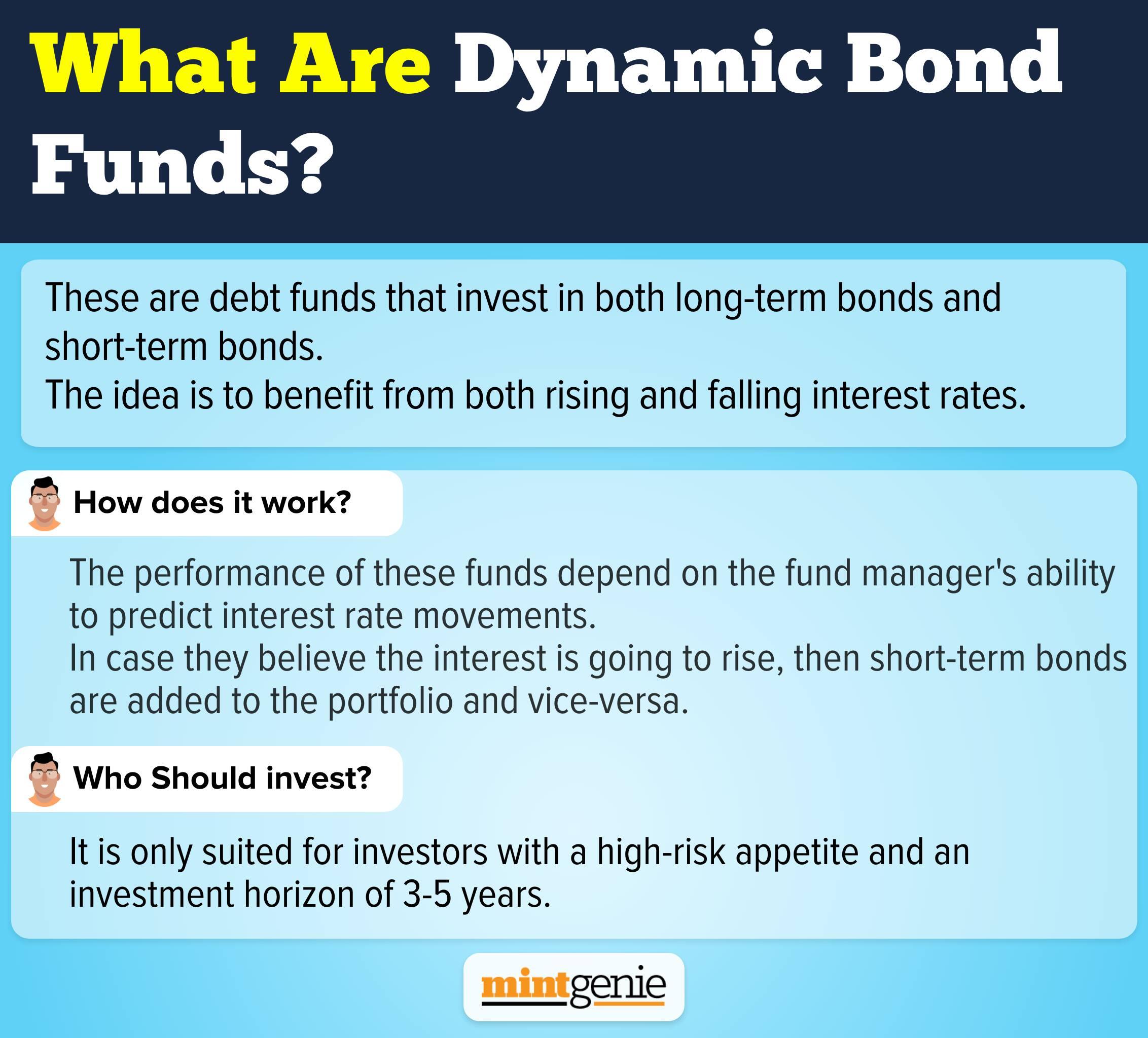

Debt funds are a type of mutual fund whose performance depends on interest rates. When interest rates rise, debt fund returns drop and vice versa. A dynamic fund is a debt fund that benefits from both rising and falling interest rates.

They alternate portfolios between long-term bonds and short-term bonds depending on the underlying interest rate scenario which helps them provide generous returns in fluctuating rate cycles.

As the name suggests, these funds are dynamic in terms of maturity. Generally, debt funds are closed-ended invested in long-term bonds and short-term bonds. Dynamic funds are open-ended investments in both types of bonds. Their main objective is to provide ‘optimal’ returns despite market volatility.

How does it work?

The fund manager of a dynamic firm plays a very important role in managing the portfolio and its performance depends on the manager's ability to predict interest rate movements.

For example, if a fund manager believes the interest rate is about to fall, he/she can increase the fund's tenure. In case he/she believes the interest is going to rise, then short-term bonds are added to the portfolio.

When interest rates are falling, dynamic funds invest in long-term bonds in order to lock in higher interest rates for a long time period. So when interest rates are rising, they invest in short-term bonds with a lock-in of 2-3 years.

Who Should Invest in Dynamic Bond Funds?

The performance of a dynamic fund is only as good as its fund manager’s prediction, hence they are only suited for high-risk appetite investors. Unlike debt funds, which are considered safer, dynamic funds carry high risk.

