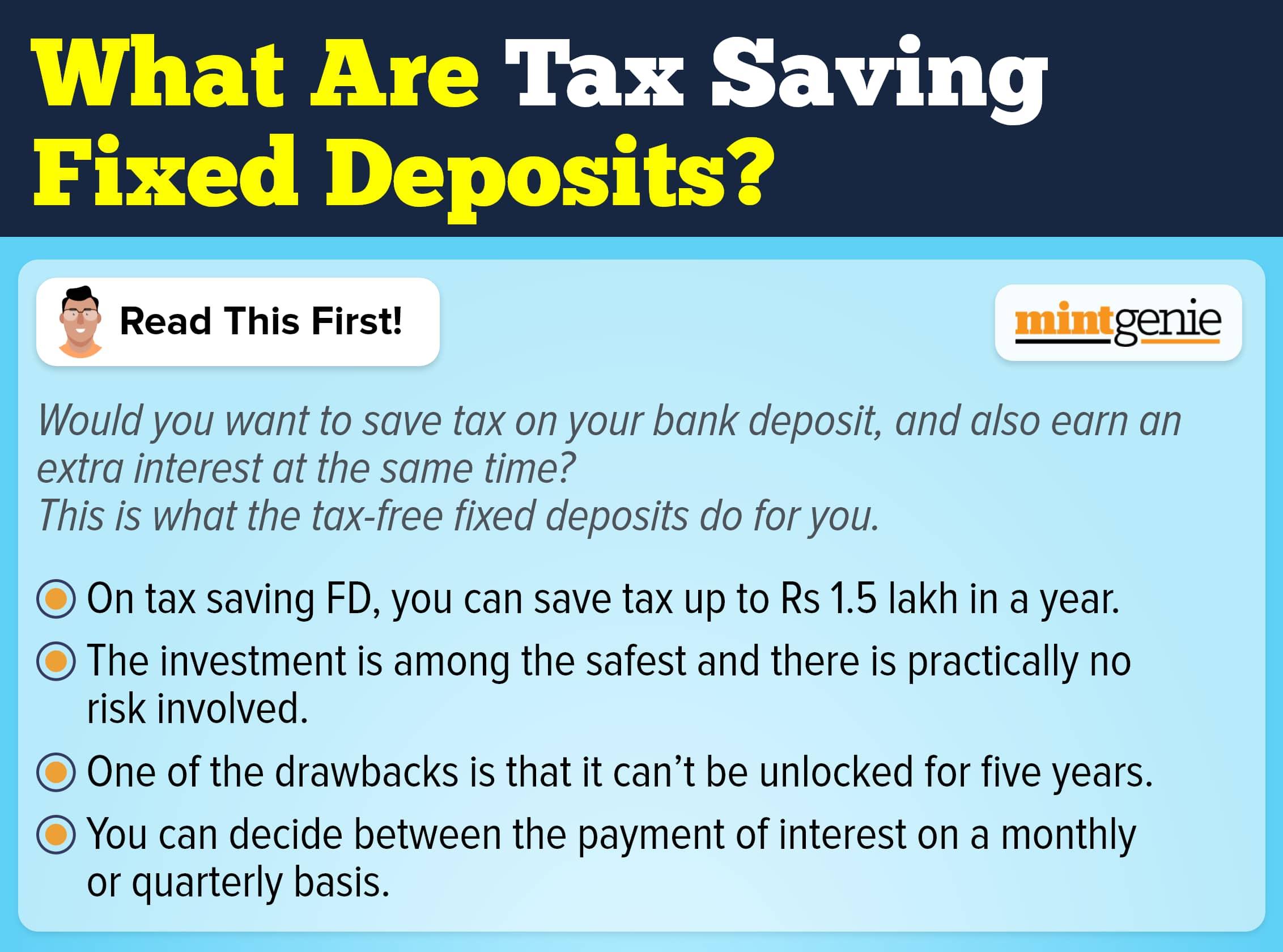

Investors often face a dilemma with planning their monthly returns through their investments. In case of senior citizens or retired individuals, the regular job-related income stops, and they must rely on their retirement corpus to take care of their day-to-day household and maintenance expenses.

Most of the above-mentioned investors are risk averse as the funds that are available with them must be kept safe so that they have the visibility of principal safety along with reasonable interest and lower taxation. The first investment avenue that comes into the mind in terms of safety and predictable returns is a bank fixed deposit.

