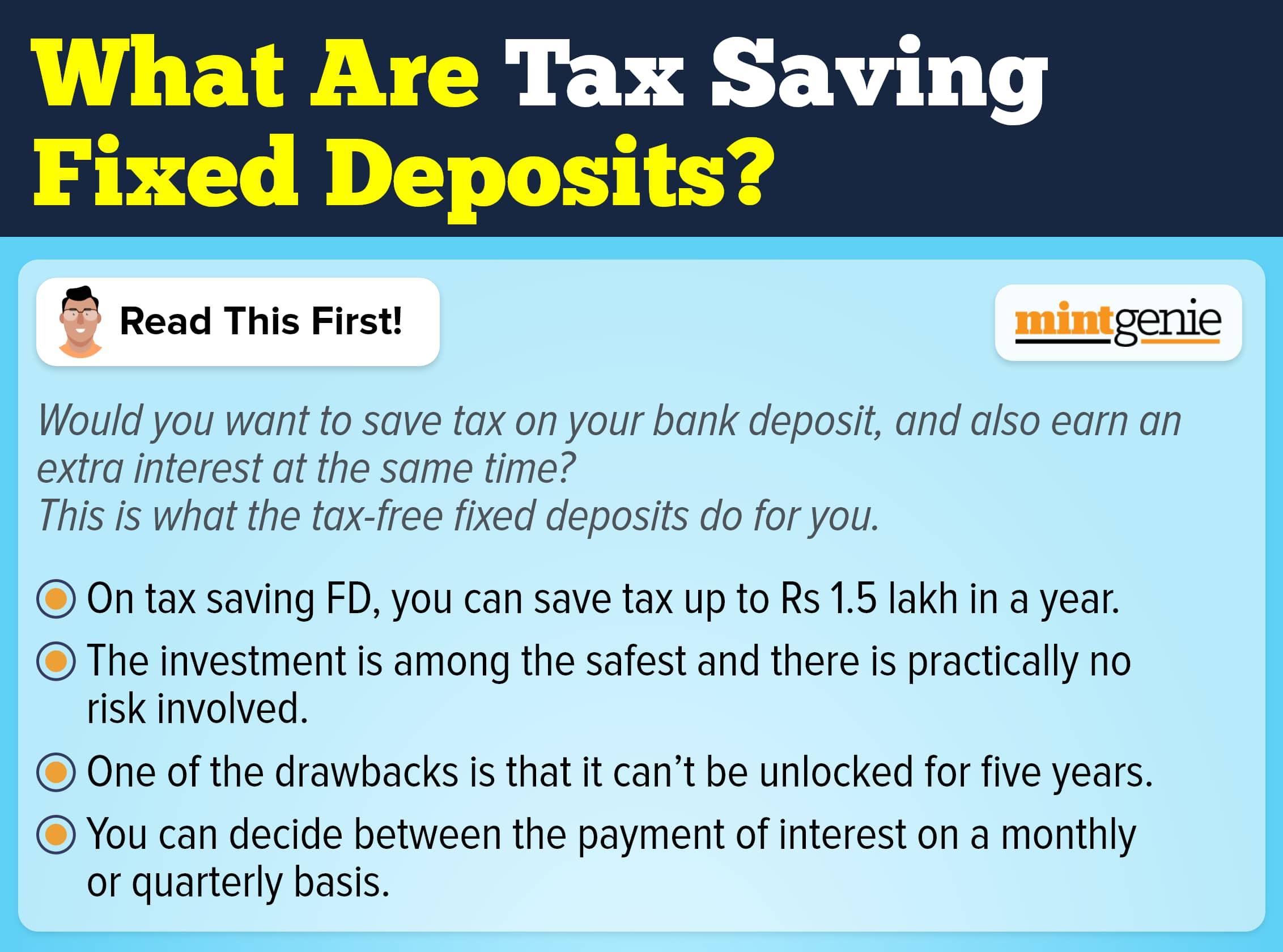

Tax Saving Fixed Deposits, as the name suggests, is the scheme that allows investors to avail tax deductions under section 80C of the Income Tax Act, 1961. The investors under the scheme are entitled to tax deduction so long as the investment does not exceed a threshold of ₹1,50,000.

The investment option is granted by banks and Non-Banking Financial Companies (NBFCs) where the investor can invest with low-risk and fixed interest rates. The Tax Saving Fixed Deposits is similar to Fixed Deposits offered by banks as the maturity amount is transferred directly to the bank accounts.

How does it work?

The investor is required to deposit a lump-sum amount with the financier for a fixed tenure decided by the investor. The investment gets locked-in with a fixed interest rate decided by the Central Bank and is unaffected by the market fluctuations till the time of maturity. Fixed Deposits are considered extremely safe and secure, and are suitable.

These Fixed Deposits can also be opened ‘individually’ as well as ‘jointly’ but the tax deduction in the case of joint Fixed Deposits can be only granted to the Primary Investor. Nomination facility is granted in these types of Fixed deposits, but in the case where the FD is held by, in the name of a minor then the nomination is not allowed.

Who should Invest?

Even though the scheme is beneficial for all age-groups who want to invest and get higher returns for the uncertain future, the investors — who are reaching retirement or are in the age group of senior citizens — have a greater incentive to invest in the scheme.

The banks offer higher interest rates to senior citizens for the scheme as they do to other investors. They can also claim higher deduction in taxes to the tune of ₹50,000 on the interest earned through deposits under Section 80 TTB. The other investors can claim tax deduction under the Section 80C.

Key Features

- Minimum deposit an investor can make is ₹1,000 and the maximum deposit can go upto ₹1,50,000 in one financial year.

- The tenure for the scheme is locked-in between 5-10 years.

- FD interest is taxable and can range from investor to investor considering the income tax bracket. (usually ranges between 0.4% - 30%) Financiers deduct 10% TDS if the interest earned for the financial year is more than ₹10,000.

- Premature withdrawal, loans and overdraft facilities are not available for Tax Saving Fixed Deposits unlike normal fixed deposits.

Tax Saving Fixed Deposits has the same criteria which is followed in Fixed Deposits granted by banks, but has an additional benefit of tax saving which makes it more attractive to the middle-class people. The scheme is completely safe and guarantees fixed return, which makes it attractive for the investors who want to speed up their revenue by doing the bare minimum.