kind of government job, then you can even live with a smaller emergency fund. Like up to 3-4 months’ worth of expenses. And that is because the chances of job loss and income stopping suddenly are almost nil. But if you work in industries/sectors or even countries (like the Middle east) which are prone to layoffs and opportunities for reemployment are lesser, then you need a bigger cushion. Something like 9 months to even 15-20 months’ worth of expenses can be considered.

No. of earning members in family

If you are the sole earning member of the family, then you know that any loss of income or big expense can derail your entire family budget. On the other hand, if you and your spouse are earning well and have very few dependents, then the risk of both incomes stopping together is extremely remote. So if you have many dependents and/or you are the sole earner, then it’s better to have a bigger buffer. First, make sure you have accumulated a 6-month Emergency Fund. But don’t stop there. Gradually, increase this fund to something like 9-12 months. This can be done via accumulating some money every month (say via RD) or using part of your annual bonuses to do it in one go.

No. & type of dependents

If you only have your spouse and one child, then your requirements will be different from someone who has a spouse, 2 kids, 2 dependent parents and occasional dependency from in-laws. Isn’t it? Many people have old parents who are dependent as well as have regular medical expenses (which are not covered under health insurance). So for them, it’s always better to have a bigger buffer.

Also, not just one but all the above factors may be applicable to you. If so, make sure to give priority to increasing emergency fund size versus all other goals.

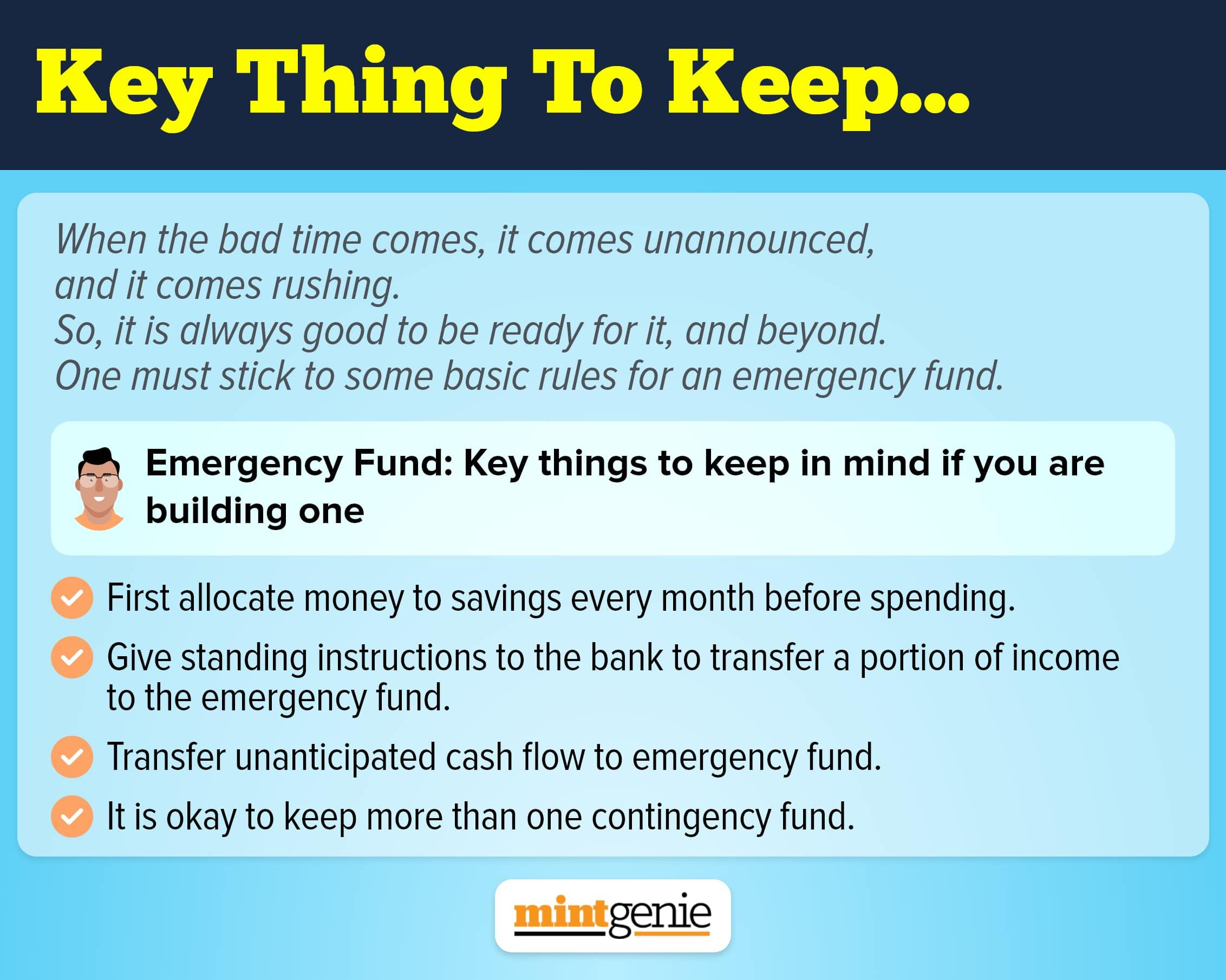

READ MORE: Emergency Fund: Key things to keep in mind when building one

Where to put your emergency fund?

When putting aside money for emergencies, you should not go after high returns. Remember that high returns come with high risks. And you don’t want to be in an emergency when you need money but due to high-risk taking, your money is now parked in instruments which are under heavy losses.

So importance should always be given to liquidity, ease of access and safety when parking your emergency money.

Where to do it?

For small amounts, a combination of a separate savings account and fixed deposits is enough. If you want a larger corpus set aside for emergencies, then even liquid funds can also be added to the mix.

And please don’t consider your credit cards as an emergency fund. And that is because once the bill comes, you will have to eventually pay back the money. So credit cards can be used for emergency expenses, but having an emergency fund to repay the bill is still needed.

Emergency fund also protects your wealth

Sounds strange. But it is true. If you have an emergency fund, then you will not have to dip into your other long term investments. That way, your savings for other goals remain intact and don’t see any unnecessary withdrawals.

I know it’s easy for us to say that you should have a bigger buffer than to put one in place. But this is what is required if your situation demands it. Hope for the best but don’t make this hope your strategy. Plan properly and scale up your emergency reserves. That way, you will be in a stronger position to manage unexpected expenses in future without compromises.

Dev Ashish is a SEBI-Registered Investment Advisor and Founder (Stable Investor). He provides fee-only financial planning and investment advisory services to small and HNI clients across India.