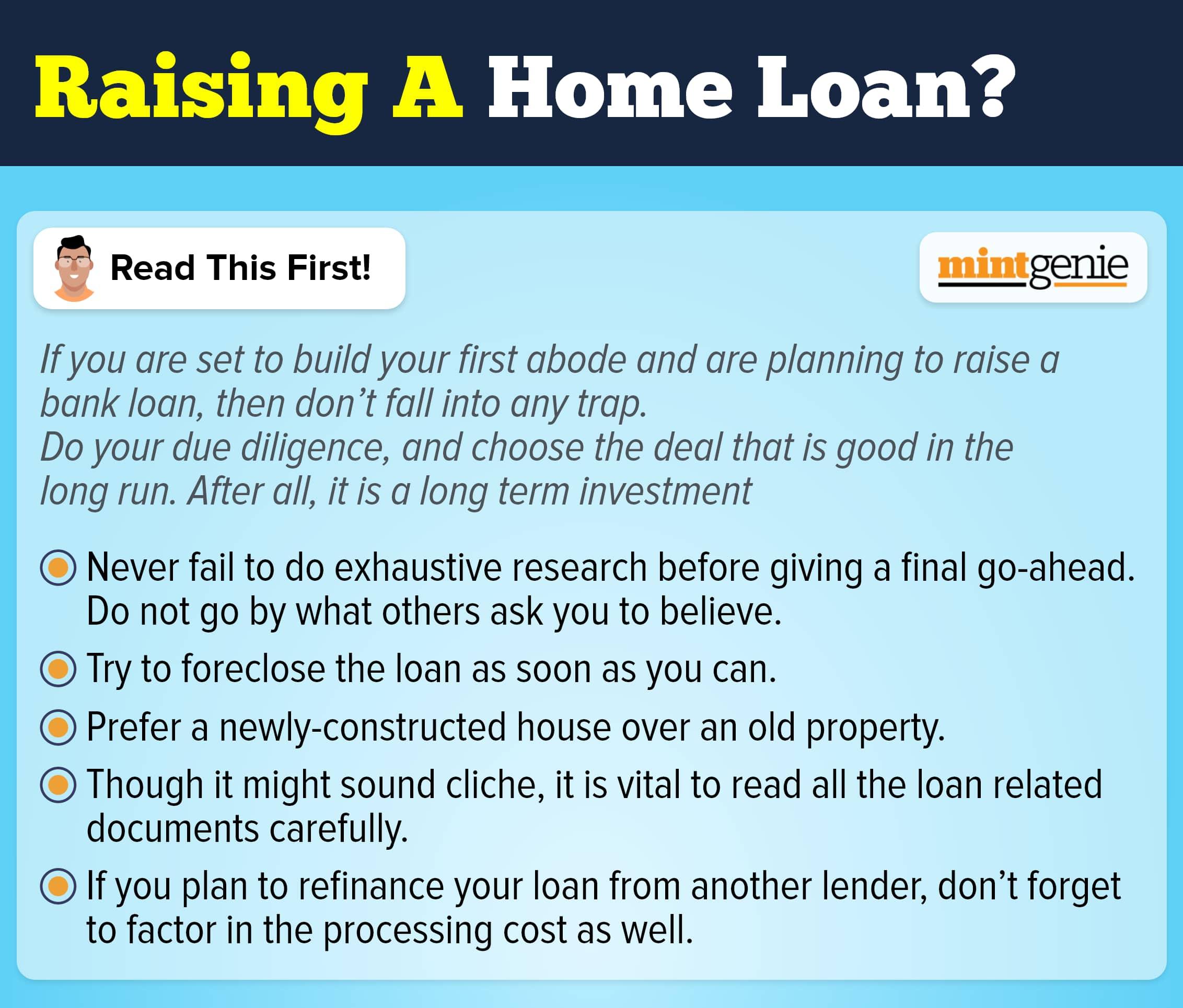

Think of taking a home loan for 20-30 years, and the first thought that creeps into your mind is whether you will be alive till then to repay the entire amount. Most often than not, borrowers die leaving behind the trail of liability on their loved ones’ shoulders. The onus of loan repayment then falls on co-borrowers and legal heirs that have then to decide whether they must pay back the entire loan amount or declare themselves as loan defaulters.

Lending banks and financial institutions often recommend a term insurance plan or home loan insurance to their borrowers to enable loan repayment by their legal heirs in their absence. Many borrowers refrain from buying insurance not realizing the financial burden they may be possibly leaving behind. This means that the co-borrowers or the legal heirs have now to repay the loan amount from their earnings.

Negotiating loan rates

The borrowing rate depends on a lot of factors out of which credit score matters the most. The credit score reflects the borrower’s ability to repay the loan. This is mostly calculated by considering the important factors including:

- Debt incurred through loans and credit cards

- Checking payment history to look for debt repaying ability

- Length of credit history

- The number and types of accounts you have

- Recent credit activity

Banks do not offer fixed loan interest rates but modify the same depending on the borrower’s credit score and loan tenure. This means that the credit score factor must never be ignored while looking for loans or borrowing money.

Renegotiating loan rates

The original loan amount was disbursed to the borrower depending on his or her credit score. But what if the borrower dies without having repaid the loan amount in full? Do the lenders uphold the practice of deciding loan rates based on credit scores with their new borrowers (aka co-borrowers or the legal heirs nominated by the original borrower)? Many legal heirs may have multiple income sources, less inclination to live on credit and enjoy high credit scores. This means that they are more likely to bargain for low-interest rates. However, do lenders live up to their word or are these appealing conditions and features limited to paper only?

Adhil Shetty, CEO, BankBazaar, says, “There are three options for the co-applicant and heirs of the borrowers. The default alternative is that the surviving co-applicant services the home loan instalments. If the co-applicant is unable to do so, the next step would be to negotiate with the bank to restructure the loan instalments depending on their capacity to repay the loan.

In case there are no co-borrowers or if they are unable to service the loan, then they can opt for the loan to be transferred to the legal heirs of the deceased borrower after executing a fresh set of documents.

In case the co-applicants and legal heirs are unable to take on the loan, the bank will try to find a mutually acceptable solution. This could be in the form of deferred payments, a smaller equate monthly instalment (EMI), or even a settlement in case the outstanding amount is small.”

Availing mortgage insurance coverage

A home loan extending to 25-30 lakhs can be a liability if not paid in time. This necessitates the need to seek insurance coverage equal to the loan amount so that the same can be repaid. It is because of this reason that some have mandated mortgage insurance coverage before agreeing to a loan application.