Bank fixed deposits offer higher safety of principal with various options like monthly/quarterly/yearly interest withdrawals. However, when it comes to the flexibility and taxation aspect, fixed deposits offer little room for monthly withdrawals as the post tax amount is lower.

In this article, we will be discussing a lesser used avenue for fixed income and withdrawal planning i.e., debt mutual funds.

Debt mutual fund schemes in India enjoyed a tax benefit called Indexation until last month when the benefit was removed to make them at par with fixed deposits. However, there is still room for better tax planning in debt mutual funds as compared to fixed deposits. Earlier, debt mutual funds enjoyed indexation benefits if the investment was held for more than 3 years.

For example, if an investor purchased a debt mutual fund unit for Rs. 1,00,000 in 2010 and sold it for Rs. 1,50,000 in 2022, the actual capital gain is Rs. 50,000. However, if the inflation index during this period was 1.25, the indexed cost of acquisition would be Rs. 1,25,000 (Rs. 1,00,000 x 1.25).

This would result in a capital gain of Rs. (Rs. 1,50,000 - Rs. 1,25,000) = Rs. 25,000, This capital gain would be taxed at 20% instead of maximum marginal rate. With this benefit gone, investors are in a dilemma of whether to invest in debt mutual funds or not.

Let us compare the tax outflow for a scenario where an amount of Rs. 10,00,000 is invested in fixed deposit vs debt mutual fund with following assumptions:

- Return on investment = 7.5%

- Tax slab of investor is 30%

- Investment horizon is 10 years

Since the indexation benefit it removed, the tax would be similar on both the avenues, however, you can defer the tax incidence in debt mutual funds in following manner:

| Fixed Deposit | Debt Mutual Fund | |||||||

Year | Withdrawal | Tax | In hand | Value of FD | Withdrawal | Tax | In hand | Value of MF | Tax deferred |

1 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 1,570 | 73,430 | 10,00,000 | 20,930 |

2 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 3,030 | 71,970 | 10,00,000 | 19,470 |

3 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 4,388 | 70,612 | 10,00,000 | 18,112 |

4 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 5,652 | 69,348 | 10,00,000 | 16,848 |

5 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 6,827 | 68,173 | 10,00,000 | 15,673 |

6 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 7,921 | 67,079 | 10,00,000 | 14,579 |

7 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 8,938 | 66,062 | 10,00,000 | 13,562 |

8 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 9,884 | 65,116 | 10,00,000 | 12,616 |

9 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 10,764 | 64,236 | 10,00,000 | 11,736 |

10 | 75,000 | 22,500 | 52,500 | 10,00,000 | 75,000 | 11,583 | 63,417 | 10,00,000 | 10,917 |

In the above example, the tax impact on both the investments at the end of tenure will be the same. The cost price of a debt mutual fund will remain around Rs. 5,21,583 and the value would be around Rs. 10,75,000. Once you withdraw the entire corpus, the net tax outflow in the 10th year would be Rs. 1,66,024.

Now, the total tax paid during the entire duration is Rs. 2,25,000 for both the options, however, the quantum of tax payment in debt mutual funds was lower in earlier years. This ensures more money in the hands of investors when he/she needs it the most.

Following are the other pros and cons involved in debt mutual funds:

Pros

Liquidity: Debt mutual funds offer high liquidity & almost no cost. Fixed deposits might have a premature withdrawal charge.

Partial redemption: Partial withdrawal from debt mutual funds is possible in the multiples of Rs. 100.

Flexibility: An investor can increase or reduce the amount of yearly withdrawals depending upon the situation and need. Same is not possible in fixed deposits.

TDS: Debt mutual funds do not attract TDS on interest as compared to fixed deposits.

Cons

Predictability of returns: Returns of debt mutual funds are based on the interest rates in the economy. The yields can keep on varying over the investment horizon. Fixed deposits offer predictable returns and the interest rate is fixed.

Credit risk: Debt mutual funds invest in instruments of various corporate entities. There are chances of default by the investee company which can affect the principal component of investment. Fixed deposits of scheduled commercial banks are relatively safer.

TIP: Debt mutual funds offer better tax deferred returns but must be managed well to ensure the credit risk is not triggered. One must seek professional help to ensure they have invested in a debt mutual fund that suits their risk appetite.

Rohit Gyanchandani is Managing Director at Nandi Nivesh Private Limited