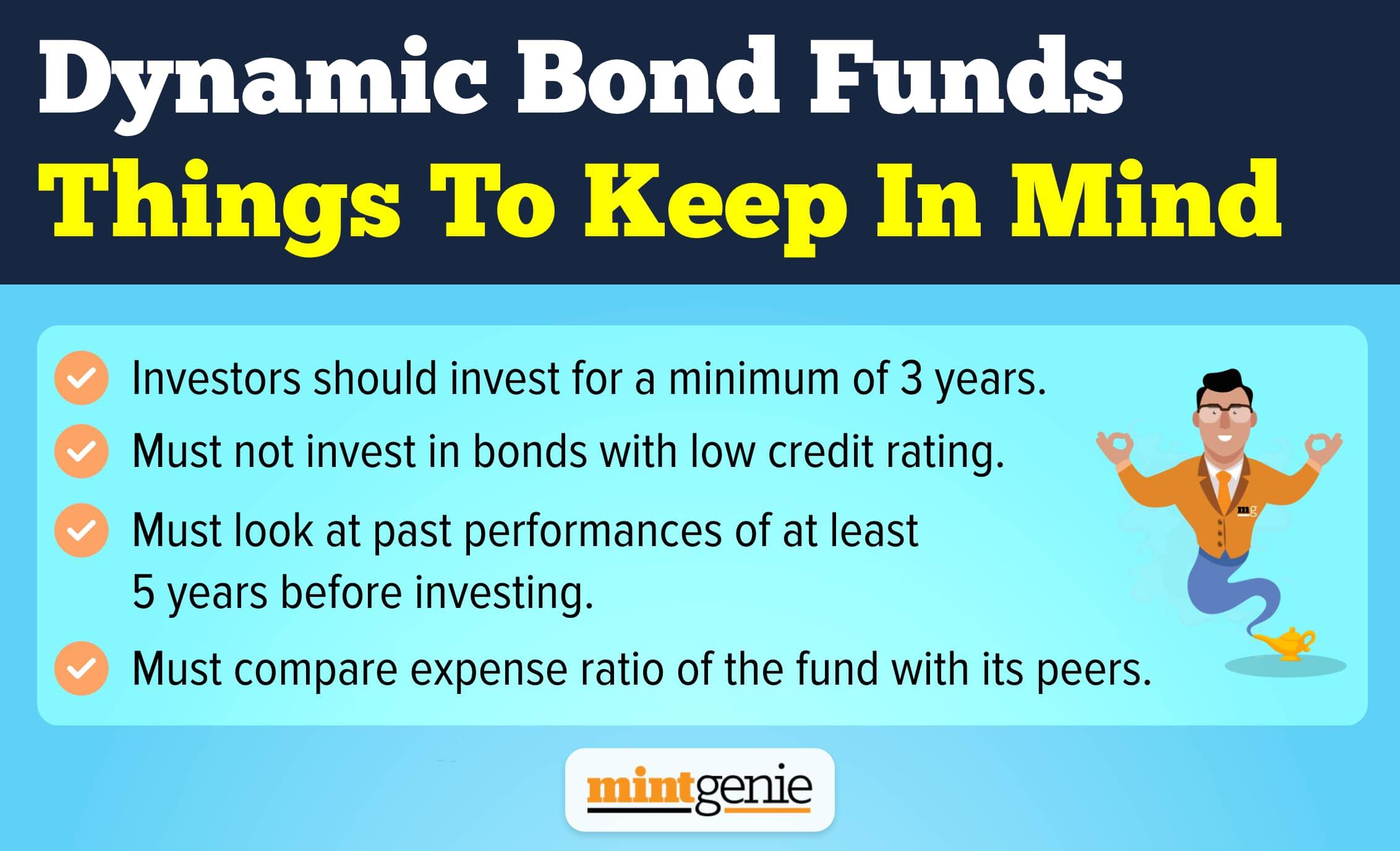

Also, investors who want to invest for less than 3 years would look at short-term bond funds. A 3-5 year investment horizon is ideal for a dynamic fund.

Investors can also invest in a dynamic fund through a SIP (Systematic Investment Plan) approach as it helps combat some volatility. One must always remember that the returns in these funds depend only on the interest rate movement.

Risks

There are 2 major risks associated with dynamic bond funds. These are - Credit risk and interest rate risk

Credit Risk: There is a risk that the borrower may not be able to pay the principal and interest amount. This happens when the fund manager invests in riskier bonds with a low credit rating. Which such bonds may have more growth potential, it also has the risk of failing to repay.

Interest rate risk: Since the whole fund is dependent on the fund manager's prediction of interest rate movement, there is always a chance that he/she may get it wrong. In case the fund manager expects a decline in rates and invests in long-term bonds but the rates rise. /this is an inherent risk any dynamic fund investor has to take. There is a 50-50 chance of winning and losing.

Things to keep in mind before investing

1) Maturity: Since dynamic bonds invest in both long-term and short-term bonds, the maturity of the funds are varying. They give an average maturity time and an investor must make sure that this average maturity time matches his/ her investment horizon.

2) Credit rating: While it is important for the fund manager to generate good returns, the investor must make sure that the bonds they invest in do not have a low credit rating.

3) Expense ratios: Since dynamic funds are active, they have a higher expense ratio. A high expense ratio reduces your returns, so it is important to compare the expense ratio between funds and make sure it is not too high in comparison to its peers.

Taxation of dynamic funds

Since dynamic bond funds are debt funds, they follow debt fund taxation. If the holding period of a dynamic bond fund is less than 36 months or 3 years, short-term capital gains tax is applicable. In this, the interest earned is added to your taxable income and taxed as per your IT slab.

If you hold the funds for over 3 years, a long-term capital gains tax of 20 percent with indexation benefit is incurred.

Dynamic funds are riskier by debt fund standards but can also deliver higher returns compared to the rest of them. Also, only investors with a horizon of 3-5 years should look to invest in these funds. Before investing in a dynamic fund, it is important to look at its performance for the last 5 years, to understand the capability of its fund manager.